RESERVE BANK OF INDIA

Governor’s Statement

Date : Sep 30, 2022

In the last two and half years, the world has witnessed two major shocks – the COVID-19 pandemic and the conflict in Ukraine. These shocks have produced profound impact on the global economy. As if that was not enough, now we are in the midst of a third major shock – a storm – arising from aggressive monetary policy actions and even more aggressive communication from Advanced Economy (AE) central banks. The necessity of such actions is driven by their domestic considerations, but in a highly integrated global financial system, they inevitably cause negative externalities through global spillovers. The recent sharp rate hikes and forward guidance about further big rate hikes have caused tightening of financial conditions, extreme volatility and risk aversion. All segments of the financial market including equity, bond and currency markets are in turmoil across countries. There is nervousness in financial markets with potential consequences for the real economy and financial stability. The global economy is in the eye of a new storm.

2. Despite this unsettling global environment, the Indian economy continues to be resilient. There is macroeconomic stability. The financial system remains intact, with improved performance parameters. The country has withstood the shocks from COVID-19 and the conflict in Ukraine. Our journey over the last two and half years, our steely resolve in dealing with the various challenges gives us the confidence to deal with the new storm that we are confronted with.

Decisions and Deliberations of the Monetary Policy Committee (MPC)

3. The Monetary Policy Committee (MPC) met on 28th, 29th and 30th September 2022. Based on an assessment of the macroeconomic situation and its outlook, the MPC decided by a majority of five members out of six to increase the policy repo rate by 50 basis points to 5.9 per cent, with immediate effect. Consequently, the standing deposit facility (SDF) rate stands adjusted to 5.65 per cent; and the marginal standing facility (MSF) rate and the Bank Rate to 6.15 per cent. The MPC also decided by a majority of 5 out of 6 members to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

4. I would now explain the MPC’s rationale for its decisions on the policy rate and the stance. The global economic outlook continues to be bleak. Financial conditions are tightening and recession fears are mounting. Inflation continues to persist at alarmingly high levels across jurisdictions. The enduring effects of the pandemic and the geo-political conflict are manifesting in demand-supply mismatches of goods and services. Central banks are charting new territory with aggressive rate hikes, even if it entails sacrificing growth in the near term. In this milieu, nervous investor sentiments have triggered a flight to safety. The US dollar has strengthened rapidly to a two-decade high. Several advanced and emerging market currencies are facing sharp depreciation pressures. Emerging market economies (EMEs), in particular, are confronted with challenges of slowing global growth, elevated food and energy prices, spillovers from advanced economy policy normalisation, debt distress and sharp currency depreciations.

5. Against this challenging global environment, economic activity in India remains stable. While real GDP growth in Q1:2022-23 turned out to be lower than our expectations, the late recovery in kharif sowing, the comfortable reservoir levels, improvement in capacity utilisation, buoyant bank credit expansion and government’s continued thrust on capital expenditure are expected to support aggregate demand and output in H2:2022-23.

6. Consumer price inflation remains elevated and above the upper tolerance band of the target due to large adverse supply shocks, some firming up of domestic demand, and the spillovers from global financial markets. The recent correction in global commodity prices including crude oil, if sustained, may ease cost pressures in the coming months. The inflation trajectory remains clouded with uncertainties arising from continuing geopolitical tensions and nervous global financial market sentiments.

7. In this backdrop, the MPC was of the view that persistence of high inflation necessitates further calibrated withdrawal of monetary accommodation to restrain broadening of price pressures, anchor inflation expectations and contain the second-round effects. This action will support medium-term growth prospects. Accordingly, the MPC decided to increase the policy repo rate by 50 basis points to 5.9 per cent and to remain focused on withdrawal of accommodation, while supporting growth.

8. Let me step back and elaborate on our monetary policy stance. Monetary policy had moved from neutral to accommodative stance in June 2019. At that time, the repo rate was 5.75 per cent; headline CPI inflation was hovering around 3 per cent and was expected to be in the range of 3.4 to 3.7 per cent in H2:2019-20; and, liquidity was in deficit mode, with an average daily net injection of ₹0.3 lakh crore in May 2019 under the liquidity adjustment facility (LAF). Today, inflation is hovering around 7 per cent and we expect it to remain elevated at around 6 per cent in H2:2022-23. Liquidity remains surplus, with average daily net absorption of ₹1.1 lakh crore under the LAF in September 2022 (up to September 28). As government expenditure picks up on the back of high GST and direct tax collections, the system liquidity will go up further. Thus, even as the nominal policy repo rate has been raised by 190 basis points so far (including today’s increase), the policy rate adjusted for inflation trails the 2019 levels. The overall monetary and liquidity conditions, therefore, remain accommodative and hence, the MPC decided to remain focused on withdrawal of accommodation.

Assessment of Growth and Inflation

Growth

9. Real GDP grew by 13.5 per cent (y-o-y) in Q1:2022-23, surpassing the pre-pandemic level by 3.8 per cent. This was led by robust growth in private consumption and investment demand.

10. High frequency data for Q2 indicate that economic activity remains resilient. Private consumption has been holding up. There is a sustained revival in urban demand which should get a further impetus from unfettered celebration of upcoming festivals after two and half years of living with COVID-19. Rural demand is also gaining gradually. Investment demand is picking up and is evident from the robust growth of domestic production and import of capital goods in July and August. Bank credit grew at an accelerated pace of 16.2 per cent y-o-y as on September 9, 2022 as against 6.7 per cent a year ago. Total flow of financial resources from banks and non-banks to the commercial sector has improved significantly to ₹9.3 lakh crore in this financial year so far (up to September 9) from ₹1.7 lakh crore in the corresponding period of last year. According to RBI survey, seasonally adjusted capacity utilisation of the manufacturing sector improved from 73.0 per cent in Q4: 2021-22 to 74.3 per cent in Q1:2022-23 – its highest level in three years1. Non-oil non-gold imports remained resilient, indicating sustained revival in domestic demand. Merchandise exports growth, however, faced headwinds in an unsettled external environment.

11. In the supply side, the agricultural sector remains resilient. The monsoon rainfall was 7 per cent above the long period average (LPA) as on September 29. Kharif sowing was 1.7 per cent above the normal sown area as on September 23. The production of kharif foodgrains as per the first advance estimate is only 0.4 per cent below the first advance estimate of last year. The reservoir levels are at 87 per cent of the full capacity on September 29, 2022 as against the decadal average of 77 per cent. This augurs well for the ensuing Rabi crop.

12. Industrial activity, reflected in the growth of index of industrial production (IIP) (y-o-y), slipped to 2.4 per cent in July. India’s manufacturing purchasing managers index (PMI), however, indicates sustained expansion at 56.2 in August. Business sentiment, as reflected in the manufacturing PMI, strengthened with the degree of optimism at its highest in six years.

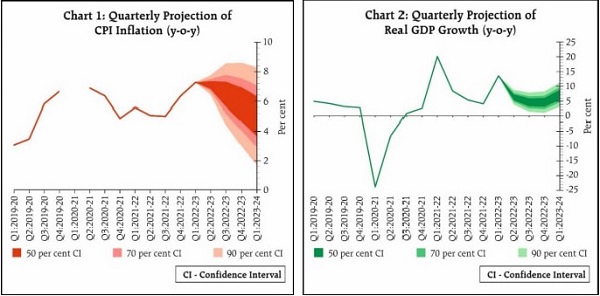

13. Services sector indicators2 point towards strong growth in July and August. Services PMI rebounded to 57.2 in August from 55.5 in July. Business confidence rose to a 51-month high.

14. Looking ahead, all these factors3 should support aggregate demand and activity. The headwinds from extended geopolitical tensions, tightening global financial conditions and possible decline in the external component of aggregate demand can pose downside risks to growth. Taking all these factors into consideration, real GDP growth for 2022-23 is projected at 7.0 per cent with Q2 at 6.3 per cent; Q3 at 4.6 per cent; and Q4:2022-23 at 4.6 per cent, with risks broadly balanced. The growth for Q1:2023-24 is projected at 7.2 per cent.

Inflation

15. Global geopolitical developments are weighing heavily on the domestic inflation trajectory. Inflation inched up to 7.0 per cent in August from 6.7 per cent in July.

16. Acute imported inflation pressures felt at the beginning of the financial year have eased but remain elevated across food and energy items. Edible oil price pressures are likely to remain contained on improved supply from key producing countries and measures taken by the Government. Going forward, there could be some tapering of selling price increases on account of easing supply conditions and softening of industrial metal and crude oil prices. With services activity showing strong rebound and some improvement in pricing power, risks of higher pass-through of input costs, however, do remain.

17. There are also upside risks to food prices. Cereal price pressure is spreading from wheat to rice due to the likely lower kharif paddy production. The lower sowing for kharif pulses could also cause some pressures. The delayed withdrawal of monsoon and intense rain spells in various regions have already started to impact vegetable prices, especially tomatoes. These risks to food inflation could have an adverse impact on inflation expectations.

18. The Indian basket crude oil price was around US$ 104 per barrel in H1:2022-23. Going forward, we are now assuming it to be US$ 100 per barrel in H2:2022-23. Taking into account these factors, the inflation projection is retained at 6.7 per cent in 2022-23, with Q2 at 7.1 per cent; Q3 at 6.5 per cent; and Q4 at 5.8 per cent, with risks evenly balanced. CPI inflation is projected to further reduce to 5.0 per cent in Q1:2023-24.

19. The extraordinary global circumstances that caused the heightened inflationary pressures have impacted both AEs and EMEs. India is, however, better placed than many of these economies. If high inflation is allowed to linger, it invariably triggers second order effects and unsettles expectations. Therefore, monetary policy has to carry forward its calibrated action on policy rates and liquidity conditions consistent with the evolving inflation growth dynamics. It must remain alert and nimble.

Liquidity and Financial Market Conditions

20. During the current financial year, the weighted average call rate (WACR) – the operating target of monetary policy – has increased cumulatively by 196 bps in a phased manner (up to September 28) over March 2022. This is in sync with our actions on the SDF and the repo rate. Consequently, interest rates across the financial market spectrum4have increased, though at varying degrees.

21. Surplus liquidity in the banking system, as reflected in average daily absorptions under the liquidity adjustment facility (LAF) [both SDF and variable rate reverse repo (VRRR) auctions], moderated to ₹2.3 lakh crore during August – September 2022 (up to September 28) from ₹3.8 lakh crore during June-July. GST and advance tax payments coupled with forex outflows moderated the surplus liquidity conditions in the third week of September. This necessitated recourse to the marginal standing facility (MSF) by banks and liquidity injection by the RBI through variable rate repo (VRR) auctions. This temporary moderation of surplus liquidity needs to be seen in the context of the large potential liquidity in the system arising from the expected pick-up in government spending that usually happens in the second half of the year. Furthermore, drawdown of excess cash reserve ratio (CRR) and excess statutory liquidity ratio (SLR) holdings of banks can also augment system liquidity.

22. In my policy statement of October 2021, I had stated that the RBI may complement the fortnightly main operation conducted through 14-day VRRR auctions with 28-day VRRR auctions depending upon the evolving liquidity conditions. In view of the moderation in surplus liquidity, it has now been decided to merge the 28-day VRRR with the fortnightly 14-day main auction. Consequently, from now on, only 14-day VRRR auctions will be conducted. Fine-tuning operations of various maturities for absorption as well as injection of liquidity will continue as may be necessary from time to time.

23. During the current financial year (up to September 28), the US dollar has appreciated by 14.5 per cent against a basket of major currencies. This has caused turmoil in currency markets globally. The movement of the Indian Rupee (INR) has, however, been orderly compared to most other countries. It has depreciated by 7.4 per cent against the US dollar during the same period – faring much better than several reserve currencies as well as many of its EME and Asian peers.

24. A stable exchange rate is a beacon of financial and overall macroeconomic stability and market confidence. In recent days, there have been divergent views on the exchange rate of the rupee and the adequacy of our forex reserves. Let me set out the overall position once again. First, the rupee is a freely floating currency and its exchange rate is market determined. Second, the RBI does not have any fixed exchange rate in mind. It intervenes in the market to curb excessive volatility and anchor expectations. The overarching focus is on maintaining macroeconomic stability and market confidence. Our actions have helped in engendering investor confidence as reflected in the return of capital inflows since July. Over the medium term, the primacy of price stability embedded in our flexible inflation targeting (FIT) framework provides the anchor for exchange rate stability. Third, our interventions in the forex market are based on continuous assessment of the prevailing and evolving situation from the point of view of our approach which I just explained. The aspect of adequacy of forex reserves is always kept in mind. The umbrella continues to be strong.

25. During the pandemic, forward guidance gained prominence in the Reserve Bank’s communication strategy. This was helpful in anchoring market expectations. In a policy tightening cycle, however, it is arduous to provide consistent forward guidance, particularly in a highly uncertain environment. In fact, forward guidance may even destabilise financial markets. Questions are often asked about the peak and terminal rates in a rate tightening cycle. Without venturing into any forward guidance which can be hazardous in the present context, I would like to state that our actions will be carefully calibrated to the incoming data and evolving scenario without being constrained by conventional or any textbook approach to policy making.

External Sector

26. The current account deficit (CAD) for Q1:2022-23 is placed at 2.8 per cent of GDP with trade deficit at 8.1 per cent of GDP. Various leading indicators, including global PMIs, point to weakening of global growth momentum and downside risks to global trade. India’s import growth, though decelerating5, outpaced export growth. Consequently, the trade deficit remained high in July-August 2022. Services exports continued to grow at a robust pace amidst resilient demand for software and business services and modest recovery in travel services. On a balance of payments (BOP) basis, for which data were released yesterday, exports of services grew at a robust pace of 35.4 per cent (y-o-y) in April-June this year. For the same period, remittances rose by 22.6 per cent. The net surplus on exports of services is expected to partly offset the higher trade deficit.

27. From external financing side, net foreign direct investment (FDI) improved to US$ 18.9 billion in April-July 2022 from US$ 13.1 billion a year ago. Foreign portfolio investors (FPIs) have returned to the domestic market with net inflow of US$ 7.5 billion during July-September after an outflow for nine consecutive months. India’s foreign exchange reserve at US$ 537.5 billion as on September 23, 2022 compares favourably with most peer economies. About 67 per cent of the decline in reserves during the current financial year is due to valuation changes arising from an appreciating US dollar and higher US bond yields. Incidentally, there was an accretion of US$ 4.6 billion to the foreign exchange reserves on balance of payments (BOP) basis during Q1:2022-23. India’s other external indicators, viz., external debt to GDP ratio; net international investment position to GDP ratio; ratio of short-term debt to reserves; and debt service ratio also indicate lower vulnerability as compared with most other major EMEs6. In fact, India’s external debt to GDP ratio is the lowest among major EMEs. In the final analysis, we remain confident of meeting our external financing requirements comfortably.

Additional Measures

28. I shall now announce certain additional measures.

Discussion Paper on Expected Loss (EL) Based Approach for Loan Loss Provisioning by Banks

29. Banks currently follow the incurred loss approach for provisioning on their loan assets, whereby provisions on loan assets are made after the stress has materialised. A more prudent and forward looking approach is the expected loss based approach, which requires banks to make provisions based on an assessment of probable losses. As a step towards converging with globally accepted prudential norms, we will issue a discussion paper on the proposed transition for stakeholder comments.

Discussion Paper on Securitisation of Stressed Assets Framework (SSAF)

30. The revised framework for securitisation of standard assets was issued by the Reserve Bank in September 2021. It has now been decided to introduce a framework for securitisation of stressed assets. This will provide an alternative mechanism for securitisation of NPAs, in addition to the existing ARC route. A Discussion Paper (DP) on the proposed framework is being issued for feedback from stakeholders.

Internet Banking Facility for Customers of RRBs

31. Regional Rural Banks (RRBs) are currently allowed to provide Internet Banking facility to their customers, subject to fulfilment of certain criteria. Keeping in view the need to promote the spread of digital banking in rural areas, these criteria are being rationalised. The revised guidelines will be issued separately.

Regulating Offline Payment Aggregators

32. Online Payment Aggregators (PAs) have been brought under the purview of RBI regulations since March 2020. It is now proposed to extend these regulations to offline PAs, who handle proximity/ face-to-face transactions. This measure is expected to bring in regulatory synergy and convergence on data standards.

Conclusion

33. Daunting challenges confront us at this juncture. The underlying fundamentals of our economy and the buffers built over the years have stood us in good stead. We have taken a series of measures since April 2022 in the backdrop of geopolitical tensions, sanctions and supply chain disruptions. We will remain resolute and persevere in our efforts to ensure price stability as well as financial stability, while supporting growth. Our policy action today is part of our continued efforts in pursuit of these goals. As we celebrate Mahatma Gandhi’s birth anniversary in another two days, I conclude my statement with his insightful words: “…we are ever wakeful, ever vigilant, ever striving.”7Today, despite the gathering clouds over the global economy, the Indian economy inspires optimism and confidence.

Thank you. Namaskar.

(Yogesh Dayal)

Chief General Manager

Press Release: 2022-2023/966

*****

Monetary Policy Statement, 2022-23 Resolution of the Monetary Policy Committee (MPC) September 28-30, 2022

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (September 30, 2022) decided to:

- Increase the policy repo rate under the liquidity adjustment facility (LAF) by 50 basis points to 5.90 per cent with immediate effect.

Consequently, the standing deposit facility (SDF) rate stands adjusted to 5.65 per cent and the marginal standing facility (MSF) rate and the Bank Rate to 6.15 per cent.

- The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

The main considerations underlying the decision are set out in the statement below.

Assessment

Global Economy

2. Global economic activity is weakening under the impact of the protracted conflict in Ukraine and aggressive monetary policy actions and stances across the world. As financial conditions tighten, global financial markets are experiencing surges of volatility, with sporadic sell-offs in equity and bond markets, and the US dollar strengthening to a 20-year high. Emerging market economies (EMEs) are facing intensified pressures from retrenchment of portfolio flows, currency depreciations, reserve losses and financial stability risks, besides the global inflation shock. As external demand deteriorates, their macroeconomic outlook is becoming increasingly adverse.

Domestic Economy

3. Real gross domestic product (GDP) grew year-on-year (y-o-y) by 13.5 per cent in Q1:2022-23. While all constituents of domestic aggregate demand expanded y-o-y and exceeded their pre-pandemic levels, the drag from net exports provided an offset. On the supply side, gross value added (GVA) rose by 12.7 per cent in Q1:2022-23, with all constituents recording y-o-y growth and most notably, services.

4. Aggregate supply conditions are improving. With the south-west monsoon rainfall 7 per cent above the long period average (LPA) as on September 29 and its spatial distribution spreading to some deficit areas, kharif sowing has been catching up. Acreage was 1.7 per cent above the normal sown area as on September 23 and only 1.2 per cent below last year’s coverage. The production of kharif foodgrains as per first advance estimates (FAE) was 3.9 per cent below last year’s fourth advance estimates (only 0.4 per cent below last year’s FAE). Activity in industry and services sectors remains in expansion, especially the latter, as reflected in purchasing managers indices (PMIs) and other high frequency indicators. The index of industrial production growth, however, slowed to 2.4 per cent (y-o-y) in July.

5. On the demand side, urban consumption is being lifted by discretionary spending ahead of the festival season and rural demand is gradually improving. Investment demand is also gaining traction, as reflected in rising imports and domestic production of capital goods, steel consumption and cement production. Merchandise exports posted a modest expansion in August. Non-oil non-gold imports remained buoyant.

6. CPI inflation rose to 7.0 per cent (y-o-y) in August 2022 from 6.7 per cent in July as food inflation moved higher, driven by prices of cereals, vegetables, pulses, spices and milk. Fuel inflation moderated with reduction in kerosene (PDS) prices, though it remained in double digits. Core CPI (i.e., CPI excluding food and fuel) inflation remained sticky at heightened levels, with upside pressures across various constituent goods and services.

7. Overall system liquidity remained in surplus, with the average daily absorption under the liquidity adjustment facility (LAF) easing to ₹2.3 lakh crore during August-September (up to September 28, 2022) from ₹3.8 lakh crore in June-July. Money supply (M3) expanded y-o-y by 8.9 per cent, with aggregate deposits of commercial banks growing by 9.5 per cent and bank credit by 16.2 per cent as on September 9, 2022. India’s foreign exchange reserves were placed at US$ 537.5 billion as on September 23, 2022.

Outlook

8. High and protracted uncertainty surrounding the course of geopolitical conditions weighs heavily on the inflation outlook. Commodity prices, however, have softened and recession risks in advanced economies (AEs) are rising. On the domestic front, the late recovery in sowing augurs well for kharif output. The prospects for the rabi crop are buffered by comfortable reservoir levels. The risk of crop damage from excessive/unseasonal rains, however, remains. These factors have implications for the food price outlook. Elevated imported inflation pressures remain an upside risk for the future trajectory of inflation, amplified by the continuing appreciation of the US dollar. The outlook for crude oil prices is highly uncertain and tethered to geopolitical developments, with attendant concerns relating to both supply and demand. The Reserve Bank’s enterprise surveys point to some easing of input cost and output price pressures across manufacturing, services and infrastructure firms; however, the pass-through of input costs to prices remains incomplete. Taking into account these factors and an average crude oil price (Indian basket) of US$ 100 per barrel, inflation is projected at 6.7 per cent in 2022-23, with Q2 at 7.1 per cent; Q3 at 6.5 per cent; and Q4 at 5.8 per cent, and risks are evenly balanced. CPI inflation for Q1:2023-24 is projected at 5.0 per cent (Chart 1).

9. On growth, the improving outlook for agriculture and allied activities and rebound in services are boosting the prospects for aggregate supply. The Government’s continued thrust on capex, improvement in capacity utilisation in manufacturing and pick-up in non-food credit should sustain the expansion in industrial activity that stalled in July. The outlook for aggregate demand is positive, with rural demand catching up and urban demand expected to strengthen further with the typical upturn in the second half of the year. According to the RBI’s surveys, consumer outlook remains stable and firms in manufacturing, services and infrastructure sectors are optimistic about demand conditions and sales prospects. On the other hand, headwinds from geopolitical tensions, tightening global financial conditions and the slowing external demand pose downside risks to net exports and hence to India’s GDP outlook. Taking all these factors into consideration, real GDP growth for 2022-23 is projected at 7.0 per cent with Q2 at 6.3 per cent; Q3 at 4.6 per cent; and Q4 at 4.6 per cent, and risks broadly balanced. For Q1:2023-24, it is projected at 7.2 per cent (Chart 2).

10. In the MPC’s view, inflation is likely to be above the upper tolerance level of 6 per cent through the first three quarters of 2022-23, with core inflation remaining high. The outlook is fraught with considerable uncertainty, given the volatile geopolitical situation, global financial market volatility and supply disruptions. Meanwhile, domestic economic activity is holding up well and is expected to be buoyant in H2:2022-23, supported by festive season demand amidst consumer and business optimism. The MPC is of the view that further calibrated monetary policy action is warranted to keep inflation expectations anchored, restrain the broadening of price pressures and pre-empt second round effects. The MPC feels that this action will support medium-term growth prospects. Accordingly, the MPC decided to increase the policy repo rate by 50 basis points to 5.90 per cent. The MPC also decided to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

11. Dr. Shashanka Bhide, Prof. Jayanth R. Varma, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to increase the policy repo rate by 50 basis points. Dr. Ashima Goyal voted to increase the repo rate by 35 basis points.

12. Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Rajiv Ranjan, Dr. Michael Debabrata Patra and Shri Shaktikanta Das voted to remain focused on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth. Prof. Jayanth R. Varma voted against this part of the resolution.

13. The minutes of the MPC’s meeting will be published on October 14, 2022.

14. The next meeting of the MPC is scheduled during December 5-7, 2022.

(Yogesh Dayal)

Chief General Manager

Press Release: 2022-2023/967

*****

Statement on Developmental and Regulatory Policies

This Statement sets out various developmental and regulatory policy measures relating to (i) Regulation and Supervision; and (ii) Payment and Settlement systems.

I. Regulation and Supervision

1. Discussion Paper on Expected Loss Based Approach for Loan Loss Provisioning by Banks

The inadequacy of the incurred loss approach for provisioning by banks and its procyclicality, which amplified the downturn following the financial crisis of 2007-09, has been extensively documented. One of the major elements of the global response to these findings have been a shift to expected credit loss (ECL) regime for provisioning. As a further step towards converging with globally accepted prudential norms, it is proposed to adopt expected loss approach for loss allowances required to be maintained by banks in respect of their exposures. As a first step, a discussion paper on the various aspects of the transition will be issued shortly.

2. Discussion Paper on Securitisation of Stressed Assets Framework (SSAF)

In September 2021, the Reserve Bank had issued the revised framework for securitisation of standard assets. As regards securitisation of non-performing assets, the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest (SARFAESI) Act, 2002 currently provides a framework for such securitisations to be undertaken by Asset Reconstruction Companies (ARCs) licensed under the Act. However, based on market feedback, stakeholder consultations and the recommendations of the Task Force on Development of Secondary Market for Corporate Loans (RBI, 2019), it has been decided to introduce a framework for securitisation of stressed assets in addition to the ARC route, similar to the framework for securitisation of standard assets. Accordingly, a Discussion Paper (DP) detailing relevant contours of the proposed framework will be issued shortly inviting comments on certain specific aspects.

3. Internet Banking Facility for Customers of Regional Rural Banks (RRBs)

The RRBs are currently allowed to provide Internet Banking facility to their customers with prior approval of the Reserve Bank, subject to fulfilment of certain financial and non-financial criteria. Keeping in view the need to promote the spread of digital banking in rural areas, the criteria for RRBs to be eligible to provide internet banking are being rationalised and guidelines are being issued separately.

II. Payment and Settlement Systems

4. Regulating Offline Payment Aggregators

Payment Aggregators (PAs) play an important role in the payments ecosystem and hence were brought under regulations in March 2020 and designated as Payment System Operators (PSOs). The current regulations are, however, applicable to PAs processing online or e-commerce transactions. These regulations do not cover offline PAs who handle proximity/face-to-face transactions and play a significant role in the spread of digital payments. Keeping in view the similar nature of activities undertaken by online and offline PAs, it is proposed to apply the current regulations to offline PAs as well. This measure is expected to bring in synergy in regulation covering activities and operations of PAs apart from convergence on standards of data collection and storage. Detailed instructions will be issued separately.

(Yogesh Dayal)

Chief General Manager

Press Release: 2022-2023/968

Notes:

1 This is notwithstanding the decline in unadjusted capacity utilisation from 75.3 per cent to 72.4 per cent over the same period reflecting seasonal pattern.

2 Railway freight traffic; port freight traffic; domestic air passenger traffic; e-way bills; toll collections, etc.

3 The recovery in kharif sowing, adequate reservoir levels, an upsurge in discretionary spending, moderation in commodity prices, Government’s continued thrust on capex, improvement in capacity utilisation in manufacturing, pick-up in bank credit and waning COVID-19 infections.

4 91-day treasury bills, commercial paper (CPs) and certificates of deposit (CDs), bond yields. (The rate hikes also triggered an upward adjustment in the benchmark lending rates of banks. In tandem, term deposit rates have also increased as banks compete for mobilising resources to meet the resurgent credit demand.)

5 Growth in merchandise imports moderated from 49.5 per cent in Q1:2022-23 to 43.6 per cent in July and 37.3 per cent in August 2022.

6 Net international investment position to GDP ratio is in terms of net claims of non-residents on India and ratio of short-term debt to reserves is measured in terms of residual maturity.

7 The Mind of Mahatma Gandhi by R.K. Prabhu and U.R.Rao, Navajivan Mudranalaya, Ahmedabad, India; page 153