Non-Banking Financial Corporations (NBFCs) play a crucial role in India’s financial landscape. Governed by the Reserve Bank of India (RBI), NBFCs offer diverse financial services, from loans to investment activities. Understanding their regulation, types, and core functions is essential for stakeholders in the financial sector.

REGULATOR

Reserve Bank of India is regulator of the Non-Banking Financial Companies under the provisions of Chapter III B of the Reserve Bank of India Act, 1934.

With the amendment of the Reserve Bank of India Act, 1934 in January 1997, in terms of Section 45 IA of the Act, all Non-Banking Financial Companies have to be mandatorily registered with the Reserve Bank of India.

Non-Banking Financial Company (NBFC) –

A) Meaning of NBFC –

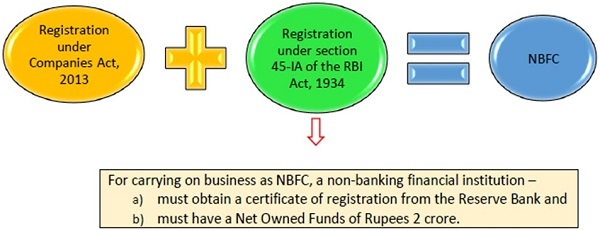

A Non-Banking Financial Company (NBFC) is a company registered under the Companies Act, 1956/2013 engaged in the business of –

a) loans and advances,

b) acquisition of shares/stocks/bonds/debentures/securities issued by Government or local authority or other marketable securities

c) leasing,

d) hire-purchase,

e) insurance business,

f) chit business

but does not include any institution whose principal business is that of

a) agriculture activity,

b) industrial activity,

c) purchase or sale of any goods (other than securities) or providing any services and sale/purchase/construction of immovable property.

Note-

A non-banking institution which is a company and has principal business of receiving deposits under any scheme or arrangement in one lump sum or in installments by way of contributions or in any other manner, is also a non-banking financial company.

Meaning of Financial activity as principal business – 50-50 test for NBFC’s

A 50/50 test means that –

a) a firm’s financial assets constitute more than 50% of the total assets; and

b) income from financial assets constitute more than 50% of the gross income.

A firm which fulfills both these criteria will be registered with the RBI as an NBFC. If, after registration, a firm violates the 50/50 criteria then RBI has the authority to penalize the NBFC.

Definition of NBFC

Section 45 I (f) of RBI Act, 1934

- a financial institution which is a company;

- a non-banking institution which is a company and which has as its principal business, the receiving of deposits, under any scheme or arrangement or in any other manner, or lending in any manner;

- such other non-banking institution or class of such institutions, as the Bank may, with the previous approval of the Central Government and by notification in the Official Gazette, specify

Section 45 I (c) of RBI Act, 1934- Financial Institution includes

- Making loans and advances,

- Acquisition of shares, stock, bonds, debentures, securities issued by Government or other marketable securities, etc,

- Letting/delivering of goods to hirer under Hire Purchase Agreement,

- Carrying on any class of insurance business.

- Chit business or accepting public deposits under any Scheme / Arrangement.

Does not include

- any institution whose principal business is that of agriculture activity,

- industrial activity, purchase or sale of any goods (other than securities)

- or providing any services and sale/purchase/construction of immovable property.

> No NBFC shall commence or carry on business of non-banking financial institution without:

– Obtaining Certificate of Registration from RBI; and

– Having a Minimum Net Owned Fund of Rs. 200 Lakhs.

> A company also needs to register as NBFC with RBI, if it fulfils the 50:50 test:

– financial assets constitute more than 50 percent of the total assets and

– income from financial assets constitute more than 50 percent of its gross income.

Exemptions:

> To avoid dual regulation, certain categories of NBFCs which are regulated by other regulators are exempted from the requirement of registration with RBI

– Venture Capital Fund/Merchant Banking companies/ Stock broking companies registered with SEBI

– Insurance Company holding a valid Certificate of Registration issued by IRDA

– Nidhi companies as notified under Section 620A of the Companies Act, 1956

– Chit companies as defined in clause (b) of Section 2 of the Chit Funds Act, 1982

– Housing Finance Companies regulated by National Housing Bank,

– Stock Exchange or a Mutual Benefit company

– It may also be mentioned that Mortgage Guarantee Companies have been notified as Non-Banking Financial Companies under Section 45 I(f)(iii) of the RBI Act, 1934. Core Investment Companies with asset size of less than ₹ 100 crore, and those with asset size of ₹ 100 crore and above but not accessing public funds are exempted from registration with the RBI.

Types of NBFC’s

NBFCs Types / Classifications

| Classification / Type | Description | |

| Liabilities Based NBFCs | Deposit Non-Banking Financial Companies | – NBFCs that can accept deposits from the public, such companies are called Deposit NBFCs. |

| Non-Deposit Non-Banking Financial Companies | – NBFCs that cannot accept deposits from the public, such companies are called Non-deposit NBFCs | |

| Assets Size NBFCs | Systemically Important | – NBFCs whose asset size is of INR 500 crore or more as per last audited balance sheet are considered as systemically important NBFCs. |

| Non-Systemically Important | – NBFCs whose asset size is below INR 500 crore as per last audited balance sheet are considered as systemically important NBFCs | |

–

| Type | Description |

| Asset Finance Company (AFC) | – Financial institution carrying on as its principal business the financing of physical assets supporting productive/economic activity, such as automobiles, tractors, etc |

| Investment Company (IC) | – Financial institution whose principal business is that of acquisition of securities. |

| Loan Company (LC) | – Financial institution carrying on as its principal business of providing finance whether by making loans or advances or otherwise for any activity other than its own but does not include an AFC (Assest Finance Company). |

| Infrastructure Finance Company (IFC) | – It is a Non-Banking Financial company

> which deploys at least 75 per cent of its total assets in infrastructure loans > has minimum net owned fund of Rs. 300 Crores. > Has minimum credit rating of ‘ A ‘ or equivalent |

| Systemically Important Core Investment Company (CIC-ND-SI) | – CIC-ND-SI is an NBFC carrying on the business of acquisition of shares and securities which satisfies the following conditions:-

a) it holds not less than 90% of its Total Assets in the form of investment in equity shares, preference shares, debt or loans in group companies; b) its investments in the equity shares (including instruments compulsorily convertible into equity shares within a period not exceeding 10 years from the date of issue) in group companies constitutes not less than 60% of its Total Assets; c) it does not trade in its investments in shares, debt or loans in group companies except through block sale for the purpose of dilution or disinvestment; d) it does not carry on any other financial activity referred to in Section 45I(c) and 45I(f) of the RBI Act, 1934 except investment in bank deposits, money market instruments, government securities, loans to and investments in debt issuances of group companies or guarantees issued on behalf of group companies. e) Its asset size is ₹ 100 crore or above and f) It accepts public funds |

| Infrastructure Debt Fund: Non- Banking Financial Company (IDF-NBFC) – | a) IDF-NBFC is a company registered as NBFC to facilitate the flow of long term debt into infrastructure projects.

b) IDF-NBFC raise resources through issue of Rupee or Dollar denominated bonds of minimum 5 year maturity. c) Only Infrastructure Finance Companies (IFC) can sponsor IDF-NBFCs. |

| Non-Banking Financial Company – Micro Finance Institution (NBFC-MFI) – | “Non-Banking Financial Company – Micro Finance Institution (NBFC-MFI)” means a non-deposit taking NBFC (other than a company formed and registered under section 25 of the Companies Act, 1956 or Section 8 of the Companies Act, 2013) that fulfils the following conditions:

– Minimum Net Owned Funds of ₹ 5 crore. (For NBFC-MFIs registered in the North Eastern Region of the country, the minimum NOF requirement shall stand at ₹ 2 crore). – Not less than 85% of its net assets are in the nature of “qualifying assets.” |

| Non-Banking Financial Company – Factors (NBFC-Factors) – | a) NBFC-Factor is a non-deposit taking NBFC engaged in the principal business of factoring.

b) The financial assets in the factoring business should constitute at least 50 percent of its total assets and its income derived from factoring business should not be less than 50 percent of its gross income. |

| Mortgage Guarantee Companies – | MGC are financial institutions for which at least 90% of the business turnover is mortgage guarantee business or at least 90% of the gross income is from mortgage guarantee business and net owned fund is ₹100 crore. |

| NBFC- Non-Operative Financial Holding Company (NOFHC) – | It is a financial institution through which promoter / promoter groups will be permitted to set up a new bank. It’s a wholly-owned Non-Operative Financial Holding Company (NOFHC) which will hold the bank as well as all other financial services companies regulated by RBI or other financial sector regulators, to the extent permissible under the applicable regulatory prescriptions. |

| Systemically important non-deposit taking non-banking financial company – | It means a non-banking financial company not accepting / holding public deposits and having total assets of ₹ 500 crore and above as shown in the last audited balance sheet. |

| Mortgage Guarantee Companies – | MGC are financial institutions for which at least 90% of the business turnover is mortgage guarantee business or at least 90% of the gross income is from mortgage guarantee business and net owned fund is ₹100 crore. |

IMPORTANT ISSUES

> All NBFC are prohibited from granting loans against their own shares.

> NBFC Not to be partner in partnership firm.

Net owned fund’ in relation to NBFCs

Net Owned Fund’ is the amount as arrived at above, minus the amount of investments of such company in shares of its subsidiaries, companies in the same group and all other NBFCs and the book value of debentures, bonds, outstanding loans and advances including hire purchase and lease finance made to and deposits with subsidiaries and companies in the same group, to the extent it exceeds 10% of the owned fund.

Conclusion: As integral players in India’s financial ecosystem, NBFCs operate under the regulatory oversight of the Reserve Bank of India. Diverse in nature, they offer a range of financial services, from deposit-taking to asset financing. With stringent criteria and regulatory mandates, NBFCs contribute significantly to the country’s economic growth and financial stability.

Definition of Infrastructure debt fund has changed. Infrastructure finance company need not sponsor and IDF. Pls update

this NBFC classification is per which Act?