Summary: Sovereign Gold Bonds (SGBs) are government securities issued by the Reserve Bank of India on behalf of the Government of India, denominated in grams of gold. They offer an alternative to physical gold investments. Eligible investors include Indian residents such as individuals, HUFs, trusts, universities, and charitable institutions, with joint holdings and minor investments allowed under guardian application. The minimum investment is one gram, with maximum limits of 4 kg per individual or HUF and 20 kg per trust per fiscal year. SGBs bear a fixed annual interest rate of 2.50%, credited semi-annually. Redemption occurs in Indian Rupees based on the average gold price over the last three days, with early redemption allowed after five years. SGBs can be traded on stock exchanges if held in demat form, and can be gifted or transferred. Tax implications include tax-free redemption proceeds and exempt capital gains on maturity, while interest income is taxable. SGBs are also subject to capital gains tax depending on holding period and transfer method, with specific rules for stock exchange and direct transfers. Always consult a financial expert for personalized advice.

Page Contents

- 1. What are Sovereign Gold Bonds (SGBs)? Who is the issuer?

- 2. Who is eligible to invest in the SGBs?

- 3. Whether joint holding will be allowed?

- 4. Can a Minor invest in SGB?

- 5. What is the minimum and maximum ceiling limit for investment in SGB?

- 6. What is the rate of interest and the method of payment of interest?

- 7. What is the procedure for redemption?

- 8. Is premature redemption of SGB allowed?

- 9. Whether the bonds can be gifted to a relative or friend on some occasion?

- 10. What are the tax implications on i) interest and ii) capital gain?

- 11. Is tax deducted at source (TDS) applicable on the bond?

- 12. How to trade these bonds?

- 14. Taxability of SGBs Explained:

1. What are Sovereign Gold Bonds (SGBs)? Who is the issuer?

- SGBs are government securities denominated in grams of gold.

- They substitute physical gold..

- The Bond is issued by Reserve Bank on behalf of Government of India.

2. Who is eligible to invest in the SGBs?

- Persons resident in India as defined under Foreign Exchange Management Act, 1999 are eligible to invest in SGB.

- Eligible investors include

- individuals,

- HUFs,

- trusts,

- universities and

- Charitable institutions.

- Individual investors with subsequent change in residential status from resident to non-resident may continue to hold SGB till early redemption/maturity.

3. Whether joint holding will be allowed?

Yes, joint holding is allowed.

4. Can a Minor invest in SGB?

Yes. The application on behalf of the minor has to be made by his/her guardian.

5. What is the minimum and maximum ceiling limit for investment in SGB?

- For Individuals and HUFs: Minimum investment in the Bond shall be one gram with a maximum limit of 4 kg for individuals and Hindu Undivided Family (HUF) and

- 20 kg for trusts and similar entities notified by the government from time to time per fiscal year (April – March).

- In case of joint holding, the limit applies to the first applicant.

6. What is the rate of interest and the method of payment of interest?

- The Bonds bear interest at the rate of 2.50 per cent (fixed rate) per annum on the amount of initial investment.

- Interest will be credited semi-annually to the bank account of the investor and the last interest will be payable on maturity along with the principal.

7. What is the procedure for redemption?

- On maturity, the Gold Bonds shall be redeemed in Indian Rupees and

- the redemption price shall be based on simple average of closing price of gold of 999 purity of previous 3 business days from the date of repayment, published by the India Bullion and Jewelers Association Limited.

8. Is premature redemption of SGB allowed?

- Though the tenor of the bond is 8 years,

- However, early encashment/redemption of the bond is allowed after fifth year from the date of issue on coupon payment dates.

- The bond will be tradable on Exchanges, if held in demat form. It can also be transferred to any other eligible investor.

9. Whether the bonds can be gifted to a relative or friend on some occasion?

- The bond can be gifted/transferable to a relative/friend/anybody who fulfills the eligibility criteria

- The Bonds shall be transferable in accordance with the provisions of the Government Securities Act 2006 and the Government Securities Regulations 2007 before maturity by execution of an instrument of transfer which is available with the issuing agents.

10. What are the tax implications on i) interest and ii) capital gain?

- Interest on the Bonds will be taxable as per the provisions of the Income-tax Act, 1961 (43 of 1961).

- The capital gains tax arising on redemption of SGB has been exempted For Individuals.

- The indexation benefits will be provided to long terms capital gains arising to any person on transfer of bond.

11. Is tax deducted at source (TDS) applicable on the bond?

- TDS is not applicable on the bond.

- However, it is the responsibility of the bond holder to comply with the tax laws.

12. How to trade these bonds?

- The bonds are tradable from a date to be notified by RBI. (It may be noted that only bonds held in de-mat form with depositories can be traded in stock exchanges) The bonds can also be sold and transferred as per provisions of Government Securities Act, 2006.

- Partial transfer of bonds is also possible

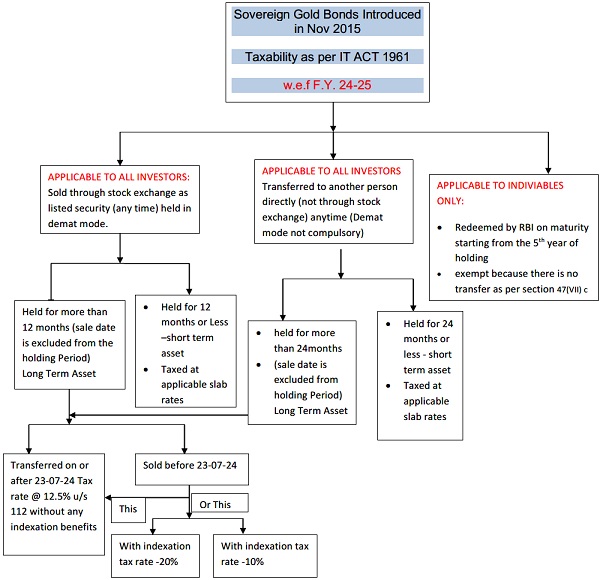

14. Taxability of SGBs Explained:

Sovereign Gold Bonds (SGBs) issued by the Government of India can indeed be taxed in various ways, depending on the nature of the transaction. Here’s a detailed look at the tax implications for each scenario (applicable w.e.f. FY 24-25):

1. Transfer through Stock Exchange (applicable to all types of investors)

When Sovereign Gold Bonds are sold on the stock exchange:

- Capital Gains Tax: The gains made from selling SGBs on the stock exchange are considered capital gains. The tax treatment depends on the holding period.

- Short-Term Capital Gains (STCG): If the bonds are held for 12 months or less, the gains are taxed as short-term capital gains (date of transfer is excluded from holding period in all cases). These are taxed at the individual’s applicable income tax slab rate.

- Long-Term Capital Gains (LTCG): If the bonds are held for more than 12 months, the gains are considered long-term. Long-term capital gains on SGBs.

- In this scenario there can be two options with the investor:

- SGBs are transferred after 23/07/2024, then tax rate is 12.5% without indexation ( new regime)

- SGBs are transferred before 23/07/2024,then the investor has the option of either opting new regime mentioned above or

- Alternatively, He can opt for old regime, which is 20% tax rate with indexation and 10% without indexation.

- In this scenario there can be two options with the investor:

2. Direct Transfer (Sale to another person) (applicable to all types of investors)

When SGBs are transferred directly to another person (outside of the stock exchange):

- Capital Gains Tax: The tax treatment is similar to that of transfer through the stock exchange.

- Short-Term Capital Gains (STCG): If the bonds are held for 24 months or less, the gains are taxed as short-term capital gains. These are taxed at the individual’s applicable income tax slab rate.

- Long-Term Capital Gains (LTCG): If the bonds are held for more than 24 months, the gains are considered long-term. Long-term capital gains on SGBs.

- In this scenario there can be two options with the investor:

- SGBs are transferred after 23/07/2024, then tax rate is 12.5% without indexation ( new regime)

- SGBs are transferred before 23/07/2024,then the investor has the option of either opting new regime mentioned above or

- Alternatively, He can opt for old regime, which is 20% tax rate with indexation and 10% tax rate without indexation.

- In this scenario there can be two options with the investor:

3. Redemption by RBI (Applicable to Individuals Only)

When SGBs are redeemed at maturity (which is typically after eight years, with an option for early redemption after the fifth year):

- Tax on Interest Income: The interest income earned on SGBs is taxable. This means that the annual interest of 2.5% p.a. paid on SGBs is added to the income of the investor under the head income from other sources.

- Tax on Redemption Proceeds: The redemption amount received upon maturity is tax-free. The principal amount and the final redemption value, which includes the appreciation in value, are not subject to tax.

Summary

- Stock Exchange Transfer: Taxed as capital gains—STCG or LTCG based on the holding period.

- Direct Transfer: Taxed similarly to stock exchange transfer—STCG or LTCG.

- Redemption by RBI: Tax-free

Imp note: Always consult with a tax advisor or financial expert to ensure compliance with the latest tax regulations and to receive personalized advice based on your specific situation

****

The author is a Lucknow based Chartered Accountant and can be reached at bhu7900@gmail.com. His Youtube channel #bhupeshacc can be visited for better understanding of the topic.

When SGB holder dies after hoolding period of 4 yr to 5yr and bonds are transferred to the nominee. whether the deacsed income is laible for Capital Gain Tax ? any tax imlication in the hand of nominee at the time of transfer or time of sale in market before maturity. ( what would be the acquisition cost if nominee sell it in market after transfer to his name but before maturity. Thanks.

Thanks for explaining comprehensively.

My question is, that since interest on SGB is not reflecting in AIS/TIS, so should it be shown Under head – Income from other sources by mentioning “Interest on Sovereign Gold Bonds” in ITR form?

Thanks & regards

please check the below link

https://www.axisbank.com/progress-with-us-articles/investment/demat-trading/sovereign-gold-bonds-taxation

It says even redemption is exempt for HUF and others

Kindly check and reply.

hi

Kindly check and reply on SGB redemption on taxabliity to HUF

hi

Awaiting your reply. Please check previous query . LTCG on HUF. You said there is a capital gain, wherein the link says, no LTCG for HUF

axisbank.com/progress-with-us-articles/investment/demat-trading/sovereign-gold-bonds-taxation

Your details reply, Would helpful to me

Dear Sir,

Please refer to the author’s opinion expressed in the comments and the article. The author stands by the content published in the article. You may consider raising your query directly with the Axis Bank portal for further clarification.

According to Section 47(vii) of the Income Tax Act, the redemption of Sovereign Gold Bonds (SGB) by an individual with the Reserve Bank of India is not considered a transfer and therefore does not result in any capital gains for the individual.

“The indexation benefits will be provided to long terms capital gains arising to any person on transfer of bond.”

Q. If redemption to HUF – tax treatment please. Hope Redemption is not a transfer. Because, it says for redemption to individual is tax free. For HUF also redemption done by RBI

The redemption of a Sovereign Gold Bond (SGB) by an individual is exempt from capital gains tax. This exemption applies to both bonds redeemed at maturity and those redeemed early after five years.

Explanation

The redemption of an SGB is not considered a transfer under the Income Tax Act.

The profits from redeeming an SGB are not considered income.

You do not need to include the redemption of an SGB in your ITR.

However, if you sell an SGB on a stock exchange or transfer it privately, the profits will be subject to capital gains tax. The tax rate depends on how long you held the bond.

If you sell the bond within one year, the profits are taxed at your individual’s slab rate.

If you sell the bond after one year, the profits are taxed at a rate of 12.50%.

You can also earn interest on an SGB, which is taxable as income. The interest income is taxed based on your income tax bracket.

Q. related to HUF – SGB redemption done by RBI. Capital gain apply or not for HUF. Because it clearly says individual no capital gains, if CG applicable, indexation applicable or not

HuF case. SGB are fully taxable upon transfer. no exemption

in case of sale on or after 23.7.24 no indexation benefit shall be available.

long term 12.5% rate shall apply

Thanks for your reply. For huf LTCG on SGB, 1.25 basic exemption available or not

HI

Awaiting your reply on For huf LTCG on SGB, 1.25 basic exemption available or not

CG falls under Which Income Tax section (112, 111. etc

exemption of Rs. 1.25 lakh is available u/s 112A

Applicability of Section 112A

Capital gain tax under section 112A will be levied only if the below-mentioned conditions are fulfilled:

Sale must be of equity shares or units of an equity-oriented mutual fund or units of a business trust.

The securities should be long-term capital assets i.e. should have been held for more than 12 months.

Only the capital gains exceeding Rs. 1,25,000 will be taxed.

The transactions of purchase and sale of equity shares are subject to STT (Securities Transaction Tax). In the case of equity-oriented mutual fund units or business trusts, the transaction of the sale is liable to STT.

so the SGBs are clearly outside the scope of section 112A.hence, HUFs will have to pay tax on LTCG on the full amount of LTCG, no matter what.

hope your query is satisfied.

Highly informative , simple and clear. Very much useful for the retail investors like me.

Thanks for your encouraging compliments.

What is SGBs are held by a private limited company till maturity and proceeds are received by company on redemption by RBI on maturity? Will this be taxable? If yes, what will be the tax implication?

Please refer point no 2 of the article-who is eligible for investment and you will find that pvt limited companies except section 8 companies are ineligible for investment further only individuals are exempt from tax on redemption of SGBs

Very clear and crisp description of SGB tax treatment. Please enlighten us on taxability under LTCG on equity and Immovable assets post budget 2024.

Very informative and beautifully explained……

Very insightful and comprehensive……. Explained in lucid way….

Thread bare analysis of SGB. All aspects clearly explained.

comprehensively explained. No doubt left. Please post regularly and benefit us. 🙏

Very informative, well written. Detailed description give us clear knowledge.

Sir very informative u have expertly solve the problem will talk to u in person

I is a good investment scheme by th RBI.

In the current budget, the customs duty on Gold was substantially reduced bringing down the Gold prices by few thousand rupees.

This was basically done because more than 30 such Gold Bonds schemes are due to either redemption or ealry redemption in the coming 6 months.

This would entail haeavy payments for the Government. The Gold prices have more than doubled in since the time these bonds wer intially issued in 2016, 2017, 2018.

To reduce this redemption burden, the Government smartly reduced the Customs duty on Gold so as to reduce the gold prices and thus reduce the redemtion amounts.

The scheme per se is very good if held till maturity as the full redemtion proceeds shall be tax free for the investors.

Very beautifully explained about each concept in language that is easy to understand

what if we buy SGBs from secondary market(stock exchange), what are the tax implications on them?

are they tax free on maturity even if we buy just 1-2 months before it’s maturity period (e.g. 7years and 10 months from launch)

the redemption from RBI remains tax free no matter what, in the case of individuals. so even if you buy 2 months prior to maturity date from stock exchange the redemption

amount from RBI goes into tax free bracket.

Each and everything about SGB is explained in lucid way…very insightful.

A Complete guidance on Gold Bond purchase limits, eligibility, criteria, interest, Lock-in, Value of encashment etc.

It’s hightime to invest in Sovereign Gold Bonds.

An Exhaustive Coverage on SCB in very simple way. Gold and valuable Content