Overview of Section 9B

Section 9B of the Income Tax Act, 1961 has been inserted vide Finance Act, 2021. It provides for taxation of Income on receipt of capital asset or stock in trade by the specified person from the specified entity. The section creates a deeming fiction that whenever there is a transfer by a specified entity to specified person any capital asset or stock in trade then profits and gains on such transfer shall be chargeable in hands of specified entity as Capital gains or Profits and Gains of Business or Profession (PGBP).

- Specified entity referred to in this section means Firm or other Association of persons (AOP) or Body of individuals (BOI) (Not being a company or co-operative society).

- Specified Person referred to in this section means a person who is a Partner of a firm or Member of other Association of persons or Body of individuals (not being a company or a co-operative society) in any previous year.

Provisions of Section 9B

Subsection (1) of section 9B

Where a specified person receives during the previous year any capital asset or stock in trade or both from a specified entity in connection with the dissolution or reconstitution of such specified entity, then the specified entity shall be deemed to have transferred such capital asset or stock in trade or both, as the case may be, to the specified person in the year in which such capital asset or stock in trade or both are received by the specified person.

Subsection (2) of section 9B

Any profits and gains arising from such deemed transfer of capital asset or stock in trade or both, as the case may be, by the specified entity shall be—

- deemed to be the income of such specified entity of the previous year in which such capital asset or stock in trade or both were received by the specified person; and

- chargeable to income-tax as income of such specified entity under the head “Profits and gains of business or profession” or under the head “Capital gains”, in accordance with the provisions of this Act.

Subsection (3) of section 9B

For the purposes of this section, fair market value of the capital asset or stock in trade or both on the date of its receipt by the specified person shall be deemed to be the full value of the consideration received or accruing as a result of such deemed transfer of the capital asset or stock in trade or both by the specified entity.

Subsection (4) of section 9B

If any difficulty arises in giving effect to the provisions of this section and sub-section (4) of section 45, the Board may, with the approval of the Central Government, issue guidelines for the purposes of removing the difficulty.

Subsection (5) of section 9B

Every guideline issued by the Board under sub-section (4) shall, as soon as may be after it is issued, be laid before each House of Parliament, and shall be binding on the income-tax authorities and on the assessee.

Analysis of provisions of Section 9B

Section 9B provides that whenever there is a dissolution or reconstitution of the specified entity and as a result of such dissolution or reconstitution specified entity transfers to specified person any capital asset or stock in trade or both then such transfer shall be deemed to be taken place by the specified entity to specified person in the year in which such transfer took place. Income arising on such transfer shall be chargeable in the hands of specified entity as Capital Gains or PGBP.

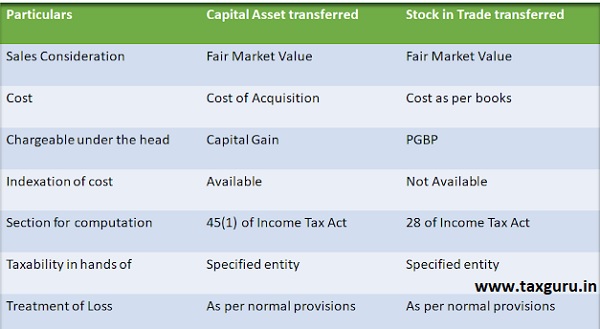

Consideration for such transfer shall be the Fair market value (FMV) of capital asset or stock in trade on the date when such stock in trade or capital asset is received by the specified person from the specified entity.

How Income Tax will be calculated

Going by the provisions of sub-section (2) of section 9B it is clearly mentioned that tax will be calculated in accordance with the provisions of this act. Accordingly一

- If specified entity transfers any capital asset to specified person then the Income tax will be calculated in accordance with provisions of sub-section (1) of section 45 of the income tax act. That is we will take FMV of capital asset as sales consideration and cost of acquisition and cost of improvement shall be taken as per the books of the specified entity. Indexation shall also be available and any loss arising on such transfer shall also be allowed to set off and carried forward in accordance with provisions of the act.

- If specified entity transfers any stock in trade to specified person then the Income tax will be calculated in accordance with provisions of section 28 of the income tax act. That is we will take FMV of stock in trade as sale value and cost of stock shall be as per the books of the specified entity. Any loss arising on such transfer shall also be allowed to set off and carried forward in accordance with provisions of the act.

Important Note: All the above calculations shall be made in the hands of specified entity and there will be no tax consequence in the hands of specified person on such transfer.

Example relating to Section 9B

Let’s suppose there are three partners in firm “FR” namely “A”, “B” and “C”. Capital balance of each partner is Rs.10 lakhs. There are three pieces of land ‘S’, ‘T’ and ‘U’ at a book value of Rs.10 lakhs each.

Partner ”A” decides to exit the firm for which he will be paid Rs.11 lakhs and shall also be given land ‘U’. FMV of land ‘U’ on such date is Rs.50 lakhs. Let’s assume Indexed cost of acquisition of land ‘U’ is Rs.15 lakhs.

Assuming land ‘U’ is a long term capital asset the long term capital gain arising on such transfer shall be Rs.35 lakhs [FMV of Rs.50 lakhs (-) Indexed cost of acquisition of Rs.15 lakhs]. Firm “FR” needs to pay long term capital gain tax of Rs.7 lakhs [ Rs.35 lakhs X 20% tax rate] ignoring surcharge and cess.

I would like to apply for my income tax return and cannot get no help to do it online how can I get some help please

Connect or share the detail on the below mentioned e mail

Kuldeepsassociates@gmail.com