CA Aditya Surana, CA Aruna R

Introduction

Any business before commencing its business incurs various expenditure, the most common ones being feasibility, marketing, brokerage for office/ work premise searching, rentals for place, salaries to staff, funding of the project etc. These expenses though incurred much before the commencement of business are very vital for carrying out the business. Generally, all expenses incurred should get a tax deduction while computing taxable income for arriving at tax liability. However, expenses which are incorporated before the commencement of business may not be eligible for tax deduction and hence it could imply spending hefty sums of money for setting up business and yet not being able to claim a tax deduction for the same, i.e. loosing cash to the extent of 25-30% (assuming it’s a corporate form of entity or LLP or individuals/ others at highest slab of income) of the amount of such expenditure. Since capital is the life and blood of any business especially a newly set up one, 25-30% dent in the working capital is a huge blow and naturally a businessman would like to explore all provisions under the law which can allow him to reduce his taxable income by deducting all or atleast some of these pre-commencement expenditure.

Hence, we thought of penning this article due to the importance of pre-commencement expenditure which is often ignored looking at the stage and size of the business, or at time due to sheer ignorance of the applicable provisions in tax law. Also, the fact that there are varied interpretations concerning tax deduction with regard to ‘commencement date’, ‘set up date’, ‘pre-operative expenditure’, mode of computation and others.

Page Contents

Preliminary expenses/Pre-incorporation expenses vs. Pre-operative expenses

There is a primary difference between the preliminary and preoperative expenses. Preliminary Expenses / Pre-incorporation expenses are those expenses incurred prior to incorporation of the LLP. Pre-operative expenses are incurred after incorporation of business but before commencement of business operations.

As per Income Tax Act, 1961 (‘the Act’), the concept of date of setting up of a business and the date of commencement of operations are the same. The date of incorporation is not the date of set up as per the Income Tax act. All expenses incurred for the purpose of business will be allowed under Profits and Gains from Business or Profession after the business is as per the Income Tax act. The debate here is where pre-operative expenses are incurred for the purpose of business. While a lay man would say yes, from a tax law perspective, an expenses would be considered to have been incurred for the purpose of business if first of all the business is in existence when the expenditure was incurred. We have in the subsequent slides discussed with reference to judicial precedents of when a business can be considered to be in existence. There is no standard norm for this and depends on facts and circumstances of each case. Hence, each case is unique and needs to be studied with the knowledge of precedents and law in the hindsight.

However, there are expenses which are incurred necessarily to set up the business if not ‘for the business’ in a tax technical interpretation as explained above. The legislature also realised this and hence introduced section 35D in the Act which provides deduction to not all the pre-operative expenses, but to certain such expenses. Such expenses are eligible for amortisation over a period of 5 years from the year in which the business is commenced/ set up or from the year in which an existing business is extended. Now what may be termed as extended also needs to be reviewed from the eyes of a businessman with the tax law and judicial precedents in the hindsight. Factors such as the volume of expansion, investment, projected revenue when compared to existing business, employment generation, licensing and premise requirement will be key indicators amongst others.

The essentials of Section 35D

As per S.35D of the Act, 1/5th of the preoperative expense can be claimed as deduction beginning with the ‘previous year’ in which the business commences or the extension of the undertaking is completed or the new unit commences operation. Only specific expenses are eligible to be claim under section 35D as under:

Eligible expenditure under Section 35D

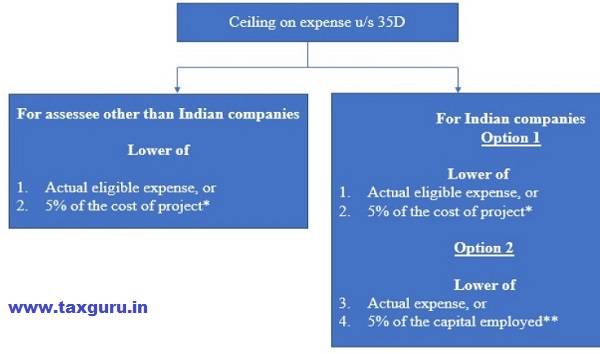

Computation of quantum of eligible expense u/s 35D

* Cost of project = The actual cost of the fixed assets, being land, buildings, leaseholds, plant, machinery, furniture, fittings and railway sidings (including expenditure on development of land and buildings), which are shown in the books of the assessee as on the last day of the previous year in which the business of the assessee commences / in which the extension of the undertaking is completed / the new unit commences production or operation in so far as such fixed assets have been acquired or developed in connection with the extension of the undertaking or the setting up of the new unit of the assessee

** Capital employed = The aggregate of the issued share capital, debentures and long-term borrowings as on the last day of the previous year in which the business of the company commences/ in which the extension of the undertaking is completed / the new unit commences production or operation in so far as such fixed assets have been acquired or developed in connection with the extension of the undertaking or the setting up of the new unit of the assessee

Other conditions

1. The accounts of the assessee for the years in which eligible expenses are incurred should be audited by a Chartered Accountant and the same should be furnished along with the Income tax returns for the first year in which deduction is claimed.

2. If accounts are not audited, then the audit report in Form 3AE shall be obtained from the Chartered Accountant and filed as prescribed above.

3. The expense claimed cannot be claimed under any other section in same or anyother AY.

Deduction under Section 35D in special situations

If amalgamation or demerger (in respect of any undertaking in respect of which Section 35D is claimed) happens before 5 successive years, then the deduction is made as follows:

Deduction under Section 35D in special situations

Ambiguities on the date of commencement -Untying the knots

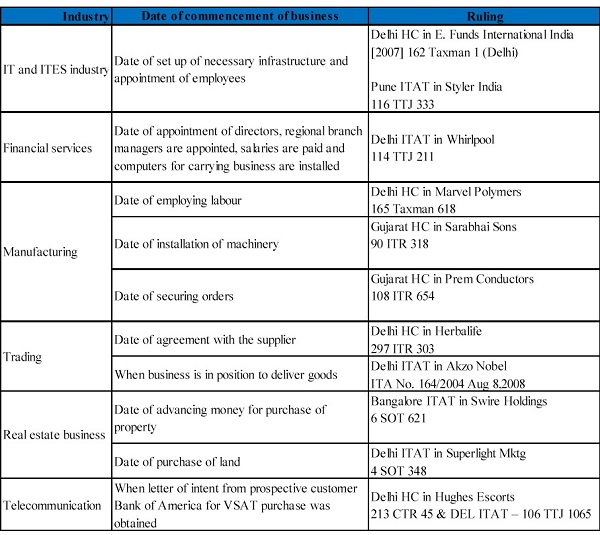

There has always been a debate as to what date should be considered as the date of set up in Income tax act. This is purely based on facts of each case and from industry to industry. We can draw support from various judgements discussed below to conclude the date of the commencement of business.

So for each business, the date of events should be clearly recorded so as to determine the date of commencement of business.

What is the conclusion?????