Introduction

Earlier, TDS was not applicable on partner’s remuneration, interest, commission etc. However, TDS was applicable on payments made to employees by firms. A new Section 194T (Payments to partners of firms) for TDS deduction proposed as per Clause 62 of the Finance (No. 2) Bill, 2024, which expands the scope of TDS to include payments made by firms to its partners.

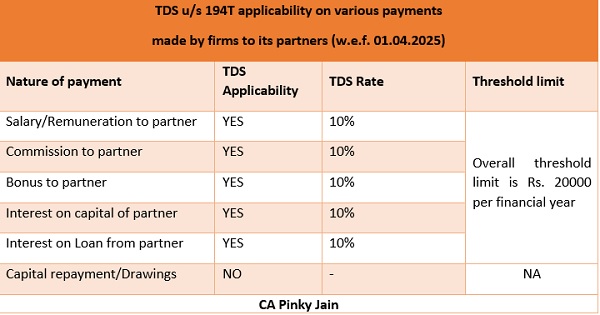

Applicability of TDS u/s 194T

Effective from 1st April, 2025, Section 194T mandates TDS deduction on various payments made by firms (Partnership firms or LLP) to its partners. These payments include salary, remuneration, commission, bonus, and interest on any account.

Important Note: TDS is not applicable on the drawings or capital repayment to partners. But TDS applicable on interest on capital or loan from partner.

TDS Rate and Threshold Limit

| Section | TDS Rate | Threshold Limit |

| 194T: Payments to partners by firm (Partnership firm or an LLP) | 10% | Rs. 20000 per financial year |

Firms are required to deduct TDS at a rate of 10% on payments made to partners if the aggregate amount exceeds Rs. 20,000 in a financial year.

Please note that TDS will be applicable on whole amount if aggregate exceeds the threshold limit.

For instance, if a partnership firm/LLP pays Rs. 5,00,000 to a partner as remuneration in a financial year, the TDS under Section 194T would amount to Rs. 50,000 (i.e., 10% of Rs. 5,00,000).

When to Deduct TDS u/s 194T?

The TDS is to be deducted at the earliest of the following dates:

- Credit to the account (including capital account) of partner in the books of the firm or

- Payment to the partner

Whether TDS u/s 194T applicable on an LLP?

Yes, Section 194T is applicable to firms, including partnership firms and LLPs.

As per Section 2(23)(i) the Income Tax Act, 1961, “firm” shall have the meaning assigned to it in the Indian Partnership Act, 1932 (9 of 1932), and shall include a limited liability partnership as defined in the Limited Liability Partnership Act, 2008 (6 of 2009).

As per Section 2(23)(ii) the Income Tax Act, 1961, “partner” shall have the meaning assigned to it in the Indian Partnership Act, 1932 (9 of 1932), and shall include,—

(a) any person who, being a minor, has been admitted to the benefits of partnership; and

(b) a partner of a limited liability partnership as defined in the Limited Liability Partnership Act, 2008 (6 of 2009)

Why TDS u/s 192 not applicable on partners salary or remuneration?

As per Explanation 2 of Section 15 of Income Tax act for Salaries: Any salary, bonus, commission or remuneration, by whatever name called, due to, or received by, a partner of a firm from the firm shall not be regarded as “salary” for the purposes of this section. Hence, no TDS liability was there on partner’s salary or remuneration u/s 192.

Conclusion

In summary, Section 194T represents India’s ongoing effort to modernize tax laws, enhancing transparency and accountability in financial transactions between firms and their partners. The introduction of Section 194T marks a departure from previous norms where TDS was not applicable on partner payments, now extending to both partnership firms and LLPs.

Author Bio

please guide whether Tax to be deducted on payments made prior to 23.07.2024 when the President gave approval to Finance Act. if yes’ how to pay on such payments

1. If remuneration will be credited monthly to partners capital account then it means TDS will be deducted monthly.

2. Any withdrawals from partners capital account for monthly expenses, will not be liable for TDS deduction.

3. It’s sure that the new provision is effected from 01/04/2025.

please confirm.

Budget 2024 introduces reductions in the TDS rates for specific payments to foster business operations and improve compliance among taxpayers. These changes are set to take effect on either October 1, 2024 or April 1, 2025.

The provisions of Section 194T is applicable w.e.f. 1st April, 2025 viz. from AY 2025-26. But this article misleads to its applicability from current FY 2024-25 itself, which is not correct according to me.

Author may kindly clarify this issue.

CA. Dilip Khetan, Gorakhpur

Dear Sir,

Please note that TDS under sec 194T @ 10% takes effect from 01.04.2025 as per Budget 2024. This is consistent with other sections like 194H, 194IB, and 194M etc. which also specify clear effective date i.e 01.10.2024. Unlike ITR provisions, TDS regulations require adherence to specific effective dates unless the department provides clarification.

So in case of sec 194T, we understand that it is applicable from the exact date i.e 01.04.2025. There is no guidance from the department indicating that this should be applied starting from AY 2025-26. As with TDS, the focus is on the exact date of applicability rather than the AY or FY.

I hope this clarifies the issue. If you need any further clarification, please feel free to reach out. I would be happy to discuss it further.

If i pay 12 lacs as remuneration to a partner and TDS not deduced. TDS deducted not paid. in both cases, shall i eligible to claim partner`s salary u/s 40(b) the maximum limit for partner`s remuneration?

In case remuneration is paid to the partner of the partnership firm on or before 23.07.2024 before the date of newly inserted section 194T, whether the TDS is applicable thereon and if so, when to be deducted and deposited in the Govt. treasury, since the payments are made without deduction of TDS also whit is the implication of Interest and penalty thereon.

This provision will not benefit ITD, as in case of more than 99% partners pay advance Income Tax on Diffrent dates taking into account salary, interst etc from the Firm, whereass now TDS will be deducted normally at Year end (These are provided generally at Year end)

But say remuneration is decided while closing of books of accounts so time of TDS etc is difficult as on 31st March. Interest will be levied for late deduction