Case Law Details

ACIT Vs Krishna Kanth Amand (ITAT Hyderabad)

Summary: The ITAT Hyderabad dismissed the Revenue’s appeal and upheld the CIT(A)’s order deleting an addition of ₹2.36 crore made under Section 69 of the Income-tax Act on account of alleged unexplained investment in purchase of immovable property. The Assessing Officer had relied solely on a seized loose sheet (Page-24 of Annexure A/LA/RES/01) recovered during a search on the seller, alleging that the assessee had paid on-money over and above the registered sale consideration. The Tribunal found that no independent or corroborative evidence was produced to establish any cash payment. It also noted that the same seized document had already been held to be a “dumb document” in the seller’s case as well as in the case of the co-purchaser, and the additions based on it had been deleted. Referring to judicial precedents, the Tribunal held that a standalone uncorroborated document could not displace the registered sale deed. Accordingly, the Revenue’s appeal was dismissed and the assessee’s cross-objection was allowed.

Core Issue: Whether an addition of Rs. 2.36 crore under section 69 for unexplained investment in purchase of immovable property could be sustained solely on the basis of a seized loose sheet allegedly evidencing payment of on-money, when no corroborative evidence was brought on record by the Revenue.

Facts of the Case: A search under section 132 was conducted in the case of the Yashoda Group, which led to a subsequent search on Dr. Amidyala Lingaiah. During the search, a loose sheet marked as Page-24 of Annexure A/LA/RES/01 was seized. Based on the entries recorded therein, the Assessing Officer alleged that the assessee, Shri Krishna Kanth Amand, had purchased a plot measuring 454.50 square yards at Kanteshwar, Nizamabad, from Dr. Lingaiah at Rs. 52,000 per square yard for a total consideration of Rs. 2,36,34,000.

The registered sale deed, however, reflected consideration of only Rs. 27,27,000 paid through banking channels. The AO interpreted the seized paper as indicating that the balance amount of approximately Rs. 2.09 crore had been paid in cash as on-money. Accordingly, proceedings under section 153C were initiated and an addition of Rs. 2,36,34,000 was made under section 69 as unexplained investment.

The assessee denied having paid any amount over and above the consideration recorded in the registered sale deed and contended that the entire addition was based solely on an unverified loose sheet.

Findings of the Assessing Officer

The AO held that:

The seized document was recovered from the premises of the seller and therefore could not be ignored.

The property details, survey numbers and measurements mentioned in the loose sheet matched the property purchased by the assessee.

The cheque payments mentioned in the loose sheet corresponded with the consideration recorded in the registered sale deed

Therefore, the remaining amount reflected in the seized paper represented cash consideration paid by the assessee.

Based on these observations, the AO treated the entire amount of Rs. 2,36,34,000 as unexplained investment under section 69.

Findings of the CIT(A)

The CIT(A) deleted the addition after recording that:

No evidence whatsoever had been gathered to establish actual payment of cash by the assessee.

No statement of the seller or purchaser admitting receipt or payment of on-money was available.

No cash trail, bank withdrawals, seized cash records, diary entries, confirmations or corroborative material had been brought on record.

The addition rested entirely on a loose sheet whose evidentiary value had already been doubted in connected proceedings.

The CIT(A) further noted that identical additions made in the hands of the seller, Dr. Lingaiah, based on the same document, had already been deleted and such deletion had been affirmed by the Tribunal.

ITAT Findings

The Tribunal upheld the order of the CIT(A) and dismissed the Revenue’s appeal.

The Tribunal observed that the AO had relied exclusively upon the contents of a loose sheet without producing any independent evidence to substantiate the allegation of payment of on-money. Mere existence of figures on a seized paper could not establish that the assessee had actually paid the amount mentioned therein.

A significant factor considered by the Tribunal was that the same document had already been examined in the case of the seller, Dr. Lingaiah. In that case, additions based on the document were deleted after the document was held to be a “dumb document” lacking evidentiary value. The Tribunal had affirmed that finding.

The Tribunal further noted that similar additions made in the case of the co-purchaser, Rutuja Projects, had also been deleted and the Revenue’s appeal had recently been dismissed.

According to the Tribunal, once a document has been judicially held to be a dumb document in respect of the same transaction, it would be impermissible to rely upon that very document to sustain an addition in the hands of another participant in the same transaction, particularly in the absence of any corroborative evidence.

Reliance on Judicial Precedents

1. Paramjit Singh v. ITO. The Tribunal relied upon the principle that the consideration recorded in a registered sale deed carries significant evidentiary value and cannot be displaced merely by oral assertions, assumptions, hearsay evidence or unsubstantiated documents. Unless strong and credible evidence establishes otherwise, the contents of the registered document must prevail.

2. PCIT v. Tarun Kumar Goyal. The Tribunal also relied upon the decision holding that additions based solely on uncorroborated dumb documents are unsustainable in law. A loose sheet, without supporting evidence, cannot constitute sufficient material for making additions.

3. ACIT v. Sri Lingaiah Amidyala. The Tribunal noted that in the seller’s own case, additions based on the same seized document had already been deleted and the document had effectively been treated as a dumb document.

Tribunal’s Conclusion

The Tribunal held that :

No evidence existed to prove actual payment of on-money by the assessee.

The registered sale deed reflected the consideration paid through banking channels.

The seized loose sheet was an uncorroborated dumb document.

The same document had already been rejected as a basis for addition in the seller’s case and in the co-purchaser’s case.

An addition under section 69 cannot be sustained merely on suspicion, conjecture or entries appearing in an unverified loose sheet.

Accordingly, the deletion of Rs. 2,36,34,000 made by the CIT(A) was upheld, the Revenue’s appeal was dismissed, and the assessee’s cross-objection was allowed.

Ratio Decidendi

A seized loose sheet or “dumb document” has no independent evidentiary value unless supported by corroborative evidence establishing the actual flow of unaccounted money. Where the consideration recorded in a registered sale deed is sought to be disregarded, the burden lies heavily on the Revenue to establish payment of on-money through reliable and independent evidence. In the absence of such evidence, no addition under section 69 can be sustained merely on the basis of entries found in a loose sheet, particularly where the same document has already been discredited in connected proceedings involving the seller and co-purchasers.

FULL TEXT OF THE ORDER OF ITAT HYDERABAD

The present appeal filed by the Revenue is directed against the order passed by the Ld. Commissioner of Income Tax (Appeals)-12, Hyderabad (for short, “CIT(A)”), dated 15/07/2025, which in turn arises from the order passed by the Assessing Officer (for short, “AO”) under section 153C of the Income Tax Act, 1961 (for short, “the Act”), dated 19/03/2024 for Assessment Year (AY) 2019-20. Also, the assessee is before us as a Cross-Objector. The revenue has assailed the impugned order on the following grounds of appeal:

“1. The Ld. CIT (Appeals) erred both in law and on facts of the case in granting relief to the assessee.

2. The Ld. CIT (Appeals) erred in deleting the addition made on account of unexplained investment u/s 69 of the IT Act of Rs. 2,36,34,000/- following the order of the Hon’ble Jurisdictional ITAT in the case of the Mr. Lijngaiah Amidyala for AY 2019-20 in ITA No. 702/Hyd/2022, dated 26.04.2023 which has not been accepted by the department.

3. The appellant craves leave to amend or alter any ground or add any other grounds which may be necessary.”

The assessee, on the other hand, has supported the CIT() order by raising the following cross-objections:

“1. The Order of the Ld.CIT(A)-12, Hyderabad has justified in allowing the appeal of the Assessee on merits.

2. The Ld. AO erred on the fact that the Ld. CIT (A) has rightly deleted the additions and allowed the Appeal of the Appellant after fairly considering the facts and submissions made before the Ld. CIT (A).

3. The Ld. AO has failed in appreciating the fact that the Ld. CIT(A) has correctly deleted the addition made based on a dumb document seized.

4. The Ld. AO has erred in considering the decision of Hon’ble ITAT in the case of Amidyala Lingaiah ITA: 702/Hyd/2022.

5. The Appellant craves to add/alter/modify any other grounds at the time of hearing.”

2. Succinctly stated, the assessee had filed his return of income for AY 201920 declaring an income of Rs.1,09,120/-.

3. Search and seizure operations were conducted in the case of Dr Amidyala Lingaiah, which in turn was an offshoot of a search conducted under section 153A of the Act on “Yashoda Group” on 22/12/2020.

4. During the course of the search proceedings conducted on Dr Amidyala Lingaiah (supra), the search officials had seized a loose sheet, viz., Page-24 of Annexure A/LA/RES/01, the contents of which apparently pertained to the assessee. Thereafter, the AO of the searched person, being satisfied that the information contained in the seized document, viz., Page-24 of Annexure A/LA/RES/01 pertained to Shri Krishna Kanth Amand, i.e., the assessee, and the same had a bearing on the determination of the latter’s income for AY 201819 to AY 2021-22, forwarded the seized material to the AO of the “other person” , i.e., the assessee, on 29.06.2022 who after recording a satisfaction note under section 153C of the Act, dated 29/06/2022 initiated proceedings and issued a notice to the assessee.

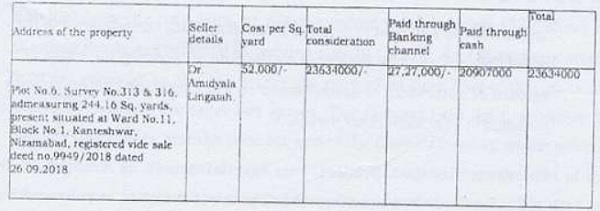

5. During the course of the assessment proceedings, the AO observed that the contents of the seized document, viz., Page-24 of Annexure A/LA/RES/01, inter alia, referred to the investment made by the assessee towards the purchase of a Plot No.6, Survey No 313 & 316, Block No. 1, Kanteshwar, Nizamabad admeasuring 454.50 sq yds (out of total area of 698.66 sq yds). The AO observed that based on the contents of the aforesaid seized document, the total consideration worked out to Rs. 2,36,34,000/-, wherein the amount as per the sale deed was Rs. 27,27,000/-, while the balance amount of Rs. 2,09,7000/-was paid in cash. The AO culled out the details of the subject property purchased by the assessee as under:

6. The AO, based on his aforesaid observations, called upon the assessee to explain as to why the purchase consideration of Rs. 2,36,34,000/- (supra) paid by him for purchasing the aforementioned property may not be considered as an unexplained investment under section 69 of the Act. In reply, the assessee submitted that he had purchased the subject immovable property from Dr Amidyala Lingaiah, but assailed the validity of the jurisdiction that was assumed by the AO for initiating proceedings under section 153C of the Act for the reason that the material seized did not belong to or relate to him. Apart from that, the assessee denied having made any cash payments and only accepted the payments made to the seller through the banking channel.

7. The AO, after deliberating on the explanation of the assessee, did not find favour with the same. It was observed by him that the seized document, viz., Page-24 of Annexure A/LA/RES/01, was seized from the premises of Dr Amidyala Lingaiah, i.e., the person from whom the assessee had admittedly purchased the land. The AO observed that it was not the case of the assessee that the material was seized from an unknown and unrelated third party. Also, it was observed by him that the 454.50 sq yds (out of the total land admeasuring 698.66 sq yds) purchased by the assessee from Dr Amidyala Lingaiah (supra), tallied with the area of land as mentioned in the seized document, viz., Page-24 of Annexure A/LA/RES/01. Further, it was observed that Dr Amidyala Linigaiah (supra) had, as per the registered sale deeds, stated to have sold the entire land of 698.66 sq yds for a consideration of Rs. 47,92,000/-, viz. (i) vide sale deed No. 9948/2018 to Shri Krishna Kanth Amandand, i.e., the assessee; and (ii). vide sale deed No. 9949/2018 to M/s Rutuja Projects and M/s. Shiva Balaji Associates. It was observed that the aggregate of the sale consideration paid by the above-mentioned parties to the seller through cheques, amounting to Rs. 47,92,000/-, was mentioned in the seized document, viz., Page-24 of Annexure A/LA/RES/01. Accordingly, the AO, based on the contents of the seized document, observed that the assessee had purchased the subject property from Dr Amidyala Lingaiah (supra) at Rs. 52,000/- per sq yd, for a total of Rs. 2,36,34,000/-. The AO, based on his aforesaid deliberations, concluded that the assessee had, during the subject year, made a total investment of Rs. 2,36,34,000/- towards the purchase of the aforementioned property. Thereafter, the AO, vide his order dated 19/03/2024 under Section 153C of the Act, determined the total income of the assessee at Rs. 2,46,54,984/,

8. Aggrieved, the assessee carried the matter in appeal before the CIT(A).

9. Ostensibly, the CIT(A) observed that the AO, except for relying on the contents of the seized document, viz., Page-24 of Annexure A/LA/RES/01, had failed to place on record any supporting evidence which would reveal that any on-money was paid by the assessee for purchasing the property admeasuring 454.50 sq yds from Dr Amidyala Lingaiah (supra). Also, the CIT(A) observed that based on the contents of the seized document, viz., Page-24 of Annexure A/LA/RES/01, the AO while framing the assessment in the case of the seller, viz., Dr. Amidyala Lingaiah (supra) had made an addition in his case by adopting the sale rate of the property @ Rs.52,000/- per sq yd, which, however was on an appeal in the latter’s case vacated by the CIT(A) on the ground that the seized document was a “dumb document” and no independent material was placed on record by the AO to support his conviction that any on-money was received from the purchasers. The CIT(A) further observed that the Revenue being aggrieved with the order of the CIT(A) in the case of Dr. Amidyala Lingaiah (supra) had carried the matter in appeal before the Tribunal, which vide its order passed in the case of ACIT, Central Circle-2(2), Hyderabad vs. Sri Lingaiah Amidyala in ITA No.702/Hyd/2022, dated 26/04/2023 had approved the CIT(A) order and dismissed the appeal filed by the Revenue.

10. The CIT(A) based on his aforesaid observations, viz., (i) that the AO while framing the assessment in the case of the assessee had failed to place on record any independent material which would support his conviction that any on-money, i.e., amount over and above the sale consideration recorded in the registered sale deed was paid by the assessee for purchasing the subject property, i.e., 454.50 sq yds from Dr. Amidyala Lingaiah (supra); and (ii) that the addition made based on the contents of the same seized document, viz., Page-24 of Annexure A/LA/RES/01 was vacated by the CIT(A) while disposing the appeal in the case of Dr. Amidyala Lingaiah (supra), which order had thereafter been approved by the Tribunal vide its order passed in the case of ACIT, Central Circle-2(2), Hyderabad vs. Sri Lingaiah Amidyala in ITA No.702/Hyd/2022, dated 26/04/2023, vacated the addition made by the AO.

11. The Revenue, being aggrieved with the order of the CIT(A), has carried the matter in appeal before us.

12. We have heard the Learned Authorised Representatives of both parties, perused the orders of the authorities below and the material available on record, as well as considered the judicial pronouncements that have been pressed into service by them to drive home their respective contentions.

13. Ms Uppaluri Meena, Learned Senior Departmental Representative (for short, “Ld. Sr-DR”), relied upon the assessment order.

14. Per contra, Shri C. Maheshwar Reddy, CA, Learned Authorised Representative (for short, “Ld. AR”) for the assessee at the threshold of hearing, submitted that a similar addition based on the same seized document, viz., Page-24 of Annexure A/LA/RES/01 in the case of the purchaser of the balance area of the property i.e., 244.16 sq. yards (out of 698.66 sq. yards), viz. M/s Rutuja Projects was vacated by the CIT(A), and recently, the appeal filed by the revenue in the case of the said co-purchaser has been dismissed by the revenue in ITA No. 1689/Hyd/2025, dated 10/06/2026. The Ld. AR placed on record the order of the Tribunal in the case of ACIT Vs. M/s Rutuja Projects, ITA No. 1689/Hyd/2025, dated 10/06/2026. The Ld. AR relied upon the CIT(A) order and submitted that he had rightly vacated the impugned addition made by the AO.

15. We have thoughtfully considered the contentions advanced by the Learned Authorised Representatives of both parties in the backdrop of the material available on record.

16. Admittedly, it is a matter of fact borne from the record that the AO except for relying upon the contents of the seized document, i.e., a loose sheet, viz., Page-24 of Annexure A/LA/RES/01, has failed to place on record any independent material which would corroborate his view that the assessee had paid on-money for purchasing the subject property from Dr. Amidyala Lingaiah (supra). Apart from that, we find that based on the contents of the seized documents, viz., Page-24 of Annexure A/LA/RES/01, the AO while framing the assessment in the case of the seller, viz., Dr. Amidyala Lingaiah (supra) had made an addition in his case based on his view that he had sold the subject property @ Rs.52,000/- per sq yd and not at the value disclosed by him in the registered sale deed. As observed herein above, the aforesaid addition made by the AO in the case of Dr Amidyala Lingaiah (supra) has been vacated by the CIT(A), which order had thereafter been upheld by the Tribunal vide its order passed in ITA No.702/Hyd/2022, dated 26/04/2023. Apart from that, we find that the order of the CIT(A) vacating a similar addition based on the content of the same seized document, viz., Page-24 of Annexure A/LA/RES/01, made in the case of M/s Rutuja Projects, i.e., the purchaser of the balance 244.16 sq. yards (out of 698.66 sq. yards), which was also vacated by the CIT(A), had recently been upheld by the Tribunal and the appeal filed by the revenue in ITA No. 1689/Hyd/2025, dated 10/06/2026 has been dismissed.

17. We further concur with the view taken by the CIT(A) in the present case before us that the AO, except for relying upon the unsubstantiated contents of the seized document, viz., Page-24 of Annexure A/LA/RES/01, has failed to place on record any documentary evidence which would irrefutably substantiate his view that the assessee had paid on-money for purchasing the subject property. At this stage, we are reminded of the judgment of the Hon’ble High Court of Punjab & Haryana in the case of Paramjit Singh vs. ITO [2010] 195 Taxman 273 (Punjab & Haryana), wherein it has been held that the contents of a registered sale deed cannot be dislodged on the basis of oral or hearsay evidence. The Hon’ble High Court, while concluding as herein above, had drawn support from Sections 91 and 92 of the Indian Evidence Act, 1872. For the sake of clarity, we deem it apposite to cull out the observation of the Hon’ble High Court, as under:

“The assessee has approached this Court by invoking the provisions of Section 260A of the Income Tax Act, 1961 (for brevity ‘the Act’) challenging order dated 17.12.2008 (A.6) passed by the Income Tax Appellate Tribunal, Amritsar (for brevity ‘The Tribunal’) in ITA No. 373 ASR -2007 in respect of assessment year 2003-04. The Tribunal while accepting the appeal of the Revenue has expressed the view that ostensible sale consideration of the land disclosed in the registered sale deed dated 24.9.2002 deserves to be added to the income of the assessee- appellant. The Tribunal has dis-regarded the statement made on affidavit by the vendor S/Shri Tirath Singh and Surmukh Singh, who are the real uncles of the assesse- appellant. They have stated in the affidavits that Infact no sale consideration had passed hands and they had relinquished their share in the landed property. The object of executing sale deed was only to handover landed property to the assessee-appellant as they are well settled in United Kingdom since 1960’s and 1970’s. After the case was remanded back to the CIT(A), a report was obtained by the CIT(A) in respect of the aforesaid affidavits filed by the vendor. The Assessing Officer asked Tirath Singh son of Pakhar Singh certain questions

xxx xx xx

Mr. Ravish Sood, learned counsel for the appellant has vehemently submitted that the arrangement made between the father of the assessee-appellant and both his uncles should have been given due credence as was rightly done by the CIT(A) and once his uncles have stated on oath that no consideration has passed to them then it should not be imagined that the amount has passed hands which is hidden income of the assessee- appellant and therefore liable to be added. The learned counsel has pointed out that in the account of the assessee- appellant the amount remained deposited is not more than few thousands at any time and such a huge amount of over 24 Lacs could not have been paid by him.

We have thoughtfully considered the submissions made by the learned counsel and are of the view that they do not warrant acceptance. There is well known principle that no oral evidence is admissible once the document contains all the terms and conditions. Sections 91 and 92 of the Indian Evidence Act, 1872 (for brevity ‘the 1872 Act’) incorporate the aforesaid principle. According to Section 91 of the Act when terms of a contracts, grants or other dispositions of property has been reduced to the form of a documents then no evidence is permissible to be given in proof of any such terms of such grant or disposition of the property except the document itself or the secondary evidence thereof. According to Section 92 of the 1872 Act once the document is tendered in evidence and proved as per the requirements of Section 91 then no evidence of any oral agreement or statement would be admissible as between the parties to any such instrument for the purposes of contradicting, varying, adding to or subtracting from its terms. According to illustration ‘b’ to Section 92 if there is absolute agreement in writing between the parties where one has to pay the other a principal sum by specified date then the oral agreement that the money was not to be paid till the specified date cannot be proved. Therefore, it follows that no oral agreement contradicting/ varying the terms of a document could be offered. Once the aforesaid principal is clear then ostensible sale consideration disclosed in the sale deed dated 24.9.2002 (A.7) has to be accepted and it cannot be contradicted by adducing any oral evidence. Therefore, the order of the Tribunal does not suffer from any legal infirmity in reaching to the conclusion that the amount shown in the registered sale deed was received by the vendors and deserves to be added to the gross income of the assessee- appellant.

For the reasons afore mentioned this appeal fails and the same is dismissed.”

18. We thus, are of firm conviction that now when it has been the claim of the assessee that he had not paid any on-money, i.e., any amount in excess of that disclosed in the registered sale deed for which it had purchased the subject property from Dr. Amidyala Lingaiah (supra), the AO was by no means justified to reject the said claim without placing on record any irrefutable secondary evidence which would disprove to the hilt the veracity of the same. Also, we find that our view that adverse inferences cannot be drawn on a standalone basis by relying upon the contents of a dumb document seized in the course of the search proceedings is supported by the judgment of the Hon’ble Jurisdictional High Court in the case of Principal Commissioner of Income Tax (PCIT) vs. Tarun Kumar Goyal in ITA No. 243 of 2022, dated 24th August, 2022. In the said case, the Hon’ble High Court, finding no element of perversity in the view taken by the Tribunal, which has held that the impugned addition of on-money payment made in the assessees’ hands on the basis of a mere dumb document, which is not corroborated by any other evidence, was not sustainable, dismissed the revenue’s appeal.

19. Be that as it may, we also cannot remain oblivion of the fact that now when the seized document, viz., Page-24 of Annexure A/LA/RES/01, has been held by the Tribunal while disposing of the appeal in the case of seller, viz., ACIT vs. Sri Lingaiah Amidyala, ITA No.702/Hyd/2022, dated 26/04/2023 as a “dumb document”, the said impugned seized document cannot be acted upon for arriving at a view to the contrary qua the consideration paid by the assessee, i.e., the purchaser for the same sale transaction, specifically when no independent corroborative material to the contrary has been placed on record by the Revenue.

20. We thus, in terms of our aforesaid deliberations, finding no infirmity in the view taken by the CIT(A), who had rightly based on his observations vacated the addition made in the hands of the assessee, uphold his order.

21. Resultantly, the appeal filed by the Revenue, being devoid and bereft of any substance, is dismissed.

C.O. No. 02/Hyd/2026

(By assessee)

22. We shall now take up the cross-objection filed by the assessee. While dealing with the Revenue’s appeal in ITA No.1688/Hyd/2025, AY 2019-20, in the foregoing paragraphs of this order, we have upheld the view taken by the CIT(A) and dismissed the appeal of the Revenue. Accordingly, in terms of our aforesaid observations, the present cross-objection filed by the assessee, supporting the view taken by the CIT(A), is allowed.

23. In the result, the appeal filed by the Revenue is dismissed, and the Cross-Objection filed by the assessee is allowed in terms of our aforesaid observations.

Order pronounced in the open court on 17th June, 2026.

Author Bio