Article compiles Income Tax Slab Rate For Financial Year 2020-21 ( A.Y.- 2021-22) for Individual and HUF as per Old Regime and as per new Regime. It further compiles Tax Rates for Co-Operative Society, Co-Operative Society, Domestic Company, Foreign Company, AOP/BOI or Every Artificial Judicial Person for Financial Year 2020-21.

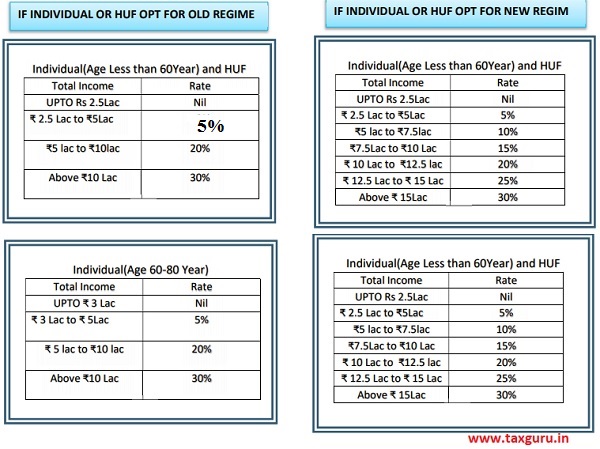

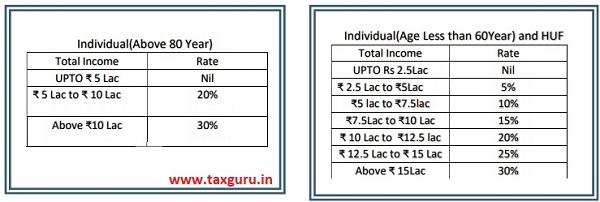

Income Tax Slab Rate For Financial Year 2020-21( A.Y.- 2021-22)

–

NOTE:

1- The Amount of Income Tax Shall Be Increased By Surcharge as Follow:-

A. Total Income ₹ 50 Lac to ₹ 1Cr- At the Rate 10%

B. Total Income ₹ 1Cr to ₹ 2 Cr- At the Rate 15%

C. Total Income ₹ 2 Cr to ₹ 5 Cr- At the Rate 25%

D. Total Income Above ₹ 5Cr At the Rate 37%

2- Marginal Relief will be allowed in all case where surcharge is to be levied.

3- Health and Educational cess on Income Tax Will be At 4%.

IN THE CASE OF CO-OPERATIVE SOCIETY

Note:-

1. The Amount of Income Tax Shall Be Increased By Surcharge at the rate 12% in case Total Income Exceed ₹ 1 Cr.

2. Marginal Relief will be allowed in all case where surcharge is to be levied.

3. Health and Educational cess on Income Tax Will be At 4%.

FIRM INCLUDING LIMITED LIABILITY PARTNERSHIP

Note:-

1. Income tax Shall be payable at the rate of 30%

2. The Amount of Income Tax Shall Be Increased By Surcharge at the rate 12% in case Total Income Exceed ₹ 1 Cr.

3. Marginal Relief will be allowed in all case where surcharge is to be levied.

4. Health and Educational cess on Income Tax Will be At 4%.

DOMESTIC COMPANY

FOREIGN COMPANY

FOREIGN COMPANY

Note:-

1. Income tax Shall be payable at the rate of 40%

2. The Amount of Income Tax Shall Be Increased By Surcharge at the rate 2% in case Total Income Exceed ₹ 1 Cr to ₹ 10 Cr.

3. The Amount of Income Tax Shall Be Increased By Surcharge at the rate 5% in case Total Income Exceed ₹ 10 Cr.

4. Marginal Relief will be allowed in all case where surcharge is to be levied.

5. Health and Educational cess on Income Tax Will be At 4%.

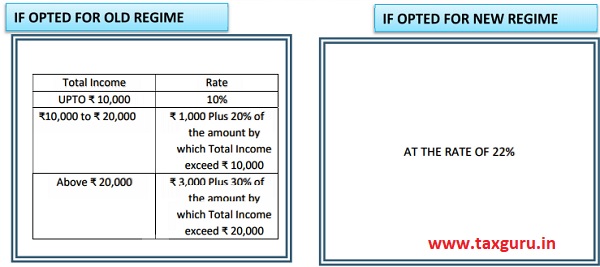

AOP/BOI OR EVERY ARTIFICIAL JUDICIAL PERSON

| Total Income | Rate |

| UPTO Rs 2.5Lac | Nil |

| ₹ 2.5 Lac to ₹5Lac | 10% |

| ₹5 lac to ₹10lac | 20% |

| Above ₹10 Lac | 30% |

Note:

1. The Amount of Income Tax Shall Be Increased By Surcharge as Follow:

> Total Income ₹ 50 Lac to ₹ 1Cr- At the Rate 10%

> Total Income ₹ 1Cr to ₹ 2 Cr- At the Rate 15%

> Total Income ₹ 2 Cr to ₹ 5 Cr- At the Rate 25%

> Total Income Above ₹ 5Cr At the Rate 37%

2. Marginal Relief will be allowed in all case where surcharge is to be levied.

3. Health and Educational cess on Income Tax Will be At 4%.

*****

Disclaimer:- The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. We do not accept any responsibility for loss incurred by any person for acting or refraining to act as a result of any matter in this article.

About The Author- : He is a member of Institute of Chartered Accountants of India since 2018 and having experience in the field of Taxation (both Direct and Indirect Tax), Company Law, Auditing and other legal framework. He is doing practice from the first day of his membership and working towards the never ending scope of improvement and quality in the field of various taxation Laws.

Author Bio

Under old tax slab ….income tax rate on individual below 60 years of age is 5% in the income bracket between 2.5 lac to 5 lac

You r showing it as 10%

Yes You are Correct. It is my clerical mistake. I Apologize for this clerical mistake.