Article explains Conditions for Tax Neutral Demerger, Reasons for Demerger, Tax Implications of Demerger, Tax implications of Demerger in the hands of the transferor entity, Tax implications of Demerger in the hands of shareholders of the transferor entity, ACCOUNTING IMPLICATIONS of Demerger, Accounting Aspects in Different Demerger Situations, Applicable Sections for Slump Sale, Taxability on gains arising from Slump Sale, Tax Effect on Slump Sale, Computation of Net worth in Slump Sale, Stamp duty on Slump Sale, DEMERGER V/S SLUMP SALE – Comparison and Important Regulations for Demerger & Slump Sale.

Page Contents

- A. DEMERGER

- 1. Conditions for Tax Neutral Demerger

- 2. Reasons for Demerger

- 3. Tax Implications of Demerger

- 4. ACCOUNTING IMPLICATIONS of Demerger

- 5. Accounting Aspects in Different Demerger Situations

- B. SLUMP SALE

- 1. Applicable Sections for Slump Sale

- 2. Taxability on gains arising from Slump Sale

- 3. Tax Effect on Slump Sale

- 4. Computation of Net worth in Slump Sale:

- 5. Stamp duty on Slump Sale

- C. DEMERGER V/S SLUMP SALE – Comparison

- D. Important Regulations for Demerger & Slump Sale

A. DEMERGER

Division of a company with two or more identifiable business units into two or more separate companies.

In accordance with following Sections:

♣ Section 2(19AA) of Income Tax Act, 1961

♣ Section 230-232 of Companies Act, 2013

1. Conditions for Tax Neutral Demerger

- Transfer of all properties & liabilities relatable to the undertaking being transferred by the demerged company to the resulting company at book value;

- Discharge of consideration by the resulting company by way of issue of shares on proportionate basis (except where resulting company itself is a shareholder of the demerged company);

- Issue of shares to the shareholders holding not less than 3/4th shares (in value) in the demerged company (other than the shares already held by the resulting company or its nominees or its subsidiary);

- Transfer of undertaking to be on a going concern basis

2. Reasons for Demerger

- To unlock value

- To exonerate family disputes

- For better focus

- Joint venture or alliance

- To get going public

- To acquire control

3. Tax Implications of Demerger

i. Tax implications of Demerger in the hands of the transferor entity

The income tax laws specifically provide that in case of a tax neutral demerger, no capital gains tax implication will arise on the transferor entity on transfer of capital assets to the transferee entity, so long as the resulting company is an Indian company.

In case of demerger of a foreign entity into another foreign entity, wherein capital assets being shares of an Indian company are transferred, no capital gains tax implication will arise in India if the following conditions are satisfied:

- At least 75% of the shareholders of the transferor foreign entity remain shareholders of the foreign transferee entity; and

- The transfer is not chargeable to capital gains tax in the country in which the transferor foreign company is incorporated.

In the case of a demerger, the issue of shares by the transferee entity to the shareholders of the transferor entity (in lieu of shareholding in transferor entity) is not regarded as ‘transfer’ and hence it is not subject to capital gains tax.

4. ACCOUNTING IMPLICATIONS of Demerger

- No specific Accounting standard prescribed for demerger.

- Generally, resulting company records all assets and liabilities at book values to comply with tax neutrality conditions:

- Excess of net assets received by the resulting company over the face value of shares issued is credited to reserve , incase of deficit debited to Goodwill account.

- In books of demerged company, the value of net assets transferred is adjusted against reserve

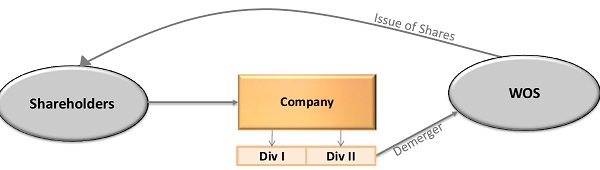

5. Accounting Aspects in Different Demerger Situations

Situation

- It is contemplated for demerger of undertaking in WOS.

- WOS to issue shares to shareholders of demerged company.

Accounting Aspect

Wholly Owned Subsidiary Difference between value of shares issued and net asset taken over to be credited to Capital Reserve or be adjusted against reserve and balance debited to goodwill.

Demerged Company Deficit to be adjusted against General Reserve or any other reserve including P&L

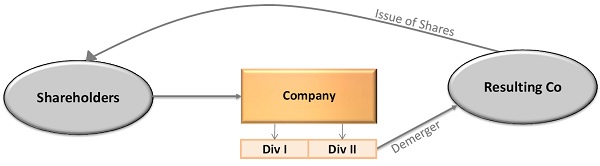

Situation

- Scheme provides for demerger of undertaking of company into Resulting Co.

- Revaluation of one of the residual undertaking

Accounting Aspects

Resulting Company

Excess of net assets over share issued to be transferred to General Reserve and in case of shortfall, be debited to goodwill/ securities premium account.

Demerged Company

Value of net assets transferred to be adjusted against securities premium, to the extent available and then against General Reserve.

Gain on revaluation of the one of the residual undertaking transferred to Revaluation Reserve.

B. SLUMP SALE

1. Applicable Sections for Slump Sale

Section 50B of Income Tax Act, 1961

Section 180 of Companies Act, 2013

Slump Sale means the transfer of one or more undertakings as a result of the sale for a lump sum consideration without values being assigned to the individual assets and liabilities in such sales.

2. Taxability on gains arising from Slump Sale

- Capital gains arising on transfer of an undertaking are deemed to be long-term capital gains.

- However, if the undertaking is ‘owned and held’ for not more than 36 months immediately before the date of transfer, gains shall be treated as short-term capital gains.

- Taxability arises in the year of transfer of the undertaking.

- Such gains arising on slump sale are calculated as the difference between sale consideration and the net worth of the undertaking.

- Net worth is deemed to be the cost of acquisition and cost of improvement for section 48 and section 49 of the Act.

- As per section 50B, no indexation benefit is available on cost of acquisition, i.e., net worth.

- In case of slump sale of more than one undertaking, the computation should be done separately for each undertaking.

3. Tax Effect on Slump Sale

| Particulars | Amount |

| Full Value of Consideration | xxx |

| Less: Expenses in Relation to Transfer | (Xxx) |

| Net Consideration | Xxx |

| Less: Cost of Acquisition/Net worth | (xxx) |

| Capital Gain/(Loss) | Xxx |

4. Computation of Net worth in Slump Sale:

In computing the net worth of the entity, the following points need to be considered:

- The value of net worth should not take into account any change in the value of the asset or liability resulting from revaluation of such asset or liability.

- In case of depreciable assets under the Income Tax Act, the Written Down Value of such assets as per the Act shall be considered.

- In case of assets on which 100% deduction has been allowed u/s 35AD (specified business), the value of such assets will not be considered.

- In case of any other asset, value as appearing in the books of accounts shall be considered.

- After considering the above points, if the resulting net worth is negative, then the cost of acquisition shall be taken as nil for the purpose of computation of capital gains.

5. Stamp duty on Slump Sale

Stamp duty shall be levied on investment and immovable property.

C. DEMERGER V/S SLUMP SALE – Comparison

| Particulars | Demerger | Slump Sale |

| Document | Scheme of Merger | Business Transfer Agreement |

| NCLT Approval | Yes | No |

| Mode of Consideration | Cash or Shares | Shares |

| Receiver of Consideration | Shareholders of Demerged Company | Demerged Company |

| Order to be filed with RoC | Required | Not Required |

| Timelines | 4 Months | 3 Months |

| Stamp Duty | Applicable | Applicable |

| Capital Gains | No tax if it is in compliance with section 2(19AA) of the Income Tax Act, 1961. | Attracts long term or short term capital gains tax |

| Accounting Treatment | No prescribed. Purchase method to be recorded at book values to avoid violation of Section 2(19AA) of the Income Tax Act, 1961. | No specific Accounting Standard prescribed. |

D. Important Regulations for Demerger & Slump Sale

Disclaimer : All data and information is provided for informational purposes only. No reader should act on the basis of any statement contained herein without seeking professional advice. The author expressly disclaim all and any liability to any person who has read this, or otherwise, in respect of anything, and of consequences of anything done, or omitted to be done by any such person in reliance upon the contents of this report.

Author Bio

Consideration in tax neutral demerger shall only be discharged by shares and in a slump sale it can be done by either cash or shares.

Kindly please check the last two line in comparision of demerger vs slump sale. In my opinion these has been interchanged by mistake

Thanks for the detailed article .

Pl re-check the impact of capital gain in ” Demerger V/s Slumb sale “