In this Article, am trying to collate all the provisions related to ‘Transportation of Good’ under CGST Act, 2017.

Notification No. 12/2017-Central Tax Rate, dated 28.06.2017, has exempted various services from CGST by providing entries and accordingly, Entry No. 6 provides exemption to:

6. Services provided by Central Government, State Government, Union Territory or Local Authority excluding the following services:

(a) Services by the Department of Posts by way of speed post, express parcel post, life insurance, and agency services provided to a person other than the Central Government, State Government, Union Territory;

(b) Services in relation to an aircraft or a vessel, inside or outside the precincts of a port or an airport;

(c) Transport of goods or passengers; or

(d) Any service, other than services covered under entries (a) to (c) above, provided to business entities.”

So, here Transportation of goods is specifically excluded from the purview of exemption, hence this is taxable, however, we have some more entries under the same Notification, which provides for the instances where Transportation of goods is exempt.

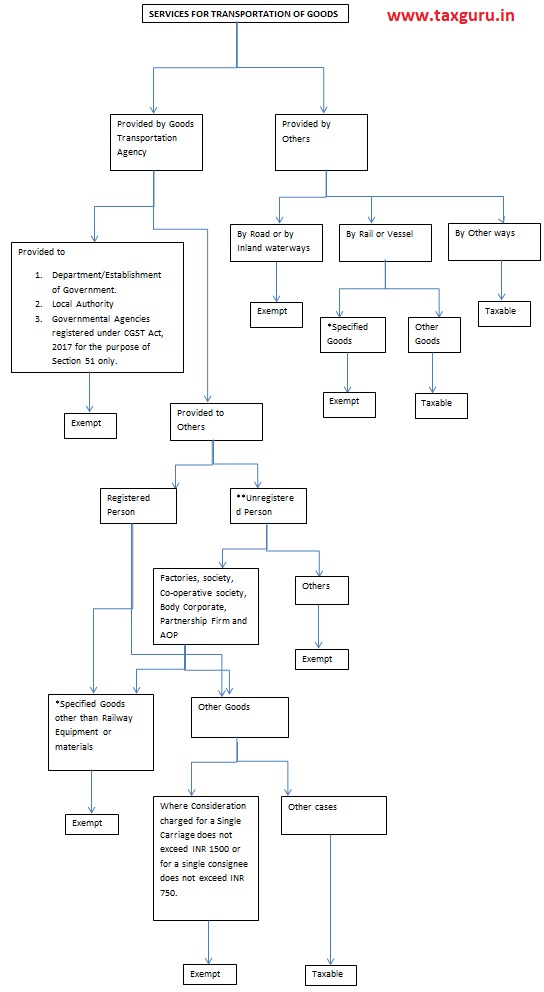

Before going into the detailed entries, we should divide the Service Providers into following two types:

Other than Goods Transportation Agencies

1. If service provider is a person other than GTA, then all the services of transportation of goods provided by that person by Road or by Inland waterways are exempt. (Entry No. 18)

2. Further, if that person provides service of transportation of goods by Rail or a vessel from one place in India to another of *specified goods is also exempt. (Entry No. 20)

Goods Transportation Agencies

1. For Goods Transportation Agencies, service of transportation in a goods carriage is exempt if is it provided for the *specified goods other than Railway equipment or materials

2. Also, where consideration charged for the transportation of goods (other than specified goods but includes Railway equipment or materials) on a consignment transported in a single carriage does not exceed INR 1500, or where consideration charged for transportation of all such goods for a single consignee does not exceed INR 750. (Entry No. 20)

3. Services provided by GTA for the transportation of any goods which are not otherwise exempt to an **Unregistered Person is exempt excluding the following categories of **Unregistered Persons under CGST Act, 2017: (Entry No. 21A)

- Any Factory registered under/ governed by the Factories Act, 1948; or

- Any Society registered under the Societies Registration Act, 1860 or under any law for the time being in force.

- Any Co-Operative society established under any law for the time being in force.

- Any Body Corporate established under any law for the time being in force.

- Any Partnership firm whether registered or not under any law including association of persons.

- Any casual taxable person registered under CGST or IGST or SGST or UTGST Act. Whereas, including the unregistered casual taxable person.

4. Next, if any GTA provides services for transportation of any goods in a good carriage to the following persons is exempt (Entry No. 21B)

- A Department or Establishment of the Central Government or State Government or Union Territory; or

- Local Authority; or

- Governmental Agencies, which has taken registration under the CGST Act, 2017 only for the purpose of deducting tax under Section 51 and not for making taxable supplies.

Example: If ABC, a Goods Transportation Agency provides services for transportation of goods to

- Private Company whether or not registered under CGST Act, 2017, then such service is taxable to CGST and the tax on such service is paid on RCM basis.

- Public Company: This is Establishment of Central Government, State Government, Union Territory, and accordingly is exempt via Entry 21B.

- If transportation of goods provided by GTA is of Specified goods then this is exempt under Entry No. 21.

Notes:

* Specified Goods are

- Relief Materials,

- Defense or military equipment,

- Newspaper or magazines,

- Railway equipment or materials,

- Agricultural produce,

- Milk, Salt and Food grains including flours, pulses and rice

- Organic Manure.

** Unregistered Persons means the person not registered under Central Goods and Service Tax Act, 2017.