After the implementation of GST, lots of issues & difficulties are being faced by the Registered Persons and Consultants to filing the Return. All of us struggled in the past file the Return timely to avoid the Late fees but endless issue on portal to submit the return. Lots of return were files with incorrect data. Department have issued no query of return file by Taxpayer. Every Taxpayer relaxed that whatever was filled has been accepted by department without any query. But now CBIC issued Instruction No 02/2022 dated 22th March 2022 on Standard Operating Procedure (SOP) for Scrutiny of returns for FY 2017-18 and 2018-19. But now gets ready to Receiving Scrutiny Notices from department.

Relevant Legal Provision

Section 61 of the Central Goods and Services Tax Act, 2017 read with rule 99 of Central Goods and Services Tax Rules, 2017 provides for scrutiny of returns:

Section 61. Scrutiny of returns:

“(1) The proper officer may scrutinize the return and related particulars furnished by the registered person to verify the correctness of the return and inform him of the discrepancies noticed, if any, in such manner as may be prescribed and seek his explanation thereto.

(2) In case the explanation is found acceptable, the registered person shall be informed accordingly and no further action shall be taken in this regard.

(3) In case no satisfactory explanation is furnished within a period of thirty days of being informed by the proper officer or such further period as may be permitted by him or where the registered person, after accepting the discrepancies, fails to take the corrective measure in his return for the month in which the discrepancy is accepted, the proper officer may initiate appropriate action including those under section 65 or section 66 or section 67, or proceed to determine the tax and other dues under section 73 or section 74.”

Rule 99. Scrutiny of returns:

“(1) Where any return furnished by a registered person is selected for scrutiny, the proper officer shall scrutinize the same in accordance with the provisions of section 61 with reference to the information available with him, and in case of any discrepancy, he shall issue a notice to the said person in FORM GST ASMT-10, informing him of such discrepancy and seeking his explanation thereto within such time, not exceeding thirty days from the date of service of the notice or such further period as may be permitted by him and also, where possible, quantifying the amount of tax, interest and any other amount payable in relation to such discrepancy.

(2) The registered person may accept the discrepancy mentioned in the notice issued under sub rule (1), and pay the tax, interest and any other amount arising from such discrepancy and inform the same or furnish an explanation for the discrepancy in FORM GST ASMT-11 to the proper officer.

(3) Where the explanation furnished by the registered person or the information submitted under

sub-rule (2) is found to be acceptable; the proper officer shall inform him accordingly in FORM GST ASMT-”

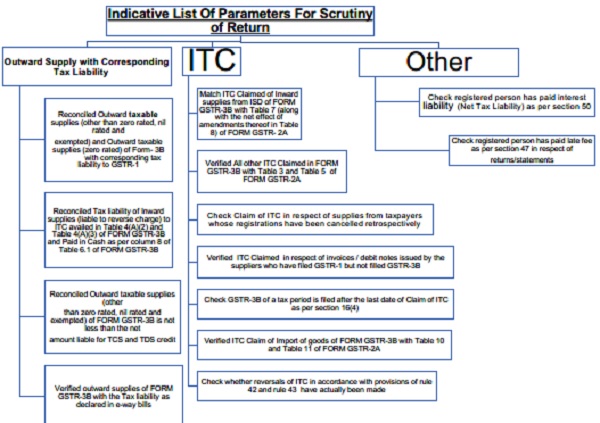

Indicative List Of Parameters For Scrutiny of Return

Process & Timelines for Scrutiny of return

Scrutiny of returns is to be conducted in a time bound manner, so that necessary action to safeguard revenue may be taken up expeditiously.

- The discrepancy issued in Form ASMT-10 show Tax, Interest and any other amount payable in relation to such discrepancy.

- If Registered Person accept the discrepancy issued in Form ASMT-10 then he will pay the Tax, Interest and any other amount through Form DRC-03 and inform the same in form ASMT-11 within the prescribed time limit.