The determination of place of supply in G.S.T. is important because only after its determination it will be decided that a transaction / supply is liable to IGST or SGST/UTGST and CGST.

The place of supply of service is determined u/s 12, 13 and 14 of the IGST act.

Section 12 deals with the situation where the location of recipients and location of supplier is an India.

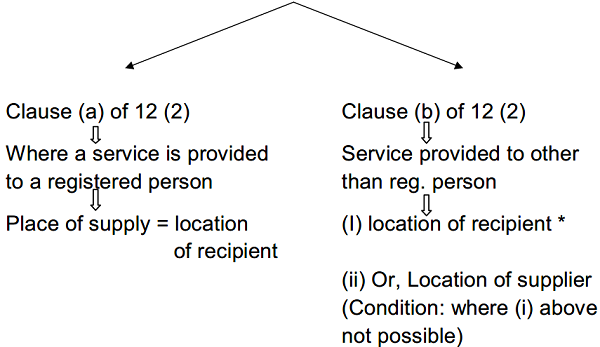

1. The subsection (2) of section 12 is a residual section which says that where the place of supply of service cannot be determined under sub-section 3 to sub-section 14, the place of supply in such situation shall be determine according to this sub-section and its says that

(*Condition: Address of recipient exists or available on records)

2. The sub-section (3) of section 12 of the IGST act has laid down 4 clauses which are in relation to immovable property

(a) The clause (a) of sub-section (3) of section 12 says that the place of supply of services. Which are directly in relation to immovable property shall be the location of immovable property.

Services directly in relation to immovable property includes service provided by architect, interior decorator, surveyors, engineers, other related experts or real estate agent, and service provided by way of grant to use immovable property, for carrying out co-ordination of construction work, this list is inclusive and not executive the services which are directly related other than that covered w/s 12(3)(a) shall also have the place of supply at the location of immovable property.

(b) The clause (b) of sub-section (3) of section 12 says that the place of supply of service by hotel, guest house etc. of logging, accommodation shall be the location of immovable property (i.e. hotel, guest house etc) as per clause (c) of 12 (3).

(c) The place of supply of service by way of accommodation in any immovable property for organizing any marriage or any official, social, cultural, religious or business function shall be the location of immovable property (i.e where such marriage or any official, social, cultural, religious or business function conducted).

(d) The service ancillary to the service rejected in clause (a), (b), (c) above shall be the location of immovable property.

Note: – The proviso to section 12(3) says that where the location of immovable is outside the India, the place of supply shall be the location of recipient and not the location of immovable property.

(3) 12(4)The place of supply of services of restaurant, catering, plastic surgery, health services, beauty treatment shall be the location where the service is actually performed (performance based services i.e where the presence of the person receiving the service is mandatory)

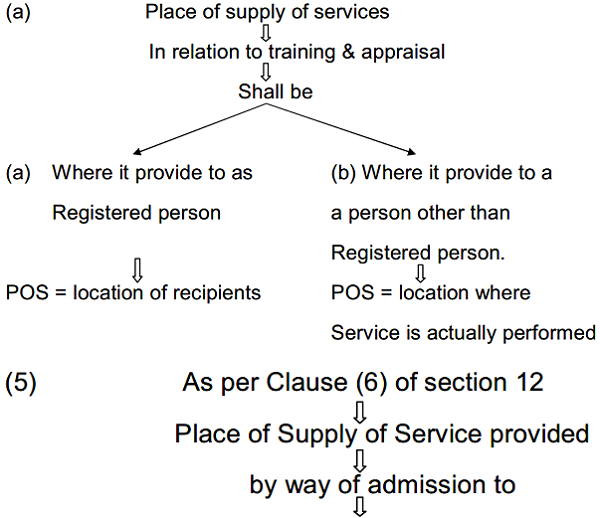

(4) As per clause (5) of section 12

| Nature of service | Place of supply |

| An event or service ancillary thereto | Place where the event is held |

| Any park or service ancillary thereto | Place where park is situated |

| Any other place or service ancillary thereto | Location of such other place. |

(6) As per sub-section (7) of section 12 the place of supply of service provided by way of organizing an event (of) services ancillary thereto (of) sponsorship of an event shall be the

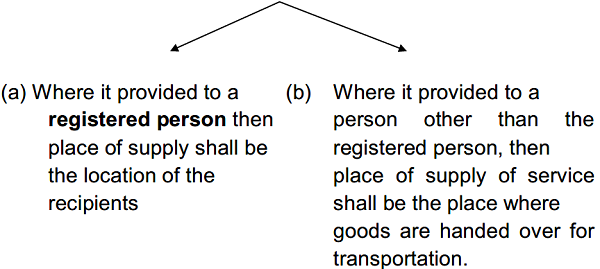

(7) As per sub-section (8) of section 12 the place of supply of Service provided by way of transportation of goods, including mail or courier shall be

(8) As per sub-section (9) of section 12 the place of supply of services provided by way of transportation of passenger shall be the

![]()

| Nature of service | Place of supply |

| Where it provides to a registered person | location of recipients |

| Where if provides to a person other than the registered person | place where passenger starts his journey |

As per the provision to section 12 (a) where the location where the passenger embarks its journey is not known, then place of supply shall be determined in accordance with 12 (2) [i.e general rule ]

(9) As per sub-section 10 of section 12, the place of supply service on board a conveyance, shall be the location of the first point of departure of the conveyance.

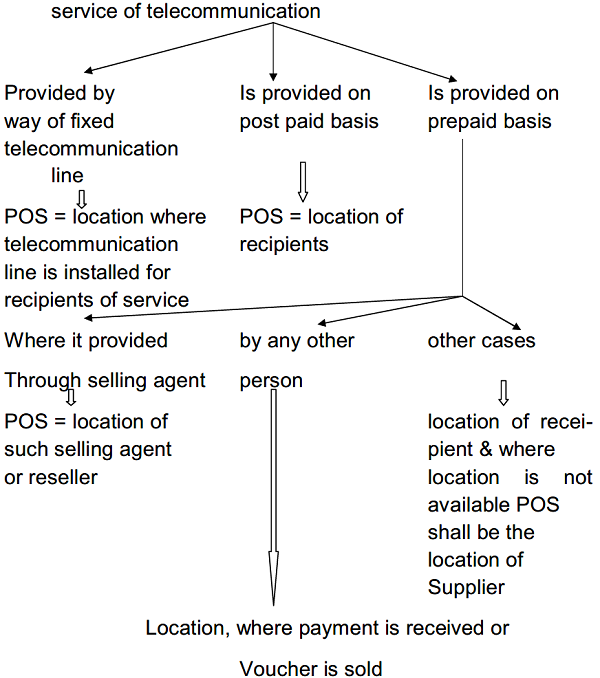

(10) As per sub-section 11 of section 12, the place of supply of service of telecommunication

(11) As per sub-section 12 of section 12 ,Place of Supply of service of banking or other financial service shall be the

(12) As per sub-section 13 of section 12, Place of supply of Insurance service shall be the

(13) As per sub-section 14 of section 12 the place of supply of advertisement services to the Central Government, a State Government, a statutory body or a local authority,

![]()

Meant for the States or Union territories identified in the contract or agreement.

![]()

Shall be taken as being in each of such States or Union territories.

Author Bio

DEAR CA SAHAB,

PLEASE UPDATE YOUR KNOWLEDGE, SECTION 12(8) HAS BEEN UPDATED, PLEASE UPDATE YOURSELF.

SUPPORT TO MINING SERVICES

A IS A MINING COMPANY. PLACE OF REGISTRATION AT KARNATAKA. HE IS THE FINAL SERVICE RECEIVER

B IS THE MAIN CONTRACTOR. PLACE OF REGISTRATION AT CHENNAI. HE HAS GIVEN SUB CONTRACT TO C

C IS THE SUB CONTRACTOR. PLACE OF REGISTRATION AT KARNATAKA. HS AS GIVEN SUB CONTRACTOR TO D

D IS THE SUB CONTRACTOR. PLACE OF REGISTRATION AT KARNATAKA. HE HAS GIVEN SUB CONTRACT TO OTHERS (XYZ) FOR EXECUTING THE WORK.

XYZ IS THE ACTUAL WORK EXECUTING PERSONS. REGISTRATION IN KARNATAKA

WE ARE CHARGING THE TAXES AS FOLLOWS:

XYZ TO D SGST AND CGST

D TO C SGST AND CGST

C TO B IE KARNATKA TO CHENNAI IGST

B TO A IE CHENNAI TO KARNATAKA IGST

NOTE: A IS THE FINAL SERVICE RECEIVER AT KANATAKA

B IS THE MAIN CONTRACTOR AT CHENNAI , C , D IS THE SUB CONTRACTOR AT KARNATAKA

XYZ ARE THE FINAL SERVICE PROVIDER WHO ACTUALLY EXECUTED THE WORK AT KARNATAKA

SIR PLEASE CLARIFY THE SAME AND IF ANY CHARGES PL INFORM.

Your Article is Good. I wish to add the situation which needs inclusion in your article for clarity.

NTPC has awarded a contract for delvopment of Mines to a party MDO ( Mine development Operator agreement) to A-1 situated in Jharkhand. A-1 has issued various PO consisting services as well as Goods.A-1 issues Design, Machinery parts, Erection commisisoning PO respectively to B-1 who is an EPC contractor.

Goods consist of Machinery parts in kockdown condition. Services Consist of Design, Erection Commissioning of that Machine.

The Machine being manufacturered based on the Design by various vendors under B-1.

Design being carried out by a single sub vendor C-1 from B-1.

C-1 & B-1 are with the same state. C-1 delivers to B-1 and has no interaction with A-1 or acess to site.

Since C-1 and B-1 have registration & having business operation in the same state and no further registration.

Whether the transaction between C-1 & B-1 coming under the purview of CGST +SGST or IGST.

Kindly clarify.