♦ A taxpayer is entitled to refund of tax wrongly paid or paid in excess (other than zero-rated supplies), in the same mode by which the tax liability was discharged.

♦ The cash part has to be sanctioned and credited to the bank account of the taxpayer by Form RFD-05 &

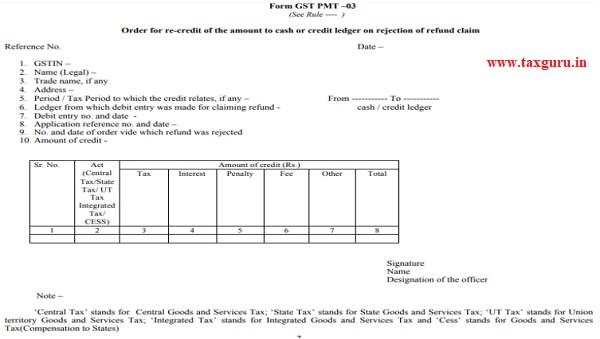

♦ ITC part should be re-credited to the electronic credit ledger of the taxpayer through Form PMT-03

♦ A new enhanced PMT-03 functionality has been developed and deployed in the Department system to re-credit the ITC in Electronic Credit Ledger in case of a Refund.

This new functionality is applicable for the below-mentioned Refunds;

> a) Refund of excess payment of tax;

> b) Refund of tax paid on an intra-State supply which is subsequently held to be inter-State supply and vice versa;

> c) Refund on account of assessment/provisional assessment/appeal/any other order; and

> d) Refund on account of “any other” ground or reason.

Author Bio