Dear Friends, as you are aware that as per 101st Constitution Amendment Act, 2016 below mentioned goods have been outside the purview of GST;

i) Petroleum Crude;

ii) High Speed Diesel Oil;

iii) Motor Spirit;

iv) Natural gas;

v) Aviation Turbine Fuel.

Some other products such as LPG, fuel oil, kerosene, naphtha etc are included in GST regime.

There are some direct and indirect impacts of the GST on oil and gas sector.

The Central Goods and Services Tax Act, 2017, Section 9(2) keeps above goods out of purview of GST regime and provides that, tax on the supply of the said goods shall be levied with effect from such date as may be notified by the Government with consultation of GST Council.

Since GST is applicable on few Oil/Gas products and many are excluded, the industry has to follow both previous VAT as well as GST regime.

The Form C is still in use for purchase of non-GST products such as natural gas, HSD, crude, ATF, and MS, for manufacture and resale of goods, generation or distribution of power and telecommunication mining or networking. However, C form cannot be issued for other manufacturer goods.

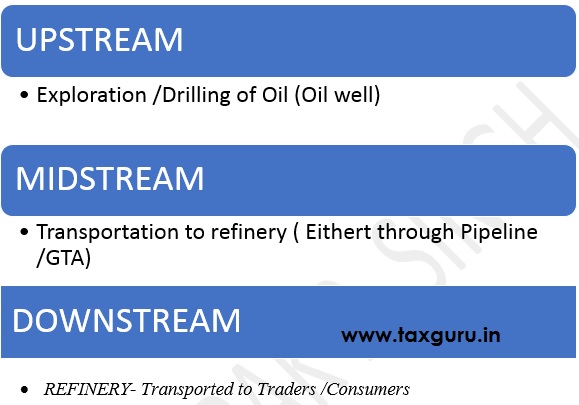

LET’S CONSIDER FIRST TYPICAL STRUCTURE OF OIL/GAS COMPANIES;

UPSTREAM SECTOR

This sector includes searching for potential underground or underwater Crude Oil Fields Drilling Exploratory and subsequently drilling and operating the wells that recover and bring crude oil to the surface.

The procurement of upstream oil companies is categorised under below mentioned heads;

i) Exploration;

ii) Drilling;

iii) Projects; and

iv) Operations.

The Oil Companies prior to drilling engaged such companies, which has expertise in searching Oil reserves underground or underwater. After that the Upstream companies have to purchase various Capital Goods for establishing a platform for exploration and drilling of searched Crude Oil.

In above situation the out put i.e. Oil and Natural Gas are kept outside purview of GST Regime, but the procurement requirements and Capital Goods are kept under GST.

“WORK CONTRACT”– as a concept will typically become relevant at the last two stages i.e. on Projects and Operations.

The Oil and Gas companies engaged contractors for setting up of an onshore/offshore platform at project stage. Such contracts if entered as a single contract for the entire work, are likely to qualify as “Work Contract”, under GST.

Note:

i) The Government in 22nd GST Council Meeting dated 06-10-2017 vide Notification No. 39/2017-Integrated Tax (Rate) dated 13-10-2017, has provided that GST shall be levied at a reduced rate of @12% on Work Contracts Services in respect of Offshore Work Contract relating to all Oil & Gas exploration and production (E&P) in the Offshore Area beyond 12 nautical miles;

ii) The Government has notified several packages under the contract for construction of a platform may qualify as “Plant and Machinery”, and thus not subject to credit restrictions as applicable on Immovable Properties as per Section 17(5) (c) and (d) of the Goods and Services Tax Act, 2017;

iii) At initial stage several kinds of Annual Maintenance Contracts are typically procured by Oil and Gas Companies; an Annual Maintenance Contracts can qualify as pure services contracts only, when they involve no supply of goods. if maintenance/repair obligations pertain to immovable property, including a plat/machinery which is embedded to earth in a manner that makes it qualify as an “Immovable Property,” such Annual Maintenance Contracts are qualified as “Work Contracts”.

iv) If those (AMC)contracts are not qualified as “Work Contracts”, then they are considered as a Work Contract, then they will be considered as “Composite Supply” of repair/ maintenance services.

The Government has allowed these Oil and Gas companies to make their contracts with contractors such that they will come under category of “Work Contracts”. They will take credit of inputs applied in above Goods and Services through procedure prescribed by the Government.

MIDSTREAM SECTOR

This sector typically involves the transportation (by pipelines, rail, barge, oil tanker or truck), storage, wholesale marking of Crude or Refined Petroleum products. The Pipelines can be used to transport Oil and Gas from exploration site to various depot from where they will be transported through Pipelines to various downstream distributors.

Note: the midstream company are expending a lot in establishment of pipelines and on their maintenance. Now if they are not involved in sale /purchase of Crude or Gas, they their services are considered as “Pure Services”, and they are eligible for Input Tax Credit.

In earlier tax regime, before GST the midstream companies procure various inputs and capital goods for undertaking construction of Pipelines System. Earlier there was much litigation on claiming of input of excise duty paid on purchase of inputs in constitution of Pipelines with taxing authorities and in GST regime also there are much litigation on subject matter.

SECTION 17(5) (C) & (D) OF CGST, ACT 2017; “Pipelines laid outside the factory premises, have been excluded from the definition of “Plant and Machinery”, consequently, it appears that GST on supply of Goods/Services or Work Contract Services leading to creation of “Pipelines laid outside the factory premises”, would not be available as credit.

The New Delhi -CESTAT in case of Jaypee Bela Plant Vs. CCE, Bhopal [2007] taxmann.com 1500

It was held that pipes and tubes constituting a pipeline which is used for carrying water from reservoir situated 5/6 kilometres away from the factory premises for use in manufacture of finished products, were eligible for credit.

Thus, we can apply “Mischief Rule of statutory interpretation “to define “Pipelines laid outside the factory premises”, for allowing GST input.

DOWNSTREAM SECTOR; commonly refers to the refining of petroleum crude oil and the processing/regasification of Raw Natural Gas/Liquified Natural Gas as well as marketing and distribution of product derived from crude and natural gases.

These companies use refineries, which purify the Petroleum Crude and manufacture refined petrol, HSD, Aviation Fuel, etc., the main inputs of these companies are Raw Crude Oil and Raw Gases, which are kept outside of GST regime and outputs consist of taxable and non-taxable products.

The concept of “Work Contract” become important for these companies both for construction/expansion of refineries/LNG Terminals as well as in case of some Annual Maintenance Contracts.

Note: –

i) for construction /expansion of refineries/ LNG terminals, downstream companies engage EPC contractors-such contracts, of entered into single contract for the entire works, are likely to qualify as “Work Contract”, under GST regime. Since these would amount to construction of immovable property;

ii) It is pertinent to understand that several packages under contract for construction/expansion of refineries/LNG terminals may qualify as “Plant and Machinery”, thus not subject to credit restrictions as applicable to “Immovable Property”, under Sections 17(5) (c) & (d);

iii) The downstream companies need to have two separate contracts one for packages that will constitute “Plant and Machinery”, and one for rest;

iv) Annual Maintenance Contracts can qualify as pure service contract, when there is no supply of goods;

v) If maintenance /repair obligations pertain to immovable property which embedded to earth in a manner that makes it qualify as an “Immovable Property”, such Annual Maintenance Contracts likely to qualify as “Work Contracts” and if not, such will qualify as “Composite supply of repair/ maintenance services”.

SOME IMPORTANT POINTS;

- The credit is available only for tax paid on input Capital Goods (CG) for manufacturing of taxable or exempt petroleum products;

- No credit of GST paid on machinery and services, plant and other input expenses for manufacturing of excluded products;

- The tax rate has increased from 15% to 18% on services, which is having an adverse impact on the capex and opex of the upstream companies which significantly rely on services;

- Import of goods such as ocean freight and time charter will be taxable under Reverse Charge Mechanism (RCM). There is also a customs duty on freight cost for such imports;

- While the supply of natural gas is out of GST purview, the gas marketers have to pay GST on transmission tariffs which leads to complexities for them;

- The piped natural gas (PNG) continues to be taxable under VAT at a higher rate of 26-28% as compared to 18% GST on other competing liquid fuels. This is likely to negatively affect the sales of PNG.

- GST is levied on the stock transfer of petroleum products between two separately registered parties for which credit is not available. This increases the cost.

CONCLUSION: As gas is not under the ambit of GST, there is no input tax credit available. Further, the downstream industries are not able to claim the benefit of the tax credit of VAT paid on purchases of natural gas which is available for alternate fuels/feedstocks .Currently natural gas is taxed under the VAT regime with VAT ranging from 3 per cent to 20 per cent across states, the ministry said in a booklet it brought out to promote the use of the fuel in automobiles, household kitchens, and industries. If brought under GST, natural gas will attract a uniform rate of tax at the consumption point anywhere in the country after doing away with current rates of excise duty and VAT. So, it is important for Government as well as consumers to bring Petroleum Products under ambit of GST. This will lead to reduce tax on these products, ultimately the end users will be benefited.

Disclaimer: The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation. Some judgements of counts have been taken as it is available. Although care has been taken to ensure the accuracy, completeness, and reliability of the information provided, author assume no responsibility, therefore. Users of this information are expected to refer to the relevant existing provisions of applicable Laws and take appropriate advice of consultants. The user of the information agrees that the information is not professional advice and is subject to change without notice. Author assume no responsibility for the consequences of the use of such information.

Author Bio