Central Goods and Service Tax Act, 2017 (CGST) deems the services of a real estate developer under a development agreement as supply of service. The legislature has introduced various notifications and schemes time and again for taxing the said transaction. The scheme was amended vide notification no.3/2019 read with 4/2019 and 06/2019 all dated 29/03/2019. As per these notifications, GST on development agreements is exempt subject to certain conditions.

Recently, the Karnataka AAAR in the case of MAARQ Spaces Pvt Ltd.1 held that in a revenue sharing agreement the developer is providing taxable service to land owner. The value of the service is equivalent to the share of Developer in the market value of developed plots sold in the project. This decision was rendered on facts which were prior to the amended notifications.

This article analyse the contours of the GST chargeability to the revenue sharing development agreement in the light of:

a) the decision of MAARQ (supra) and;

b) the amended notifications.

and arrives at a conclusion that the amended notifications create a lot more issues for a revenue share development agreement.

FACTS OF THE CASE :

The Appellant developer entered into a Joint Development Agreement with Land Owners for development of land into residential plot layout along with specification and amenities. Land Owner executed separate agreements with customers for sale of developed plots of land for consideration. The parties shared the consideration in the ratio 75% : 25% between Land Owner and Developer respectively. The Appellant incurred the entire cost of development.

Question before AAR :

(a) Whether the activity of development and sale of plots by the Developer is a service to the Land Owner so as to attract GST ?

(b) If yes, whether provision of Rule 31 can be made applicable in ascertaining the value of land and supply of service ?

Developer’s contention before AAR :

(i) Sale of land is excluded from the definition of supply u/s. 7 of the CGST Act as per Schedule III Entry 5.

(ii) Sale of land + Development activity = “Composite supply” as defined in section 2(30) of the CGST Act.

(iii) Development activity is incidental to sale of land.

(iv) Development service rendered to the plot buyers and not to the land owner

(v) Sale consideration from the Buyer = Cost of land (not subjected to GST) + Development cost (subject to GST).

(vi) The Developer acquired 25% rights in total plots developed and sold

Thus, according to the Developer, the transaction was as under :

CHART 1

AAR Decision :

A. ISSUE NO.1 : Whether the activity of development and sale of plots by the Developer is a supply of service to the Land Owner so as to attract GST ?

The AAR analysed the terms and conditions of the JDA between the Land Owner and the Developer. It held that the activities undertaken by the Developer amount to a supply of service to the Land Owner and thus, liable for GST :

| Para no. | Terms of the Agreement | Analysis by AAR |

| Sale Agreement with buyer is incidental to activity of development of land | ||

| Para no. 9.4 | Developer has the necessary experience and expertise as a land developer. | Core competence of the Developer is to carry of activity which convert a raw piece of land into a well-developed residential layout. These activities change the character of the barren land and gives it a character of a marketable land. The Developer enters into a sale agreement with the Buyer for recovering his investment in development of land. Thus, the sale agreement is incidental to activity of development of land. |

| Developer has no right over the land and consequently, the Developer cannot claim to be engaged in the activity of sale of land under Schedule III Entry 5 : | ||

| Para 2.6 | Nothing contained in the agreement shall be construed as delivery of possession in part performance of any agreement of sale. | Thus, the Land Owner does not transfer the possession of land in the name of the Developer. |

| Para 4.2 | land owner alone shall apply to the government authorities to obtain sanctioned plans. | Law recognizes the landowners alone as the persons responsible for developing the land. The landowners have engaged the Developer to develop the land in accordance with the approvals. |

| Para 6 | Entire cost of development shall be borne by the Developer. | The Developer is engaged in theactivity of providing certain service to the landowners and the landowners will compensate the Developer for the same in accordance with the terms of the agreement. |

| Para 8 | Developer gets an amount on the sale of each individual plot. | The Developer cannot claim rights over any specific plots. The amount received from buyer is credited to an escrow account and thereafter divided. The share of Developer is towards the cost incurred in development and profit. |

| Para 12 | Developer stands indemnified by the landowners on any issue related to the title of the 1 and. | This again shows that the Developer has no claim on the title of any portion of the land. Once they have no right vested in them, they cannot hold themselves out as sellers of land as envisaged in Entry 5 of Schedule III.

The Developer can only be considered to have extended their services to the landowners in the sale of the Plots. |

The AAR held that Schedule III Entry 5 applies only to those persons who are the “owners” of the land and not to persons who are incidental to the sale of land. The Developer only had a right to the extent of 25% of the amounts received on account of sale of the plots towards the cost of development incurred by them. Thus development activities do not qualify to be covered under Entry 5 Schedule III of the CGST Act.

The AAR’s version of the transaction is depicted in the chart below

CHART 2

where T1, T2 and T3 are the three transactions involved in the facts of the case as under:

T1: Transfer of Development rights by the land owner to Developer

T2: Supply of development services by Developer to Land Owner

T3: Sale of developed plots by Land Owner to Buyer.

AAR concluded that Development service (T2 in above chart) is “supply” of service to the landowner. This service is held liable for CGST@18%.

B. ISSUE 2 : Value of supply of T2 :

The AAR adjudicated upon various clauses of the Development Agreement. It held that cost of execution of the development of the land shall be borne by the Developer. The Developer is to recover the cost from the purchasers of the Plots. The AAR observed that as and when any plot is sold, the proceeds will be divided between the Developer and the landowners in the agreed ratio. Therefore 25% share of revenue is the consideration received by the Developer for supply of service. Applying section 15 r.w. Rule 31 of the CGST Act the consideration is equal to 25% of the Market value of the plots.

The developer approached the Appellate authority (AAAR) seeking redressal.

Proceedings before AAAR :

The Developer reiterated the contentions raised before the AAR and made additional submissions:

| Sl.no. | Additional submission by Developer before AAAR | AAAR Verdict |

| (i) | Section 7 of the CST Act provides for scope of the term “supply”. The parties did not contract for supply of goods or services to each other. The Land Owner agreed to contribute land and Developer agreed to carry out development work and share revenue out of sale of developed plots to the prospective customers.

Therefore, Section 7 was inapplicable. |

The AAAR held that the expression “supply” induces all forms of supply of good or services or both such as sale, transfer, barter, exchange, license, rental, lease or disposal made or agreed to be made for a consideration by a person in the course of furtherance of business, and includes activities specified in Schedule II to the CGST Act, 2017. Therefore, the service of development carried out by the Developer was a supply of service to land owner since it was for consideration and in furtherance of business. |

| (ii) | There is no clause in the JDA which fixes a responsibility on the Land Owner to pay consideration to the Developer for development of land.Irrespective of the sale or not, the Appellant is liable to develop the said land. | Para 12. JDA indicates that the primary purpose of the agreement is for the Developer to develop the land. The agreement acknowledges that the expertise of the Developer in development of land is the reason the land owner approached the Developer for the JDA. The consideration for the development of land is in the form of the revenue earned from the sale of land. |

| (iii) | The supply, if at all, is a “composite supply”primarily in the nature of sale of land. It is exempt under Schedule III | The AAR held that JDA includes two transactions :

(a) sale of land (b) development of land. Combination of two activities, one of whic his not a supply under GST annot be said to be a composite supply u/s. 2(30). If the transaction of sale of land is coupled with another activity such as infrastructure works, then exclusion under Schedule III will not apply. |

| (iii) | A contract between the theatre owner and the distributor is on revenue sharing basis i.e. percentage of revenue earned from selling the tickets goes to the theatre owner and the balance goes to the distributor.

As per Circular no. 109/03/2009, dated 23/02/2009 under Service Tax the two contracting parties act on principal-to-principal basis and one does not provide service to another. |

JDA indicates that the primary obligation of the Developer is to develop the land. The consideration is collected from the sale proceeds as share of revenue. Thus, there is an element of supply of service u/s. 7 – Schedule II rendered by the Appellant Where JDA is entered into for the two parties to jointly reap the benefits of the sale of the land to customers, there is a clear rendering of services by the developer to land owner in developing the land which belongs to the land owner. |

CHART 3

AAAR held that the activity of developing land is a supply of service by the Appellant even under the revenue sharing arrangement and it cannot be said that no services were being rendered by the Developer to the land owner.

The key principles laid down by the AAAR are:

(i) Substance of the agreement between the parties is important to determine whether there is supply u/s. 7 of the CGST Act, 2017.

(ii) A transaction shall be out of GST net only if the activity is exclusively dealing with transfer of title or transfer of ownership of land, which is immovable property.

(iii) Where the developer is carrying out infrastructure work on the land, it will

be supply of service by developer to land owner.

Acelegal Analysis:

The erstwhile Service tax regime had issued Circular 151/2012 explaining the levy of Service Tax on the joint development agreements. Circular recognised two separate service providers i.e. the land owner and the Developer. The circular further recognised that both parties are collaborating with each other and providing service to the unit buyer. The transfer of Development rights by the land owner remained non-taxable (T1 in this article). The construction service provided by the developer to the owner (T2 in this article) entailed service tax as “construction service”. No service tax was levied in revenue sharing agreement since no constructed area was provided to Owner (no T2).

Under the GST regime Notification no. 04/2018 dated 24/01/2018 recognised the transfer of development rights by the land owner to the Developer as a separate taxable service. This continues in the amended notification no.4/2019 and 06/2019 dated 29/3/2019. Therefore, Transfer of development rights (T1) is taxable whether its area sharing model or whether its revenue sharing model. The construction services carried out by the Developer (T2) for land owner is taxable under area sharing model. But when no construction service is provided by the Developer to land owner in a revenue sharing model there is no T2 to levy tax on. Graphically put, in a revenue sharing model the transfer of development rights from land owner to developer is the only supply of service involved. There is no service by developer to land owner. Graphically put:

CHART 4

A new line of thinking has emerged from the decision of the AAAR in the case of MAARQ Spaces Pvt Ltd. (supra) The decision permits the authorities to tax a presumed supply of service by the Developer to the Land Owner even under the revenue share model of JDA. The entire share of revenue of Developer is deemed as taxable consideration for levy of GST.

Before Maarq Spaces Pvt. Ltd. (supra), AAR decided the case of M/s. Vidit Builders2 on identical question. In that case, the developer entered into a revenue sharing JDA with land owner for development of land. It was agreed that once the project is developed, the Developer would ensure sale of plots. The authority was to decide whether the work undertaken by the developer falls under Para 5 of Schedule III or should be classified as works contract? The developer argued that they are primarily engaged in sale of land and the said activity is not liable to be taxed in terms of Para 5, Schedule III. Therefore, merely by developing the common facilities, GST should not be attracted.

The AAR after considering the terms and conditions of JDA held that :

– Only if the seller it’s a title holder of the land, can claim that he is engaged in sale of land ;

– The developer has no right over the land or plots. The activities undertaken by the developer are in the nature of development of land into residential layout ;

– The developer can enter into a sale deed. However, this activity is incidental to the main activity of development of land.

Accordingly, the AAR held that the service provided by the Developer amounts to a supply of service as work contract. The value of said supply as per Rule 31 is equal to the amount received / receivable by the developer which is equal to his share in revenue on sale of plots.

Let’s see how these decisions apply to transfer of development rights on or after 01/04/2019 to a revenue sharing model :

1. Notification no. 3/2019 dated 29/03/2019 : Taxing Construction Service

This notification taxes the supply of construction service provided by the Developer to Land Owner in an area sharing model i.e. T2 in CHART 2. The notification only applies to the “landowner promoter” and the “developer promoter”. The notification defines the “landowner promoter” as under:

Explanation :

(i) “landowner- promoter” is a promoter who transfers the land or development rights or FSI to a developer- promoter for construction of apartments and receives constructed apartments against such transferred rights and sells such apartments to his buyers independently.”

(Emphasis Added)

Therefore, notification 3 should not apply to a revenue sharing development agreement since the landowner promoter is not receiving constructed apartments from the Developer. In other words there is no T2 in a revenue sharing agreement. For the same reasons the notification should not apply to development agreement for plotted development. The Notification 3 can be better explained as under:

CHART 5

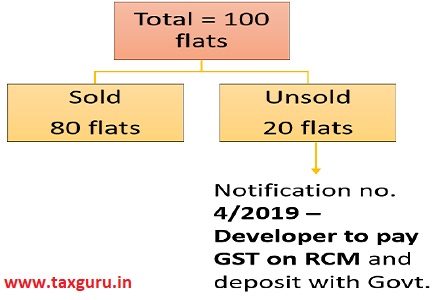

2. Notification no. 4/2019 dated 29/03/2019 : Taxing supply of Development Rights

This notification taxes the transfer of development rights by the Land Owner to the Developer. (T1 in CHART 2 ). The Developer Promoter is liable to pay GST on reverse charge basis on units that remain to be booked on the date of issuance of completion certificate. The Owner transfers the development rights to the developer even in a revenue share model of JDA and hence, this notification will apply to T1. The GST would be 18% on the value of development rights subject to a maximum of GST on unsold units at the time of receipt of occupancy certificate. Graphically put:

CHART 6

Now, when the entire constructed area developed by the Developer is getting taxed, logically there should be no further tax. But the decision of Maarq Spaces Pvt. Ltd. (supra), if applied, will result in GST charge on the presumed service provided by the Developer to the land owner (T2 in CHART 2). This will create an anomalous situation. The same transaction will get taxed twice i.e. T1 on the entire constructed area and T2 on the development service supplied by the developer to land owner separately. That too on the share of revenue received by the Developer out of sale consideration of the same constructed area. This is neither intended nor provided by legislature. Hence, the decision of Maarq Spaces Pvt. Ltd. (supra) will lead to double taxation of the same consideration.

The AAAR decision is also against the principle laid down by CESTAT in the case of Mormugao Port Trust v. CCE Goa3 wherein it was held that activities undertaken by a partner/ co-venturer for mutual benefit of the partnership/ joint venture cannot be regarded as a service rendered by one person to another for consideration and therefore, cannot be taxed under GST. While doing so, the court observed that whatever the partner does for the furtherance of the business of the partnership, he does so only for advancing his own interest as he has a stake in the success of the venture. There is neither an intention to render a service to the other partners nor is there any consideration fixed as a quid pro quo for any particular service of a partner. All the resources and contribution of a partner enter into a common pool of resource required for running the joint enterprise and if such an enterprise is successful the partners become entitled to profits as a reward for the risks taken by them for investing their resources in the venture.

CONCLUSION :

In a revenue sharing agreement, the land owner supplies land and the developer contributes in the form of development activity. Both parties together enter into a sale document with the buyer. It is the Buyer who is the ultimate receiver of the service and he pays GST as per the Notifications issued from time to time. Presently, the buyer pays GST being 1% / 5% after reducing 1/3rd rebate in respect of element of land.

The decision of AAAR in the case of Maarq Spaces Pvt. Ltd. (supra) will create litigation. The revenue authorities will heavily rely on the said decision to try and collect 18% on the share of revenue of the developer. Its need of the hour that a clarification is issued by the legislature at the earliest instead of leaving the Developers at the door step of the courts to slug it out.

Notes:

1. ORDER NO. KAR / AAAR-19 / 2020-21, DATED 04/05/2020

2. 09/2019 (MP AAR), order dt. 06/01/2020

3. TS-432-CESTAT-2016-ST

Author Bio

Informative and helpful. There is clear indication of double taxation on part of developer. Builder and developer association should asked for clarification else it will increase litigation on developer part.