Ms. Jaya Sharma-Singhania and Mr. Akash Deepak Tekale

INTRODUCTION:

GST (Goods & Services Tax), a single unified tax system aims at uniting India’s complex taxation structure to a ‘One Nation- One Tax’ regime. It is the biggest tax reform since India’s independence.

GST proposes to remove the geographical barriers for trading, and transform the entire nation to ‘One Common Market Place’. The GST will replace at least 17 state taxes that would make taxation of goods and services far simpler than the current system. GST would enable goodsn to be taxed at the point of consumption rather than production thus avoiding double taxation.

Once GST is implemented, consumers will not be subjected to the burden of double taxation; which mean that all taxes will be levied at the times of purchase will include both the central government’s taxes as well as the state government’s taxes. The move would deter state governments from indiscriminately increasing taxes.

GST LAW IN INDIA – A DETAILED HISTORY:

France was the world’s first country to implement GST Law in the year 1954. Since then, 159 other countries have adopted the GST Law in some form or other. In many countries, VAT is the substitute for GST, but unlike the Indian VAT system, these countries have a single VAT tax which fulfills the same purpose as GST.

In India, the discussion on GST Law was flagged off in the year 2000, when the then Prime Minister Atal Bihari Vajpayee brought the issue to the table.

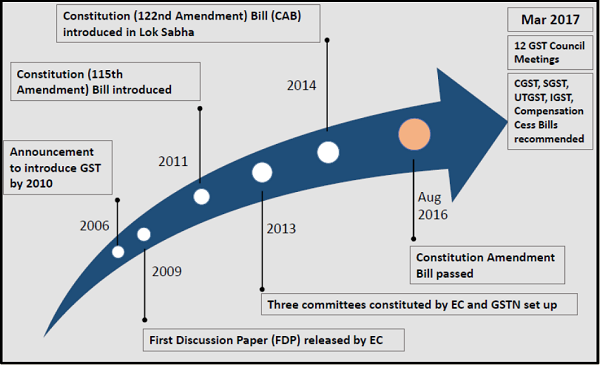

THE JOURNEY OF GST SO FAR:

INDIRECT TAX STRUCTURE PRIOR TO IMPLEMENTATION OF GST:

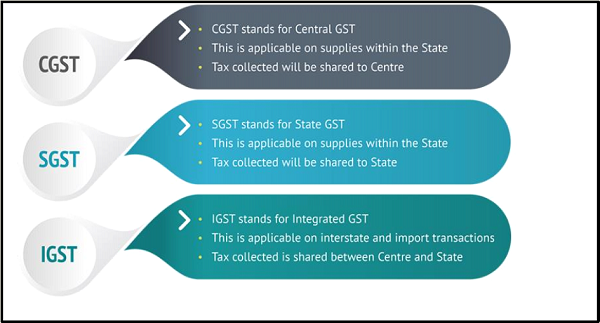

COMPONENTS OF GST:

TAX SUBSUMED UNDER GST:

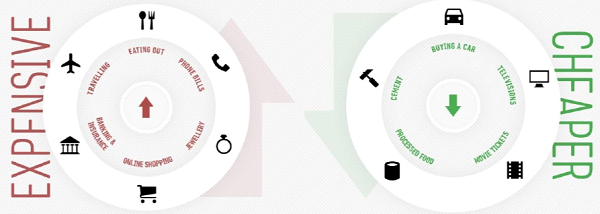

EFFECTS of GST:

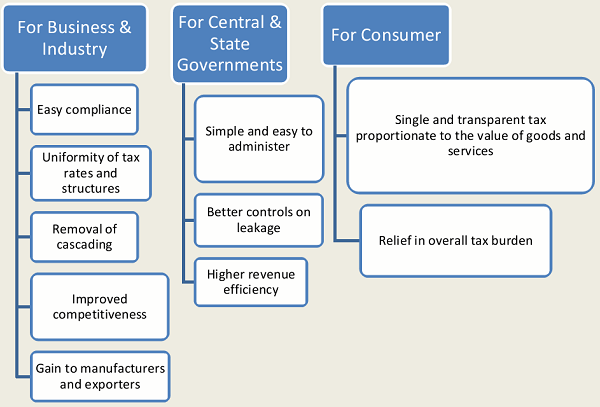

ADVANTAGES of GST

TAXABLE PERSON UNDER GST:

Under the GST law, a ‘taxable person’ is a person who carries on any business at any place in India and who is registered or required to be registered under the GST Act. Any person who engages in economic activity including trade and commerce is treated as taxable person.

‘Person’ here includes individuals, HUF, company, firm, LLP, an AOP/BOI, any corporation or Government Company, body corporate incorporated under laws of foreign country, co-operative society, local authority, government, trust, and artificial juridical person.

WHO IS LIABLE TO GET REGISTERED UNDER GST?

GST registration is mandatory for-

- Any business whose turnover in a financial year exceeds Rs 20 lakhs (Rs 10 lakhs for North Eastern and hill states);

[Note: If your turnover is supply of only exempted goods/services which are exempt under GST, this clause does not apply.]

- Every person who is registered under an earlier law (i.e., Excise, VAT, Service Tax etc.) needs to register under GST, too;

- When a business which is registered has been transferred to someone/demerged, the transferee shall take registration with effect from date of transfer;

- Anyone who drives inter-state supply of goods;

- Casual taxable person;

- Non-Resident taxable person;

- Agents of a supplier;

- Those paying tax under the reverse charge mechanism;

- Input service distributor;

- E-commerce operator or aggregator;

- Person who supplies via e-commerce aggregator;

- Person supplying online information and database access or retrieval services from a place outside India to a person in India, other than a registered taxable person.

TYPES AND DUE DATES OF GST RETURNS:

| Return Form | What to file? | By whom? | By when? |

| GSTR-1 | Details of outward supplies of taxable goods and/or services effected. | Registered Taxable Supplier | 10th of the next month |

| GSTR-2 | Details of inward supplies of taxable goods and/or services effected claiming input tax credit. | Registered Taxable Recipient | 15th of the next month |

| GSTR-3 | Monthly return on the basis of finalization of details of outward supplies and inward supplies along with the payment of amount of tax. | Registered Taxable Person | 20th of the next month |

| GSTR-4 | Quarterly return for compounding taxable person. | Composition Supplier | 18th of the month succeeding quarter |

| GSTR-5 | Return for Non-Resident foreign taxable person. | Non-Resident Taxable Person | 20th of the next month |

| GSTR-6 | Return for Input Service Distributor. | Input Service Distributor | 13th of the next month |

| GSTR-7 | Return for authorities deducting tax at source. | Tax Deductor | 10th of the next month |

| GSTR-8 | Details of supplies effected through e-commerce operator and the amount of tax collected. | E-commerce Operator/Tax Collector | 10th of the next month |

| GSTR-9 | Annual Return | Registered Taxable Person | 31st December of next financial year |

| GSTR-10 | Final Return | Taxable person whose registration has been surrendered or cancelled. | Within three months of the date of cancellation or date of cancellation order, whichever is later. |

| GSTR-11 | Details of inward supplies to be furnished by a person having UIN. | Person having UIN and claiming refund | 28th of the month following the month for which statement is filed |

ROLE OF COMPANY SECRETARIES IN GST:

Company Secretary is a competent professional and is provided exhaustive exposure by the institute through compulsory coaching, examination, rigorous training and continuing professional development programmes and is governed by the Code of Conduct contained in the Company Secretaries Act, 1980.

Company Secretaries can be authorised Representative in the following areas under GST:

- Issue Certificate certifying the fact of non-passing of the GST burden (Report for GST on refund process);

- Act as Authorised Representative in the matter of registration under Goods and Services Tax Act (Report on GST Registration);

- Act as an Authorised Representative for acting as an agent for the taxpayer (Report on GST Payment Process).

SUMMARY:

The idea behind having one consolidated indirect tax to subsume multiple currently existing indirect taxes is to benefit the Indian economy in a number of ways:

- It will help the country’s businesses gain a level playing field;

- It will put us on par with foreign nations who have a more structured tax system;

- It will also translate into gains for the end consumer who not have to pay cascading taxes anymore;

- There will now be a single tax on goods and services.

In addition to the above,

The Goods and Services Tax Law aims at streamlining the indirect taxation regime. As mentioned above, GST will subsume all indirect taxes levied on goods and service, including State and Central level taxes. The GST mechanism is an advancement on the VAT system, the idea being that a unified GST Law will create a seamless nationwide market.

It is also expected that Goods and Services Tax will improve the collection of taxes as well as boost the development of Indian economy by removing the indirect tax barriers between states and integrating the country through a uniform tax rate.