Overview

The composition scheme under GST, is for the small corporations, keeping into consideration, the challenges they face with regards to GST especially when their annual turnover is not above Rs 1 crore.

Provisions under the composition scheme is mentioned in Section 10 of the Central GST Act, 2017 and Chapter 2 of the CGST Rules, 2017.

GST Registration under the composition scheme is an essential aspect if these businesses want to benefit from the scheme.

Why Composition Scheme?

As mentioned in the overview, the purpose behind the introduction of the scheme in GST is to provide support to the smaller businesses, reduce their tax burdens and remove the GST compliance complexities.

Advantages offered

The scheme brings along with it some benefits –

- Limited compliance with the usual rules of GST

- Limited tax liability

- High liquidity

- Less number of records to be maintained

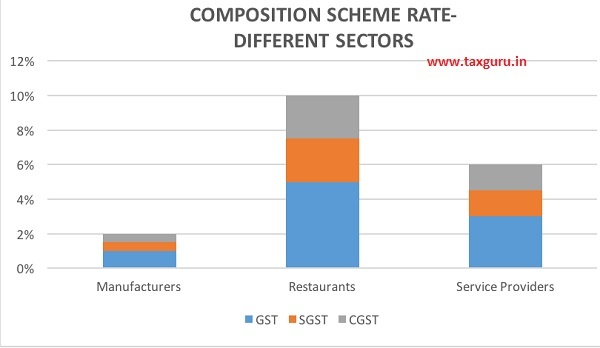

The ideal rate at which taxpayers would be charged is 6% which includes 3% CGST and 3% SGST.

Manufacturers – 1% (0.5% central and 0.5% state),

Restaurant services – 5% (2.5% central and 2.5 state),

Service providers – 3%

–

Composition scheme for service providers

The service providers have been granted benefits of the scheme too. The scheme was made available to them from 1 April 2019 as mentioned in the Form GST REG-01. Under this, they can now charge a rate of 6% from their customers as compared to the usual rates of 12% to 18%.

The service providers that have a turnover of up to Rs 50 lakhs are eligible to register for the scheme. They are expected to pay 6% GST.

The new rates will be applicable at the beginning of the financial year or at the time of new registration during a financial year.

Requirements for eligibility

- Turnover of less than Rs 50 lakh

- Supply of only taxable goods

- Normal taxpayers will fall under the ‘composition scheme’ category if 10% of the annual income is earned by providing a service.

Non-eligibility criteria

- Inter-state supplies

- Companies that carry out their business through e-commerce websites are not eligible

- Suppliers of ice cream, ice or products that contain cocoa, tobacco.

- Non-resident taxpayers

- Casual taxpayers

- Suppliers cannot charge tax from the customer

Penalty

The non-compliance to the rules of the scheme and providing incorrect data will result in huge amounts of penalty for the taxpayers. It will be charged as per the provisions of Section 73 and Section 74.

Changes in the composition scheme

Certain modifications were made in the composition scheme in the 32nd council GST Meeting –

- The annual turnover limit to be eligible for the scheme increased to Rs 1.50 Crores.

- The Annual GSTR 4 Return should be filed yearly not quarterly.

- Tax should be paid quarterly.

- The GST rate for the service providers of the annual income of up to Rs 50 Lakhs have increased from 3% to 6%.

Is it beneficial? A Cost analysis

Even though the scheme was introduced to make the operations of the smaller organizations less complicated, certain aspects of the scheme is hurting these businesses and proving to be a disadvantage.

Also, it does not seem to be quite working in the benefit of the smaller businesses and enterprises formally know as the Small and Medium Enterprises (SMSE) that are now struggling to survive.

These elements need to be highlighted too-

- Limiting business activities

Inter-state supplies are not allowed which will limit the capacity of the business to reach more customers.

- Input tax credit cannot be claimed on the purchases

The taxpayer is not allowed to take credit on his purchases and thus they are at a loss.

- Exempted goods cannot be supplied

The suppliers cannot supply goods that are exempted from GST which means restrictions with regards to the freedom of supplying goods and loss of money as the suppliers cannot finish up the stock of goods they currently have.

- Exemption of E-commerce business activities

Any business activity that takes place online does not fall under the composition scheme.

- Rates in the reverse charge mechanism

If the reverse charge is being implemented, the taxpayer has to pay tax at the normal rates.

- Quarterly payment of taxes and returns

The payment of GST returns as well as taxes have changed from paying annually to quarterly basis in the FORM GSTR-04 which is challenging for the small businesses.

- No issuance of taxable invoices as per GST law

The companies registered under the composition scheme cannot issue any invoices that are taxable.

- The suppliers cannot collect tax from their customers

There’s a need to understand as to how the last two points mentioned above have an effect on cost.

The suppliers have been categorized into three categories-

Category 1

- Non- taxable person (do not pay GST)

Category 2

- A person working under the composition scheme

Category 3

- Taxable persons

Category 1

The suppliers that supply goods to the non-taxable persons; there is no impact on cost at all as they do not have to pay any GST and Input Tax Credit (ITC) is not applicable.

Category 2

The suppliers that fall into the second category pay a fixed amount of GST, the amount of which is not to be collected from the customers. Also, the suppliers cannot claim any ITC which eventually increases their cost as they have goods with them.

Category 3

The suppliers supplying the goods to the taxable persons have the most impact on the cost.

Here’s how-

For instance, the cost of the good is Rs 200 and the GST rate is 18%. (Rs 36). The amount payable is Rs 236. The cost of production is Rs 236. He sells the product at Rs 300 at a margin of Rs 64. He does not have any ITC to be claimed or any GST to be collected from the customer.

Whereas, in the case that does not apply the composition scheme, the supplier can avail ITC as well as collect tax from the customer.

Conclusion

With the never-ending restrictions under the scheme, it does not seem to work in favour of the small businesses and prove to be helpful to make profits.

Micro and small businesses are still suffering and will continue to suffer under any new rule that comes along if appropriate measures are not taken to understand the consequences they might face in the future.