The term Export generally refers to Exports of Goods but that reference is a passé now. Export of Services is the emerging trend as it widens the scope of exports, bringing in the diversification and increasing India’s Foreign Exchange Earnings. The Indian Economy has witnessed a major boost in the last decade in the services sector.

India has emerged as the fastest growing nation in global services trade. It remained among the top 10 trading countries in commercial services in FY 2019-20 accounting for 3.5% of world services exports. Despite COVID 19 pandemic, India’s Services sector remained relatively resilient as compared to merchandise trade. As per the data released by Ministry of Commerce & Industry, the Gross Services Export receipts for the period April 2020 to March 2021 amounted to USD 202.57 Billion and the Net Services Export receipts stood at USD 85.81 billion for FY20-21. Export of Services contributed 41% of the total exports (merchandise plus services) made from India for FY 20-21.

Service sector’s significance in the Indian Economy has been steady. As per the Ministry of Statistics and Programme Implementation, Service Sector now accounts for over 54% share in Gross Value Added (GVA) of the economy and attracts almost 4/5th of total Foreign Direct Investment (FDI) inflows into India.

Exports under Goods and Service Tax (GST)

An Export in International Trade means Goods and Services produced in one country and sold to buyers in another country (Foreign buyer). Services being intangible in nature are different from export of goods. Goods are deemed to be exported once they cross the country’s border but it is not in the case of export of services.

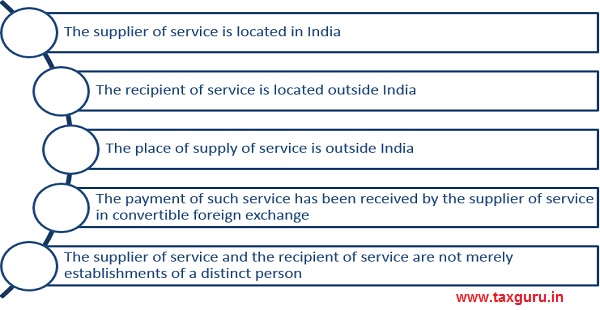

Section 2(6) of IGST Act defines Export of Services as supply of any service when

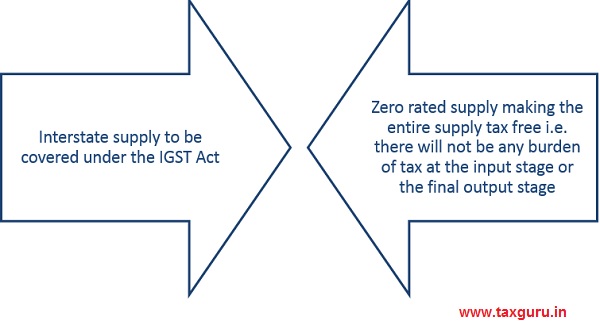

GST treats exports as:

Indian exports are becoming globally competitive basis the above treatment.

Zero rated supply will also include any supply of services to Special Economic Zone Unit/ Developer which means these supplies will have zero tax under GST. Supply of services to Nepal and Bhutan will be considered as export even if payment for such service is received in Indian Rupees, hence categorised as zero rated supply and will have all the benefits a zero rated supply enjoys under GST.

Zero rated supply cannot be equated with the supplies having 0% tax rate. As per CGST Act, no input credit can be claimed against supplies having 0% tax rate. But this restriction does not hold good for zero rated supply. For every exporter, it is mandatory to have GST registration i.e. a person who is unregistered under GST laws cannot make Zero Rated Supplies.

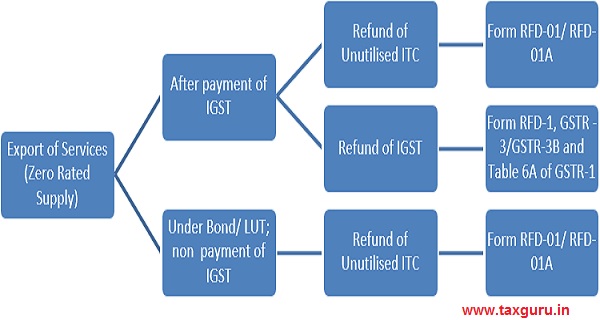

An Exporter has two options to comply with GST guidelines:

Option 1 – Export of Services after payment of IGST without any Bond or Letter of Undertaking (LUT)

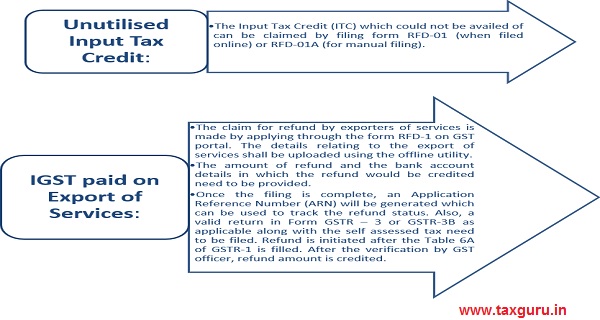

As per GST laws, exporter has the option to pay IGST on exports and claim for the refund later. There are two variants in the refund:

The refund can be claimed within 2 years from the relevant date

| S.No. | Type of Refund | Relevant Date |

| 1. | Tax paid on the services exported out of India | |

|

a. Supply of service is completed before payment is received |

Date of receipt of payment in convertible foreign exchange | |

|

b. Services received in advance prior to the date of issue of invoice |

Date of issue of invoice | |

| 2. | Unutilised Input Tax Credit | End of the Financial year in which claim for refund arises |

Option 2 – Export of Services without payment of IGST under a Bond or Letter of Undertaking (LUT)

A registered supplier also has an option to export services under Bond or Letter of Undertaking (LUT) and can claim refund of unutilised Input Tax Credit.

Earlier the facility of LUT submission was available to specified category of exporters but post release of GST Circular No. 8/8/2017 dated 4th Oct 2017 all the exporters were eligible for it except in few instances where it was required to furnish Bonds. Any person who is charged for a tax evasion of amount INR 2.5 Crore and above is not eligible for LUT. Also, in cases where taxpayer does not comply with the conditions specified in LUTs within the required time, Bonds need to be submitted. The validity of LUT is 1 year. A fresh LUT needs to be furnished every financial year. LUT can be submitted online while Bonds need to be furnished manually in hardcopy.

Registered Supplier can submit a Bond or LUT in a specified format in Form RFD-11 prior to the exports on the letterhead of registered supplier to the jurisdictional commissioner. Acknowledgement Reference number (ARN) is received once LUT is accepted. In case of Bonds, additionally a bond on stamp paper along with Bank Guarantee and other supporting documents will also be furnished. There is no need for a separate bond for each transaction, instead a Running Bond can be submitted in which terms and conditions remain same for all transactions. E.g. Taxpayer gives a Running Bond of INR 2 Crore. This means he can export services worth of tax up to INR 2 Crore in numerous transactions. Once the conditions of a particular transaction are met, the Bond is free for that amount and can be reused for next set of transactions.

This Bond or LUT is nothing but a kind of promise that a taxpayer makes to pay Taxes along with interest if services are not rendered within 1 year of issuing the export invoice. Tax needs to be paid within 15 days from the end of 1 year or such period as may be allowed by the commissioner. Once the services are rendered after 1 year, benefits are given back to the exporter.

Refund for unutilised Input Tax Credit can be claimed by filing the form RFD-01/ RFD-01A. It is permissible to claim refund even if exports are made after 1 year.

Exports of Services under FEMA

Exports of Services from India is governed by clause (a) of sub section (1) and sub section (3) of Section 7 of Foreign Exchange Management Act 1999 (42 of 1999) read with Foreign Exchange Management (Current Account Transactions) Rules, 2000 further read with FEMA Notification No 23(R)/2015-RB dated January 12, 2016. These Notifications released by Reserve bank of India along with prevailing Foreign Trade Policy released by Directorate General of Foreign Trade (DGFT) lays guidance to conduct Export Trade from India.

For Service Exports, Import Export Code (IEC) is not necessary except when the service provider is taking benefit under the Foreign Trade Policy (FTP). For instance, a Service Exporter needs to mandatorily have IEC as one of the pre requisites along with other requirements to apply for Service Exports from India Scheme (SEIS).

Unlike Export of Goods, in case of Service Exports none of the forms and declarations is applicable. Service Exporter can render services to overseas buyers without submission of any forms/declarations but is liable to realize the amount of foreign exchange due into India and adhere to the below guidelines.

Invoicing & Realization Timelines

> All Exports contracts shall be denominated either in freely convertible currency or Indian Rupees

> Export proceeds shall be realised in freely convertible currency.

> Export proceeds against specific exports may be realised in Indian Rupee provided funds are received through freely convertible vostro account of non-resident bank in any country other than member of Asian Clearing Union or Nepal or Bhutan. (vostro account is the account held by a foreign bank with a domestic bank in domestic currency)

> It is obligatory for Exporters to realize and repatriate full value of services into India within 9 months from the date of rendering service.

> RBI has allowed AD Category-I banks to extend the period for export realization beyond stipulated timelines up to a period of 6 months at a time

> In view of current Covid pandemic, the Government of India has increased the realization period to 15 months for service exports made till 31st July 2020.

Manner of Receipt & Payment

> Amount representing the full value of services exported shall be received through an AD Bank in the manner specified in notified vide Notification No. FEMA 14 (R)/2016-RB dated 02 May 2016.

> When payment for services rendered to overseas buyers is received during their visits:

-

- AD Category – I banks should receive the funds in their Nostro account ( Nostro account refers to an account that a bank holds in foreign currency in another bank) or

- Exporter can also arrange certificate from the Credit Card servicing bank certifying that it has received equivalent amount in Foreign Exchange or

- AD Category-I banks may also receive payment for exports made out of India by debit to the credit card of an importer where reimbursement from the card issuing bank will be received in foreign exchange.

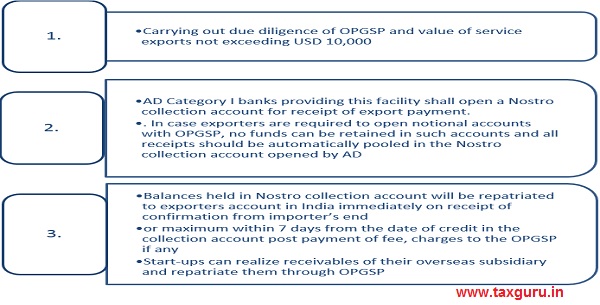

Exports receipts through Online Payment Gateway Service Providers (OPGSPs)

AD Category-I banks have been allowed to offer the facility of export realization by entering into standing arrangements with OPGSPs adhering to following conditions:

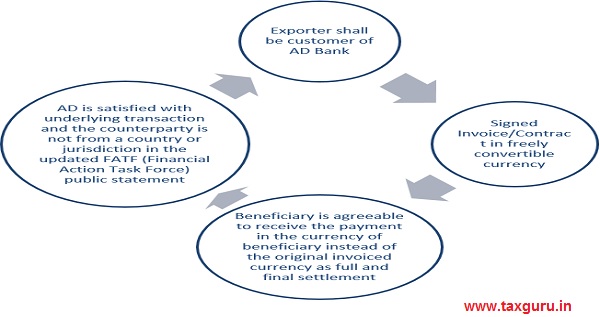

Settlement of Export Transactions in Currencies not having direct exchange rate

Exports invoices raised in freely convertible currency can also be settled in the currency of beneficiary which though convertible does not have direct exchange rate subject to below conditions:

Receipt of Advance against Exports

> Exporter receiving an advance payment from a buyer outside India should ensure to render the services within 1 year from the date of receipt of advance

> Rate of Interest (in case payable) on such advance payment cannot exceed London Inter-Bank Offered Rate (LIBOR) + 100 basis points

> In case the exporter fails to render the services partially or fully within the stipulated time frame, refund of advance payment post 1 year would require prior approval of RBI

AD Category-I banks may allow Exporter to receive advance payment for a period beyond 1 year where export of services will take more than 1 year and the export agreement allows such time frame

*****

About the Author

Author is Ruchika Bhagat, FCA helping foreign companies in setting up and closure of business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants, is a well-established Chartered Accountancy firm founded in the year 1997 with its head office at New Delhi.

Author is Ruchika Bhagat, FCA helping foreign companies in setting up and closure of business in India and complying with various tax laws applicable to foreign companies while establishing a business in India. Neeraj Bhagat & Co. Chartered Accountants, is a well-established Chartered Accountancy firm founded in the year 1997 with its head office at New Delhi.

what ere the tax rate for International vender for Technical testing of material (Metal) if the vender paid in US $

Does a person require GST registration for exporting exempt services.

“The export of services can be made without the payment of tax, subject to fulfilment of certain conditions. Therefore, the value of the export shall be the transaction value as declared by the exporter taking into account all discounts and rebate, provided that the price is the sole consideration and is not made to the related party.

In short, discounts can be applied on such services without having any impact on GST.”

mam,

can we give rebate and discount of 25 ℅ on export of services. if yes then what will be tax implications.

“The export of services can be made without the payment of tax, subject to fulfilment of certain conditions. Therefore, the value of the export shall be the transaction value as declared by the exporter taking into account all discounts and rebate, provided that the price is the sole consideration and is not made to the related party.

In short, discounts can be applied on such services without having any impact on GST.”

What is applicability of GST on Service received by Indian company in a foreign country where service provided by Indian company and payment made in India