1.1. INTRODUCTION TO DUAL GST MODEL

Many countries in the world have a single unified GST system i.e. a single tax applicable throughout the country. However, in federal countries like Brazil and Canada, a dual GST system is prevalent whereby GST is levied by both the federal and state or provincial governments. India is a federal country, which means there’s a division of power between the federal government and the state governments. Before GST, this meant that each state had its own tax system in addition to the central government’s tax system. As a result, business owners had to deal with a variety of complicated state and federal taxes for each sale. Since the taxes were often levied over each other, you ended up paying tax on tax, a problem called cascading taxes.

The GST regime replaces those confusing taxes with a single, nationwide tax rate. This is intended to unify India’s tax system, make it easier to do business, and reduce prices for consumers. Because of India’s federal structure, dual GST model had been adopted. This means GST is administered by the central government and the states.

In India, a dual GST is proposed whereby a Central Goods and Services Tax (CGST) and a State Goods and Services Tax (SGST) will be levied on the taxable value of every transaction of supply of goods and services.

1.2. MEANING OF DUAL GST MODEL

Dual GST means that GST will be levied simultaneously by Center and State Governments. Hence, every transaction of supply of goods or services shall suffer Central GST (CGST) and State GST (SGST), when the transaction is within the State. However, when the transaction is between states, there will be Integrated GST (CGST + SGST), which will be collected by the Central Government and then the SGST component paid to the State Government where the goods or services have been consumed.

Dual GST is preferred in countries where there is a federal structure of the government. As in this system states would be independent in their revenue sources and they don’t have to rely on center to share the revenues that they collect. This is important as it will reduce the conflict between center and state over revenue distribution.

Example — If a dealer in Rajasthan, selling goods to consumers within the state, makes a sale of INR 20,000 at 18% GST rate. Then the dealer will collect INR 3,600 as total tax. In this case CGST and SGST will be shared by Centre and State equally as INR 1,800 each.

1.3. WHY IS DUAL GST MODEL IS REQUIRED IN INDIA?

India is a federal country where both the Centre and the States have been assigned the powers to levy and collect taxes through appropriate legislation. Both the levels of Government have distinct responsibilities to perform according to the division of powers prescribed in the Constitution for which they need to raise resources. A dual GST will, therefore, be in keeping with the Constitutional requirement of fiscal federalism.

1.4. TYPES OF DUAL GST MODEL:

Normally, there is two type of Dual GST Model. Which are as follows.

Non Concurrent Dual GST Model: In Non Concurrent Dual GST Model Centre levies GST on services and levies GST on goods.

Concurrent Dual GST Model: Tax levied by Centre & state on the both goods and services. This model is adopted in many countries. For example, Brazil, Canada and India. Therefore, India has adopted a Dual GST Model in view of the federal structure of the country.

India has adopted “Concurrent dual GST” model. The need for Dual GST model is based on the following premise:

- In the pre GST framework, both levels of Government, that is, Centre and State, as per Constitution held concurrent powers to levy tax on domestic goods and services.

- The Concurrent Dual GST model would be a dual levy imposed concurrently by the Centre and the States, but independently;

- Both Centre and State will operate over a common base, that is, the base for levy and imposition of duty/tax liability would be identical.

1.5. STRUCTURE OF DUAL GST MODEL

As discussed above, the GST in India is a Dual GST framework, wherein, Centre will levy and administered CGST & IGST, while respective state/ Union Territory will levy and administer SGST/UTGST. This structure discussed as under;

Summary Chart of Structure of Dual GST Model

| Name | Explanation | Levied By | When? |

| CGST | Central Goods and Service Tax | Central Government | On INTRA State supply of Goods and Services. |

| SGST/ UTGST | Sate Goods and Service Tax / Union Territory Goods and Service Tax | State/

Union Territories |

On INTRA State supply of Goods and Services. |

| IGST | Integrated Goods and Service Tax | Central Government | On INTER State supply of Goods and Services. |

1. CGST (Central Goods and Service Tax) : CGST is a tax levied on Intra State supplies of both goods and services by the Central Government and will be governed by the CGST Act. SGST will also be levied on the same Intra State supply but will be governed by the State Government.

This implies that both the Central and the State governments will agree on combining their levies with an appropriate proportion for revenue sharing between them. However, it is clearly mentioned in Section 8 of the GST Act that the taxes be levied on all Intra-State supplies of goods and/or services but the rate of tax shall not be exceeding 14%, each.

2. SGST (Sate Goods and Service Tax ): SGST is a tax levied on Intra State supplies of both goods and services by the State Government and will be governed by the SGST Act. As explained above, CGST will also be levied on the same Intra State supply but will be governed by the Central Government.

Note: Any tax liability obtained under SGST can be set off against SGST or IGST input tax credit only.

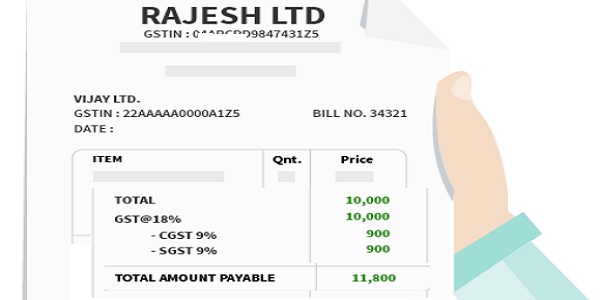

An example for CGST and SGST:

Let’s suppose Rajesh is a dealer in Maharashtra who sold goods to Anand in Maharashtra worth Rs. 10,000. The GST rate is 18% comprising of CGST rate of 9% and SGST rate of 9%. In such case, the dealer collects Rs. 1800 of which Rs. 900 will go to the Central Government and Rs. 900 will go to the Maharashtra Government.

3. UTGST (Union Territory Goods and Services Tax): UTGST is just the way similar to SGST. The only difference is that the tax revenue goes to the treasury for respective administration of union territory where the goods or services have finally been consumed. There is a key difference between union territory and states. The Union Territory directly comes under the supervision of the Central Government and does not have its own elected government as in case of States.

UGST is also charged at the same rates that of CGST. But, amongst UTGST or SGST only one at a time shall be levied together with CGST in each case.

Currently, there are 8 union territories in India:

- Lakshadweep

- Dadra and Nagar Haveli and Daman and Diu

- Andaman and Nicobar Islands

- Delhi

- Puducherry

- Ladakh

- Jammu & Kashmir

But out of these Delhi and Puducherry levy SGST and not UTGST because they have their own elected members and Chief Minister. Hence, they function as partial – states. As the SGST Act cannot be applied on a union territory which does not have its own legislature. The UTGST Act has been introduced by the GST Council

4. IGST (Integrated Goods & Service Tax): Under GST, IGST is a tax levied on all Inter-State supplies of goods and/or services and will be governed by the IGST Act. IGST will be applicable on any supply of goods and/or services in both cases of import into India and export from India.

Note: Under IGST,

- Exports would be zero-rated.

- Tax will be shared between the Central and State Government.

An example for IGST:

Consider that a businessman Rajesh from Maharashtra had sold goods to Anand from Gujarat worth Rs. 1,00,000. The GST rate is 18% comprised of 18% IGST. In such case, the dealer has to charge Rs. 18,000 as IGST. This IGST will go to the Centre.

1.6. DIFFERENCE BETWEEN SGST, CGST AND IGST

| Criteria of Distinction |

SGST | CCGST | IGST |

| Full Form

|

SGST stands for State Goods and Services Tax | CGST stands for Central Goods and Services Tax | IGST stands for Integrated Goods and Services Tax. |

| Meaning

|

SGST is one of the components of GST levied and collected by the respective state government on intra-state supplies. Such a tax is governed by State Goods and Services Tax Act, 2017.

|

CGST is another component of GST levied and collected by central government on intra-state supplies. Such a tax levy is governed by the Central Goods and Services Tax Act, 2017.

|

IGST is the third component of GST levied and collected by only central government on inter-state supply of goods or services.

The tax so collected is then apportioned between Central government and respective State Government where goods are consumed. Such a tax levy is governed by Integrated Goods and Services tax Act, 2017. |

| Applicability

|

SGST is applicable in case of intra-state supplies where the location of the supplier and place of supply are in the same state or UT.

|

CGST is also applicable in case of intra-state supply where the location of the supplier and place of supply are in the same state or UT.

|

IGST is applicable in case of inter-state supply where the location of the supplier and place of supply are in: (i) two different states (ii) two different UTs and (iii) a state and UT. |

| Taxes Replaced

|

SGST replaces:

• VAT (Value Added Tax) or Sales tax • Luxury Tax • Octroi • Entertainment Tax • Purchase Tax • Tax on betting or gambling or lottery |

CGST replaces:

• Central Excise Duty • Service Tax • Additional Customs Duty • Additional Excise Duty • Excise duty imposed under medicinal and • Special additional duty of customs |

|

| Who Collects the Tax |

SGST is collected by the respective state government. | CGST is collected by the Central government. | IGST is collected by the Central government. |

| Claim of ITC

|

The claim of SGST credit is available only against SGST and IGST in the same order. | The claim of CGST is available only against CGST and IGST in the same order. | The claim of IGST is available against IGST, CGST and SGST in the same order. |

| Applicability of Composition Scheme

|

A registered taxpayer can apply for the Composition Scheme if his aggregate annual turnover is upto Rs.1.5 crores | A registered taxpayer can apply for the Composition Scheme if his aggregate annual turnover is upto Rs.1.5 crores | Composition scheme is not applicable in case of inter-state supplies

|

| Registration Limit

|

Taxpayer is not required to register under GST if his aggregate annual turnover is up to Rs. 40 lakhs in case of supply of goods, 20 lakhs in case of supply of services and 20 lakhs in case of supply of both goods and services in special category states | Taxpayer is not required to register under GST if his aggregate annual turnover is up to Rs. 40 lakhs in case of supply of goods, 20 lakhs in case of supply of services and 20 lakhs in case of supply of both goods and services in special category states | Registration under GST is mandatory in case on inter-state supplies |

1.7. SALIENT FEATURES OF DUAL GST MODEL

The following points describes the Salient features of Dual GST Model:

- GST shall have two components one levied by the Centre (referred to as Central GST), and the other levied by the States (referred to as State GST)

- Central GST and the State GST would be applicable to all transactions of goods and services

iii. Central GST and State GST are to be paid to the accounts of the Centre and the States individually

- Central GST and State GST are to be treated individually, therefore taxes paid against the Central GST shall be allowed to be taken as input tax credit (ITC)

- Cross utilization of ITC between the Central GST and the State GST would not be permitted except in the case of inter-State supply of goods and services Cross utilization of ITC between the Central GST and the State GST would not be permitted except in the case of inter-State supply of goods and services

- Credit accumulation on account of refund of GST should be avoided by both the Centre and the States except in the cases such as exports, purchase of capital goods, input tax at higher rate than output tax etc.

- Uniform procedure for collection of both Central GST and State GST would be prescribed in the respective legislation for Central GST and State GST.

- Composition/Compounding Scheme for the purpose of GST should have an upper ceiling on gross annual turnover and a floor tax rate with respect to gross annual turnover.

- The taxpayer would need to submit periodical returns, in common format as far as possible, to both the Central GST authority and to the concerned State GST authorities.

- Each taxpayer would be allotted a PAN-linked taxpayer identification number with a total of 14/15 digits.

1.8. BENEFITS/ ADVANTAGES OF DUAL GST MODEL

The Dual GST is a simple and transparent tax with one or two CGST and SGST rates. The dual GST is already proved and provides the results in:-

- reduction in the number of taxes at the Central and State level

- decrease in effective tax rate for many goods

- removal of the current cascading effect of taxes

- reduction of transaction costs of the taxpayers through simplified tax compliance

- increased tax collections due to wider tax base and better compliance

Author Bio

Very beautiful explainatiin.

Thanks sir

Your obedient student

Prem Kumar

Muzaffarpur, Bihar