Article explains Meaning of Insurance, Requirements of Insurance Contract, Principles of Insurance Contract, Benefits of Insurance Contract, Types of Insurance and Life Insurance, its benefits & types.

Insurance

Insurance can be defined as—-

- transferring or lifting of risk

- from one individual to a group and

- sharing of losses on an equitable basis by all members of the group.

In legal terms Insurance is a contract (Policy) in which one party (Insurer) agrees to compensate another party (Insured) of its losses for a consideration (Premium).

WHY INSURANCE ?

> Financially Security

> Transfer of Risk

> Complete Protection for You and Your Family

> No More Stress or Tension During Difficult Times

> Some Types of Insurances are Compulsory(Like Motor Insurance, Transit Insurance, Third Party Insurance etc.)

> Peace of Mind

Requirements of an Insurance contract:

> An Agreement: Agreement must be an important element of the insurance contract. Without an agreement a contract is not valid.

> Valid Parties to the contract: The parties must have legal capacity to contract. Minors, lunatics, insolvents, intoxicated persons, etc. do not have the legal capacity and cannot have the legal capacity and cannot enter into an insurance contract.

> Valid offer and acceptance: There should be a valid offer and acceptance.

> Valid Consideration: there must be exchange of consideration in response to an agreement which defines the quantum of possible losses to the insured. The premium amount paid by the Insured by way of consideration on the basis of policy risk insured. The Insurer’s consideration will be a promise to indemnify the loss of the insured on the occurrence of the insured’s risk

Nature of INSURANCE Contract

Nature of contract is a fundamental principle of insurance contract. An insurance contract comes into existence when one party makes an offer or proposal of a contract and the other party accepts the proposal. A contract should be simple to be a valid contract. The person entering into a contract should enter with his free consent.

The followings are the characteristics of Insurance Contract;

> Aleatory Contract (Dependent on Chance) : The insurance contract is fully dependent on chances. It means that, if the loss arises, compensation is paid by the insurer on the occurrence of peril. If it does not occur Insurer does not pay any compensation while the premium gets paid to the insurer.

> Conditional Contract: Insurance contracts laydown conditions like providing proof of insurable interest, immediate communication of loss, proof of loss and payment of premium by the insured.

> Contract of Adhesion (Strong attachment to Causes) : Legally obligatory on the part of the insurer to explain the terms of the contract fully to all the parties. This is particularly important as under contract of adhesion, any ambiguity in the wording of the agreement will be interpreted against the insurer as he had laid down the terms.

> Unilateral Contract: Insurer is the only party to the contract who makes promises that can be legally enforced.

Principles of Insurance

1. Principle of Utmost Good Faith

2. Principle of Insurable Interest

3. Principle of Indemnity

4. Principle of Contribution

5. Principle of Subrogation

6. Principle of Loss Minimization

7. Principle of Causa Proxima (or Principle of Proximate Causes)

Principles of Insurance

1. Principles of Utmost Good Faith

> Both parties, insurer and insured should enter into contract in good faith.

> Insured should provide all the information that impacts the subject matter

> Insurer should provide all the details regarding insurance contract

For example – John took a health insurance policy. At the time of taking policy, he was a smoker and he didn’t disclose this fact. He got cancer. Insurance company won’t pay anything as John didn’t reveal the important facts.

2. Principle of Insurable Interest

> Insured must have the insurable interest on the subject matter.

> In case of life insurance spouse and dependents have insurable interest in the life of a person. Corporations also have insurable interests in the life of it’s employees

> In case of life or marine insurance, insured must be the owner both at the time of entering of entering into the insurance contract and at the time of accident.

3. Principle of Indemnity

> Insured can’t make any profit from the insurance contract.

> Insurance contract is meant for coverage of losses only.

> Indemnity means a security to put the insured in the position as he was before accident

> This principle doesn’t apply to life insurance contracts

4. Principle of Contribution

In case the insured took more than one insurance policy for same subject matter, he/she can’t make profit by making claim for same loss more than once

For example – Raj has a property worth Rs.5,00,000. He took insurance from Company ‘A’ worth Rs.3,00,000 and from Company ‘B’ – Rs.1,00,000.

In case of accident, he incurred a loss of Rs.3,00,000 to the property. Raj can claim Rs. Rs.3,00,000 from ‘A’ but after that he can’t make profit by making a claim from Company B. Now Company A can make a claim from Company B to for proportional loss claim value.

5. Principle of Subrogation

The principle of subrogation enables the insured to claim the amount from the third party responsible for the loss. It allows the insurer to pursue legal methods to recover the amount of loss,

For example, if you get injured in a road accident, due to reckless driving of a third party, the insurance company will compensate your loss and will also sue the third party to recover the money paid as claim.

6. Principle of Loss Minimization

This principle states that the insured must take all the necessary steps to minimize the losses to inured assets.

For example – Ram took insurance policy fo his house. In an cylinder blast, his house burnt. He should have called nearest fire station so that the loss could be minimized.

7. Principle of Causa Proxima (or Principle of Proximate Causes)

> Word “Cause Proxima” means “Nearest Cause”

> An accident may be caused by more than one cause. In case property insured for only one cause. In such case nearest cause of the accident is found out.

> Insurer pays the claim money only if the nearest cause is insured.

Assignment Questions:

1. What is an Insurance Contract ? Explain requirements of Insurance Contract.

2. Explain various principles of Insurance Contract.

BENEFITS OF INSURANCE

1. RISK MINIMISATION

2. FUTURE INVESTMENT

3. TAX BENEFITS

4. FAMILY SUPPORT

5. ECONOMIC DEVELOPMENT OF THE COUNTRY

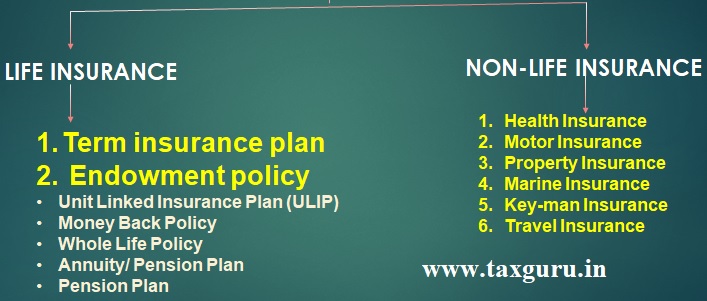

TYPES OF INSURANCE

LIFE INSURANCE

- Life Insurance is an arrangement between the Insurance company/Government which guarantees of compensation for loss of life in return for payment of a specified premium.

- In Life Insurance, the beneficiary whose name has been mentioned in the contract receives the specified sum, from the insurer in case of happening of the event i.e. Loss of Life

BENEFITS OF LIFE INSURANCE

> Risk Coverage: Insurance provides risk coverage to the insured family in form of monetary compensation in lieu of premium paid.

> Difference plans for different uses: Insurance companies offer a different type of plan to the insured depending on his need for insurance. More benefits come with the more premium.

> Cover for Health Expenses: These policies also cover hospitalization expenses and critical illness treatment.

> Promotes Savings/ Helps in Wealth creation: Insurance policies also come with the saving plan i.e. they invest your money in profitable ventures.

> Guaranteed Income: Insurance policies come with the guaranteed sum assured amount which is payable on happening of the event

> Loan Facility: Insurance companies provide the option to the insured that they can borrow a certain sum of amount. This option is available on selected policies only.

> Tax Benefits: Insurance premium is tax deductible under section 80C/80D of the income tax Act, 1961

TYPES OF LIFE INSURANCE

Term-Life insurance plan

As the name says Term insurance plan are those plan that is purchased for a fixed period of time, say 10, 20 or 30 years. As these policies don’t carry any cash value their policies do not carry any maturity benefits, hence their policies are cheaper as compared to other policies. This policy turns beneficial only on the occurrence of the event.

FETURES OF TERM-LIFE INSURANCE:

> It is purchased for a fixed term ie. 10, 15,20,30 years .

> The payment of premium can be fixed or recurring in nature.

> No loss,No Claim, that means, This policy turns beneficial only on the occurrence of the event. If there is no death occur during the term, the insured can not clam any amount.

> Claim Process:

Case-1: If No Loss : No Claim, Whole premium paid will be forfeited.

Case-2: If loss occurred : His Nominee will calm the Insurance and they. will get the amount of Sum Assured

Example of Term-Life Insurance Plan

Mr. X (Age 25 Years) purchased a Term-Life insurance plan for 25 years with a premium of Rs.5000 per annum. The company fixed the Sum Assured of Rs.2,00,000. Calculate the claim amount in following cases.

1. Death occurred at the age of 30 Years

2. Death Occurred at the age of 51 years

3. No Death occurred.

| Particulars | Case-1:Death at the age of 30 | Case-2: Death at the age of 51 | Case-3: No Death occurred. |

| Total Premium Paid | (5000 x 5 years)=25,000 | (5000 x 25 years)=1,25,000 | (5000 x 25 years)=1,25,000 |

| Claim Amount | Rs.2,00,000 | NIL | NIL |

| Net Gain/(Loss) | Gain=Rs.2,00,000-25,000 = 1,75,000 | Loss = Nil-125000 = (125000) | Loss = Nil-125000 = (125000) |

“In this case, only Death benefit, no Survival benefit will be provided”

Endowment policy:

The only difference between the term insurance plan and the endowment policy is that endowment policy comes with the extra benefit that the policyholder will receive a lump sum amount in case if he survives until the date of maturity. Rest details of term policy are same and also applicable to an endowment policy.

Endowment policy = Death Benefits + Survival Benefits (i.e. Maturity on Investment)

FETURES OF TERM-LIFE INSURANCE:

> It is purchased for a fixed term ie. 10, 15,20,30 years .

> The payment of premium can be fixed or recurring in nature.

> Both Death & Survival Benefits: In case of No Loss (No Death), he can not claim the sum assured but he will get a lump-sum amount (ie. Principal Amount + Interest) at the maturity with Bonus if any.

But in case of Death, his nominee will claim the Sum Assured+ Principal Amount + Interest till death + Bonus if any.

Example of Endowment Policy

Mr. X (Age 25 Years) purchased an Endowment Policy for 25 years with a premium of Rs.5000 per annum.

The company fixed the Sum Assured of Rs.2,00,000 and at the maturity, he will get 80% of Total Premium Plus interest @10% Per annum as survival benefit. Calculate the claim amount in following cases.

1. Death occurred at the age of 30Years

2. Death Occurred at the age of 51 years

3. No Death occurred.

| Particulars | Case-1:Death at the age of 30 | Case-2: Death at the age of 51 | Case-3: No Death occurred. |

| Total Premium Paid (a) | (5000 x 5 years)=25,000 | (5000 x 25 years)=1,25,000 | (5000 x 25 years)=1,25,000 |

| Claim Amount(Death Benefit) (b) | Rs. 2,00,000 | NIL | NIL |

| Survival Benefit (c) (Note-1) | Rs. 26,442 | Rs.1,43,339 | Rs.1,43,339 |

| Total Benefit (b + c) | Rs. 2,26,442 | Rs.1,43,339 | Rs.1,43,339 |

| Net Gain/(Loss) |

Note-1: Computation of Survival Benefits under Endowment Policy

| Particulars | Case-1:Death at the age of 30 | Case-2: Death at the age of 51 | Case-3: No Death occurred. |

| Total Premium Paid (a)

(Rs.5000 P.a.) |

(5000 x 5 years)=25,000 | (5000 x 25 years)=1,25,000 | (5000 x 25 years)=1,25,000 |

| Principal Amount (b) (80% 0f (a) above) (as per the question)** | =25000 x 80% = 20000 | =125000 x 80% = 1,00,00 | =125000 x 80% = 1,00,000 |

| Interest on Investment (c)

[@ 10% on Rs.4000P.a. ,i.e.(5000P.a x 80%) Compounded annually.] |

=4000(1+0.10)5 =6442 | =4000(1+0.10)25 = 43339 | =4000(1+0.10)25 = 43339 |

| Total Survival Benefit (b + c) | =20000 + 6442= 26442 | =100000 + 43339= 143339 | =100000 + 43339= 143339 |

** The Principal amount may be varies from Company to Company . Normally the principal amount is less then the Total premium Paid. That’s why, we have taken as 80% of the Premium Paid.

*** The Rate of interest may be varies from company to company.

Author Bio

Very clear and right explanation…

🙏