In pursuance of the Press release dated 24th March 2020 wherein Government has announced various relief measures to mitigate the severe blow caused by the outbreak of COVID-19 across India and insertion of Section 168A in CGST Act, 2017 by way of an Ordinance, 2020 dated 31st March 2020, the Government, on 3rd April 2020 issued 7 Notifications and 1 Circular outlining relief measures under GST. The same is summarized below:

Page Contents

- A. Relaxation in 10% restriction for a few months under Rule 36(4) of CGST Rules 2017

- B. Extension in validity of E-way bills issued between 20th March 20 to 15th April 20

- C. Conditional waiver of Interest and late fee relating to GST returns and revised due dates to file GSTR-3B for May 2020

- D. Extension in due date for Composition Taxpayers

A. Relaxation in 10% restriction for a few months under Rule 36(4) of CGST Rules 2017

Current Rule

Without going into the controversies around Rule 36(4), as per the requirements of this Rule, Input tax credit claimed in GSTR-3B every month cannot exceed 110% of eligible credit appearing in GSTR-2A.

Relief by way of insertion of Proviso in Rule 36(4)

The condition of availment of ITC in GSTR-3B to the extent of 110% of the total eligible ITC appearing in GSTR-2A has been deferred for February 2020 to August 2020 and the same shall not be required to be fulfilled monthly but on a cumulative basis. That is, input tax credit as per tax paid documents available with the taxpayer subject to other conditions of availment of ITC as per Section 16 of the CGST Act, 2017 can be claimed irrespective of the amount appearing in GSTR-2A during the filing of GSTR-3B for the aforesaid months.

Accordingly, taxpayers need to do final adjustments in ITC availed while filing GSTR-3B for September 2020, i.e. in case of excess ITC is availed by the taxpayers then such excess ITC shall be adjusted while filing GSTR-3B for September 2020.

Comments: It is a welcome relief and will provide an interim breather to the taxpayers in their working capital position. However, it is suggested that inspite of the above relaxation, the taxpayers should continue doing GSTR-2A reconciliation every month and push the suppliers to file GSTR-1 in a timely manner.

B. Extension in validity of E-way bills issued between 20th March 20 to 15th April 20

The nation-wide lockdown was announced at 8 p.m. on 24th March 2020 w.e.f. 25th March 2020 giving only 4 hours to 1.35 billion Indians to stay at their homes. This entailed complete business disruption and a temporary halt in the movement of the goods-in-transit and uncertainty in their arrival to the intended destination at the time of announcement of lockdown and consequent expiry of the e-way bills.

To address this issue, the Government by CGST Notification No. 35/2020 dated 03.04.2020 notified that where an e-way bill has been generated under Rule 138 of the CGST Rules, 2017 and its period of validity expires during the period 20th day of March 2020 to 15th day of April 2020, the validity period of such e-way bill shall be deemed to have been extended till the 30th day of April 2020.

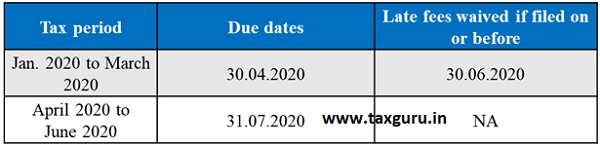

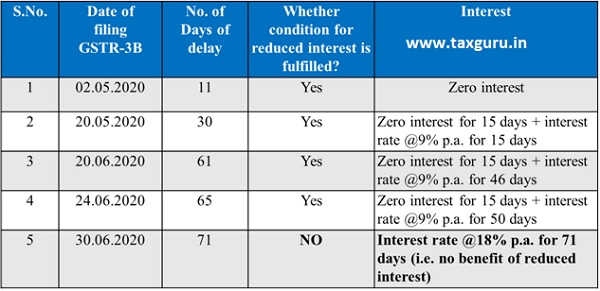

C. Conditional waiver of Interest and late fee relating to GST returns and revised due dates to file GSTR-3B for May 2020

Firstly, there is a change in the due date to file GSTR-3B only for the month of May 2020. There is no change in due date to file GSTR-1 for any month or quarter or GSTR-3B for any month except May 2020

The relief has been provided in following manner:

- By waiving the late fee if the GSTR-1 or 3B for a month or quarter is filed till certain dates

- By waiving interest if GSTR-3B is filed till a certain date

- Reduced rate of Interest @9% p.a. as against existing Interest rate of 18% p.a. if GSTR-3B is filed till a certain date

If the conditions attached to the relief are not fulfilled, then a late fee as well interest will be calculated from the due date of filing GSTR-3B or GSTR-1 for a tax period as the case may be.

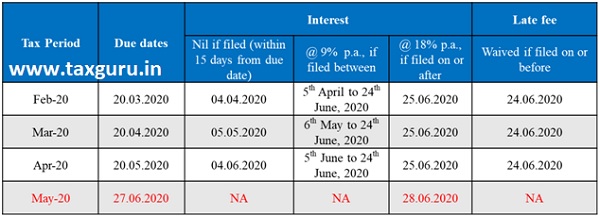

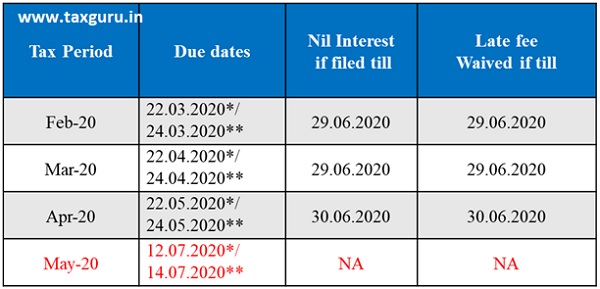

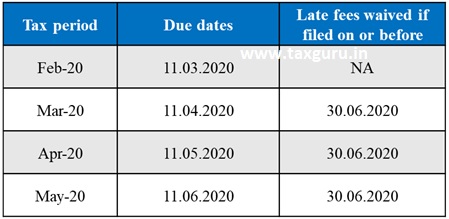

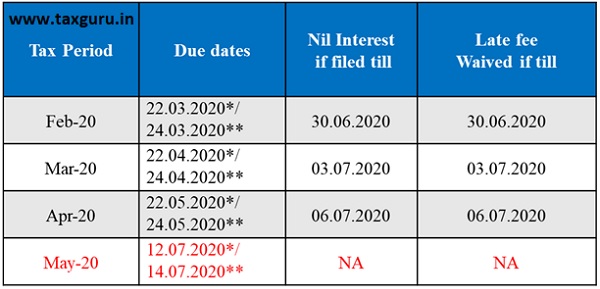

The month-wise and taxpayers wise due dates and reliefs are summarized in the table below:

(1) Aggregate turnover of more than Rs. 5 crores

GSTR-3B

GSTR-1

(2) Aggregate turnover of more than Rs. 1.5 crores but upto Rs. 5 crores

GSTR-3B

GSTR-1

(3) Aggregate turnover of upto Rs. 1.5 crores

GSTR-3B

GSTR-1

* Taxpayers with principal place of business in the States of Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana, Andhra Pradesh, the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands or Lakshadweep

** Taxpayer with principal place of business in the States of Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha, the Union territories of Jammu and Kashmir, Ladakh, Chandigarh or Delhi,

Note: The aggregate turnover would be seen for the preceding Financial Year. Since the months for which relief has been provided falls in two Financial Years, the turnover criteria would be different for months under FY 2019-20 and months under FY 2020-21.

The illustration as per CBIC CGST Circular No. 136/6/2020 dated 03.04.2020

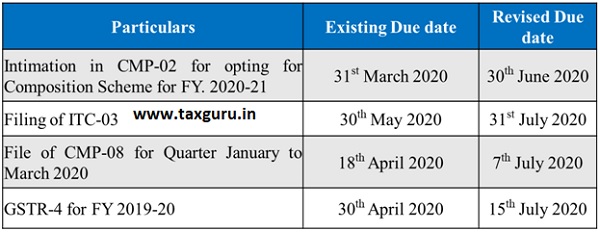

D. Extension in due date for Composition Taxpayers

The due dates have been extended for various returns and intimations in respect of Composition Tax Payers by CGST Notification No. 30 & 34/2020 dated 03.04.2020. The same is summarized as under:

Extension in various compliances and actions under GST law

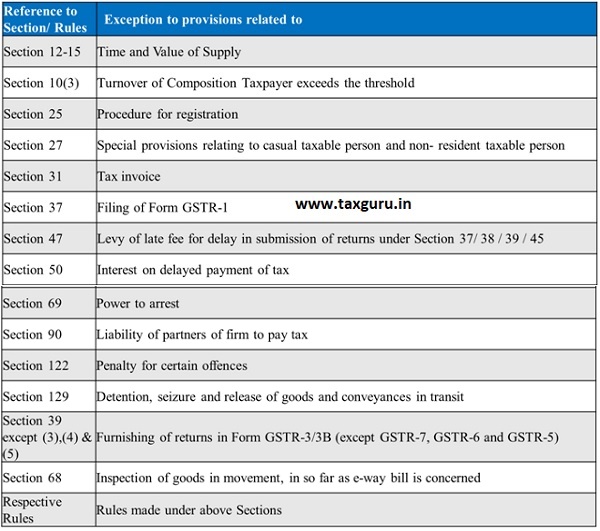

By way of the CGST Notification No. 35/2020 dated 03.04.2020, it has been notified that where any time limit for completion or compliance of any action, by any authority or by any person which falls during the period from the 20.03.2020 to 29.06.2020, then such time limit shall be extended to 30.06.2020. The Notification is divided into two parts, one, the inclusion in the above extension and second, the exclusion i.e. the activities to which the above relief will not apply. Each of the inclusion and exclusion is mentioned below:

Inclusions

- completion of any proceeding or passing of any order or issuance of any notice, intimation, notification, sanction or approval or such other action, by whatever name called, by any authority, commission or tribunal, by whatever name called, under the provisions of the Acts stated above; or (Comment: From the perspective of the Department)

- filing of any appeal, reply or application or furnishing of any report, document, return, statement or such other record, by whatever name called, under the provisions of the Acts stated above. (Comment: From the perspective of the Taxpayer)

Exclusions

Comments: Barring few exceptions like penalty under Section 122, the power to arrest, detention/seizure/inspection of the goods-in-transit, most of the timelines have been extended including response to the summons, provision release of the seized goods, reply to Show Cause Notice, filing of appeals before the appellate authority, etc.

Due dates for Returns for TDS, TCS, Non-resident taxpayers, ISDs

It is pertinent to note that there is no specific Notification extending the due dates to file other returns under GST like GSTR-5, GSTR-6, GSTR-7 & GSTR-8. However, the same is very well covered by the general CGST Notification No. 35/2020 dated 03.04.2020 extending timelines for various compliances and actions. Hence, the due dates for all the above returns for those periods whose due date fall between 20th March 2020 to 29th June 2020 have been extended till 30th June 2020.

Disclaimer: The information in this document is for educational purposes only and nothing conveyed or provided should be considered as legal, accounting or tax advice.

Author Bio