INTRODUCTION:–

The word ‘Composition’ comes from the Latin , meaning ‘Put together’.

It is a feature of Indirect tax laws that in order to provide comfort to an assessee from completing with the requirement of paying tax on value addition by maintaining details of ‘inputs’ & ‘outputs’, an option is provided to go for a ‘put together scheme’,& make a payment of an amount.

The objective of composition scheme is to bring simplicity and to reduce the compliance cost for the small taxpayers. Small taxpayers with an aggregate turnover in a preceding financial year up to 1.5 Cr. shall be eligible for composition levy. Suppliers opting for composition levy need not worry about the classification of their goods or services or both, the rate of GST applicable on the same, etc. They are not required to raise any tax invoice, but simply need to issue a Bill of Supply. At the end of a quarter, the registered person opting for composition levy would pay a certain specified percentage of his turnover of the quarter as tax, without availing the benefit of the input tax credit.

Important Definition:-

Turnover in State or Turnover in Union Territory Sec 2(112):-means the aggregate value of –

- all taxable supplies (excluding the value of inward supplies on which tax is payable by a person on reverse charge basis)and

- exempt supplies made within a state or union territory by a taxable person,

- export of goods and services or both and

- inter-state supplies of goods or services or both made from the state or union territory by the said taxable person

- but excludes central tax,state tax,Union territory tax,integrated tax& cess.

Sec 10(1):- ELIGIBILITY CRITERIA FOR COMPOSITION LEVY

Notwithstanding anything to the contrary contained in this Act but subject to the provisions of sub-sections (3) and (4) of section 9, a registered person, whose aggregate turnover in the preceding financial year did not exceed 1.5 Cr. (75 lacs for Special category State except for the state of Assam, Himachal Pradesh and Jammu & Kashmir,) may opt to pay, in lieu of the tax payable by him u/s 9(1), an amount calculated at such rate as may be prescribed, but not exceeding,–

(a) Half Per cent of the turnover in State or turnover in Union territory in case of a manufacturer,

(b) two and a half per cent of the turnover in State or turnover in Union territory in case of persons engaged in making supplies referred to in clause (b) of paragraph 6 of Schedule II, and

(c) half per cent of the turnover of taxable supply of goods (An services as per rule 7 below) in State or turnover in Union territory in case of other suppliers.

Provided that the Government may, by notification, increase the said limit of fifty lakh rupees to such higher amount, not exceeding one crore & fifty lakh rupees, as may be recommended by the Council.

Provided further that a person who opts to pay tax under clause (a) or clause (b) or clause (c) may supply services (other than those referred to in clause (b) of paragraph 6 of Schedule II), of value not exceeding 10% of turnover in a State or Union territory in the preceding financial year or 5 lakh rupees, whichever is higher.

Actual Rate of Tax under Composition Scheme notified in Rule 7 of CGST Rules, 2017

(Amended by N/n 1/2018 C.T.)

| Sr.No. | Categories of Registered Person | Central Rate | State/Ut GST Rate | Total Rate | Basis of Calculation |

| 1. | Manufacturers other than manufacturers of such goods as may be notified by the government. | 0.50% | 0.50% | 1.00% | Turnover in State |

| 2. | Suppliers making supplies referred to in clause (b) of para 6 of Schedule II

Example – Restaurant, Catering, Mess or any other service contract where goods as food or drink are supplied for human consumption. |

2.50% | 2.50% | 5.00% | Turnover in State |

| 3. | Other Supplies | 0.50% | 0.50% | 1.00% | Turnover of taxable supplies of goods & Services in state. |

Sec 10(2)- CONDITIONS FOR COMPOSITION SCHEME:-

(a)Save as provided in subsection(1), he is not engaged in the supply of services.

Comment: As we have seen in the proviso to sec 10(1), that a person who opts to pay tax under clause (a) or clause(b) or clause (c) may supply services (other than those referred to in clause (b) of paragraph 6 of Schedule II), of value not exceeding 10% of turnover in a State or Union territory in the preceding financial year or 5 lakh rupees, whichever is higher.

Example: Finolex Ltd (MH branch), sells electrical cables, motos and wire & also undertakes repair of switches, motor sets the turnover from such services during the 1st quarter of current FY 2019-20 was 2 Lacs. The Aggregate Turnover during the preceding financial year from the sale of goods was 70 lakhs, including repairing whereas Turnover in State for the preceding financial year was 40 lakhs. Whether Finolex Ltd. is eligible for composition scheme.

Answer: Yes. As per proviso to sec 10(1) inserted via CGST amendment act 2018, Finolex Ltd., can make a supply of services up to 10% of turnover in the state in previous FY i.e. 4 lakhs or 5 lakhs whichever is higher. Therefore, the benefit of composition scheme will be available to Finolex Ltd. as the turnover from services has not exceeded the limit of 5 lakhs as computed above. Also the aggregate turnover in the previous fin.yr. is below 1.5 Cr. thus eligible for composition scheme.

(b)He is not engaged in making any supply of goods which are leviable to tax under this Act;

Example: Mr Jay is a dealer who is selling taxable goods, exempted goods and non-taxable goods (i.e.Liquor). His turnover in the preceding financial year is 35 lakh,10 lakh,15lakh goods which are leviable to GST exempted and non-taxable respectively. Whether Mr Jay is eligible for the Composition Scheme?

Answer: If a person is selling the goods, which are not leviable to tax under GST, then he is not eligible to opt for composition scheme.

(c)He is not engaged in making any inter-state outward supplies of goods;

(d)He is not engaged in making any supply of goods through an electronic commerce operator who is required to collect tax at source under Sec52; and

(e) He is not a manufacturer of such goods as may be notified by the Government on the recommendations of the Council

| Tariff item, subheading, heading or Chapter | Description |

| 2105 00 00 | Ice cream and other edible ice, whether or not containing cocoa |

| 2106 90 20 | Pan Masala |

| 2202 10 10 | Aerated Water |

| 24 | All goods, i.e. Tobacco and manufactured tobacco substitutes |

Proviso to Sec 10(2): SCHEMES APPLIES TO ALL REGISTERED PERSONS WITH THE SAME PAN.

Provided that where more than one registered persons are having the same Permanent Account Number (issued under the Income-tax Act, 1961), the registered person shall not be eligible to opt for the scheme under sub-section (1) unless all such registered persons opt to pay tax under that sub-section.

Sec10(3):- ELIGIBILITY CRITERIA FOR COMPOSITION SCHEME

The option availed of a registered person under subsection(1) shall lapse with effect from the day on which his aggregate turnover during the financial year exceeds the limit specified under sub-section (1).(i.e. 1.5 Cr.)

RULE 5: CONDITIONS AND RESTRICTIONS FOR COMPOSITION LEVY

The person opting to pay tax under Sec10(i.e. Composition Scheme) has complied with the following conditions:-

1. He is not a Casual Taxable Person or Non-Resident Taxable Person.

2. The stock held on the appointment date should not have been purchased in the course of inter-state trade, imported or received from the branch and should not have been purchased from unregistered supplier provided the tax should have been paid under sec9(4).

3. He should pay tax under sec9(3) & 9(4) on inward supplies of goods or services or both.

4. He should mention on top of every bill that “composition taxable person, not eligible to collect tax on supplies”.

5. He should mention at all places, every notice, signboards displayed at a prominent place at his principal place and all additional places of business that he is a Composition Taxable Person.

RULE 3&4: INTIMATION OF OPTING FOR COMPOSITION LEVY

1.Intimation by the person applying for registration: Any person who is not registered and applies for registration may give an option to pay tax under composition levy in Part B of the registration form, viz., FORM GST REG-01.

The same shall be considered as an intimation to pay tax under Composition Levy. Such intimation shall be considered only after the grant of registration to the applicant and his option to pay tax under composition levy shall be effective from the date from which registration is effective.

2.Intimation by a Registered Person: A registered person who opts to pay tax under composition levy scheme shall electronically file an intimation in the prescribed form (CMP-02) on the Common Portal [www.gst.gov.in], prior to the commencement of the FY for which said option is exercised.

He shall also furnish the statement Form GST ITC-3 for details of ITC relating to inputs lying in stock, inputs contained in semi-finished or finished goods within 90 days of commencement of the relevant financial year in accordance with the provisions of rule 44(4) of CGST Rules, 2017.

Any intimation in respect of any place of business in a State/UT shall be deemed to be an intimation in respect of all other places of business registered on the same PAN.

The option to pay tax under composition levy shall be effective from the beginning of the FY.

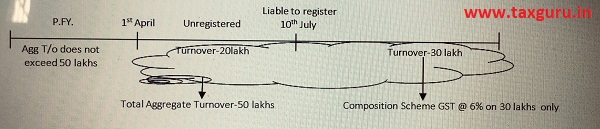

COMPOSITION SCHEME FOR SERVICES: EFFECTIVE FROM 1ST APRIL, 2019 (NOTIFICATION NO.- 2/2019-CT(R) dt 7/3/2019)

Eligibility Criteria:-

- Supplies are made by the registered person whose aggregate turnover in Preceding financial year was 50Lakh or below.

2)Supply is not eligible to pay tax u/s 10(1) of CGST Act.

Composite Tax rate & Levy in the current year : –

GST rate 6% (i.e. CGST 3% & SGST 3%) on the first supply of goods or services or both up to an aggregate turnover of 50 lakh made on or after the first day of April in any financial year, by the registered person.

Explanation – “first supplies of goods or services or both” shall include the supplies from the first day of April of a financial year to the date from which he becomes liable for registration under the said Act but for the purpose of determination of tax payable under this notification shall not include the supplies from the first day of April of a financial year to the date from which he becomes liable for registration under the Act.

IMPORTANT NOTE:-

The first supply of goods and services include:-

1.Taxable supply of Goods and Services

2.Exempt Supply of Goods and Services

3.NIL Rate Supply of Goods and Services

OTHER CONDITION FOR AVAILING COMPOSITION SCHEME(FOR SERVICES):-

a) The supplier should not be engaged in the business of making any supplies on which GST is not leviable under this Act (i.e., petro products or alcoholic liquor).

b) The supplier should not be making any interstate supplies.

c) The supplier should not be a casual taxable person, non-resident taxable person and

d) The supplier should not making any supply through an e-commerce operator (ECO) on which TCS applies.

e) Shall not collect any tax from the recipient on supplies made by him nor shall he be entitled to any credit of input tax.

f) Shall be liable to pay central tax on inward supplies on which he is liable to pay tax under Section 9(3) or 9(4) of CGST Act at the applicable rates.

g) Shall issue, instead of tax invoice, a bill of supply as referred to in section 31(3)(c) of the CGST Act with particulars as prescribed in rule 49 of CGST Rules. The registered person shall mention the following words at the top of the bill of supply, namely: – ‘taxable person paying tax in terms of notification No. 2/2019-Central Tax (Rate) dated 07.03.2019, not eligible to collect tax on supplies’.

h) The supplier should not be engaged in the business of ice cream, Pan Masala, Aerated Water, Tobacco and tobacco substitutes.

CONCLUSION:-

Even though the CGST Act states the composition levy is an easy method for the purpose of assessment by the assessee under the CGST Act because there is no need to maintain elaborate books of accounts and simple filing of the quarterly return, from reading of the abovesaid facts it may not be seen that even composition scheme is also a complex one.

The composition scheme may be beneficial for a small trader whose aggregate turnover may be less than 1.5crore in case of goods and 50 lakhs in case of services. But in the present trade world, it cannot be an effective remedy for the majority of taxpayers.

Author Bio

Nicely explained the concepts 👍