1. E- Way Bill (EWB) generation blocking means not allowing the taxpayer to generate an E-Way bill if he has not filed GST Return for the latest two successive months or quarters.

2. STATUTORY PROVISION

Rule 138E – No person (including a consignor, consignee, transporter, an e-commerce operator, or a courier agency) shall be allowed to furnish the information in PART A of FORM GST EWB 01 in respect of a registered person, whether as a supplier or a recipient, who:-

(a) Being a person paying tax under composition scheme has not furnished the statement in FORM GST CMP-08 for two consecutive quarters

(b) Being a person other than a person specified in clause (a) has not furnished the returns for a consecutive period of two months.

3. The anti-evasion measure was originally scheduled to come into force in June 2019. CBIC vide Notification 22/2019-Central Tax, DT. 23-04-2019 notified that Non-filers of GST returns would not be able to generate e-way bills from the 21st day of June 2019. However, this has been repeatedly set aside due to various reasons

3.1 The rule has been modified w.e.f. 15 Oct 2020 to apply only to taxpayers above Rs 5 crore turnover thresholds.

4. The Central Board of Indirect Taxes and Customs (CBIC ) has clarified that the E-Way Bill generation facility to be blocked for all taxpayers irrespective of their aggregate annual turnover who failed to file GSTR-3B for 2 or more tax period from December 1st, 2020.

4.1 The EWB generation facility of a taxpayer is liable to be restricted, in case the taxpayer fails to file their FORM GSTR-3B returns or Statement in FORM GST CMP-08, for tax periods of two or more.

4.2 Thus on 1st December 2020, the system blocked EWB generation in the following cases:-

(a) Non-filing of two or more returns in GSTR 3B for months till Oct 2020

(b) Non-filing of two or more CMP 08 statements up to Jul 20-Sep 20 quarters.

5. The taxpayers can come across the following situations in case E-Way is blocked:

(a) A pop-up notification will appear every single time the block taxpayer tries to generate a new EWB for a bulk generation:

(b) If any taxpayer/transporter enters the blocked GSTIN as another party while e-waybill generation, a similar message will appear.

6. UNBLOCKING OF E- WAY BILL: Unblocking means allowing the generation of E-Way bills for the GSTIN.

6.1 E-Way Bill generation facility would be automatically unblocked on the EWB Portal when the taxpayer files GST Return and the default in Return filing reduces to less than two tax periods.

6.2 UNBLOCKING WHEN TAXPAYER FILES THE RETURNS In case, the blocked taxpayer has filed the Return on the GST Common Portal, the next day morning his GSTIN is unblocked on the E-way Bill system and allows him to generate the E-way bills.

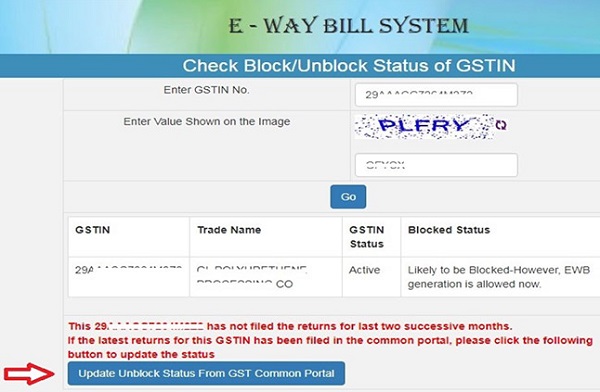

6.3 If the taxpayer wants to generate the e-way bills immediately after filing the Return, then he can go to the e-way bill portal and select the option ‘Search enter his GSTIN and see the status.

6.4 If it is blocked then he can use the update option to get the latest filing status from the GST Common Portal and get unblocked.

6.5 Still if the system is not unblocking the GSTIN for e-way bill generation, then he can contact the Help Desk of the GST and raise the complaint to get his case resolved.

7. ONLINE REQUEST FOR UNBLOCKING: The taxpayer may also file an online request for unblocking of the E-Way Bill generation facility with his jurisdictional tax officer. The taxpayers were to apply manually earlier. Now, w.e.f. 28th Nov 2020, an online facility has been provided.

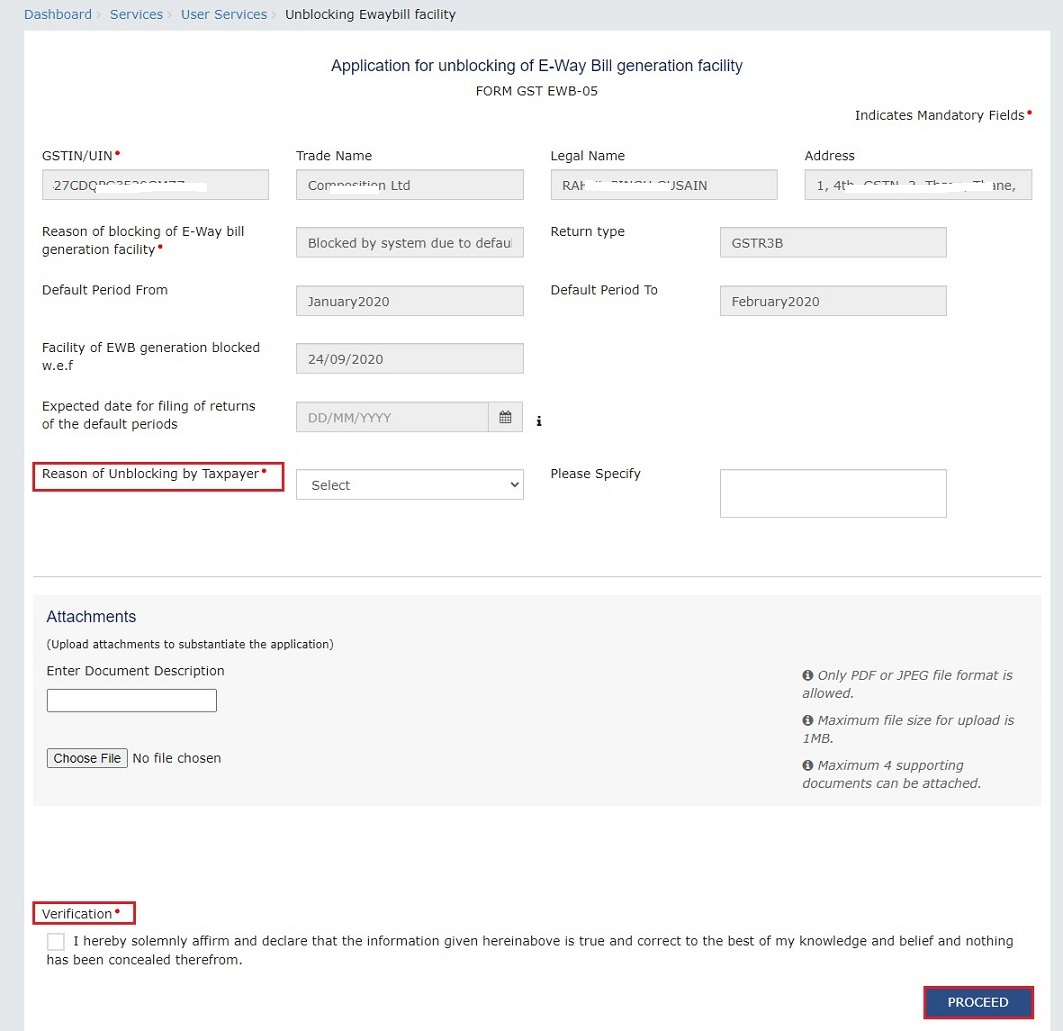

7.1 The taxpayer can file an online application for unblocking of EWB generation in Form GST EWB 05 with sufficient cause for the reason and request to unlock.

8. STATUTORY PROVISION

| 1st Proviso to Rule 138E | The Commissioner may, on receipt of an application from a registered person in FORM GST EWB 05 on sufficient cause being shown and for reasons to be recorded in writing, by order, in FORM GST EWB 06 allow furnishing of the said information in PART A of FORM GST EWB 01, subject to such conditions and restrictions as may be specified by him. |

9. STEPS FOR ONLINE UNBLOCKING: To file an online application for unblocking EWB generation facility on GST Portal, a taxpayer need to take the following steps:

(a) Login to the portal and navigate to Services> User services> My Applications

(b) Select application type as “Application for unblocking of E-way bill” and click New Application.

(c) The Application for unblocking of E-way bill page is displayed:-

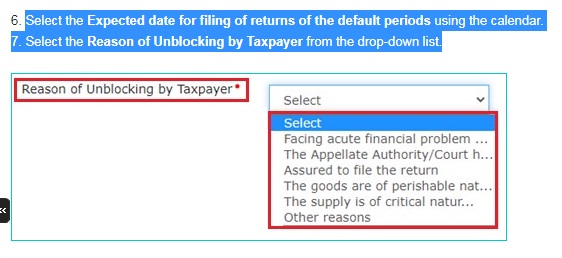

(d) Select the Expected date for filing of returns of the default periods using the calendar.

(e) Select the Reason of Unblocking by Taxpayer from the drop-down list.

(f) The application so filed is populated to the dashboard of the jurisdictional tax official. The tax official can issue a Notice for a personal hearing to the taxpayer. Then the taxpayer can file their reply to the notice online, along with supporting documents.(g) After the proceedings, the Tax Officer can issue an order (in Form EWB-06) approving the taxpayer application for unblocking the EWB generation facility. After which their EWB generation facility will be restored for the duration specified in the order.

(h) If the Tax Officer rejects the taxpayer’s application vide order in Form EWB-06, the EWB generation facility will remain blocked and the taxpayer shall be required to file their pending returns (in Form GSTR-3B / Statement in FORM CMP-08, to reduce the pendency to less than two tax periods), for the restoration of the EWB generation facility.

(i) Notice(s)/ Order issued by Tax Officer will be sent via SMS and mail to the taxpayer and will be made available on the taxpayer dashboard (Services > User Services > View Additional Notices/Orders option).

10. OTHER RELEVANT POINTS

10.1 There will not be any effect or impact on the already generated e-way bills of the blocked GSTINs. These e-way bills are valid and can be moved to the destination without any problem.

10.2 The transporters, taxpayers of blocked GSTINs, can update the vehicle and transporter details and carry out the extension, if required, as per the rule.

____________

The author can be approached at caanitabhadra@gmail.com

Author Bio