Ankur Jain

Audit – Highest Level of Assurance

An audit provides the highest level of assurance. An audit is a methodical review and objective examination of the financial statements, including the verification of specific information as determined by the auditor or as established by general practice.

Our work includes a review of internal controls, testing of selected transactions, and communication with third parties. Based on our findings, we issue a report on whether the financial statements are fairly stated and free of material misstatements.

An Audit allows you to….

- Satisfy stakeholders such as employees, customers, suppliers and especially pressure groups, as well as the investing community, as to the credibility of published information.

- Facilitate the payment of corporate tax, goods and services tax, and other taxes on-time and accurately, thereby avoiding interest, penalties, and investigations.

- Comply with banking covenants.

- Help deter and detect material fraud and error.

- Facilitate the purchase and sale of businesses.

Executive Summary for Audit Efficiency

- Some professional firms have discovered that by working smarter they can maintain and even improve quality while enhancing profits by cutting back on the hours they invest in audit engagements. A new survey spotlights some of these best practices at firms known for their efficient and effective controls.

- To be honest with you, the very first step to achieve audit efficiency is to manage and train clients. Some of the professional firms work best when client provide then with the data.

- Many firms have different strategies for educating their clients about their needs (Audit checklist) but most such strategies pay off.

- Retaining clients and staff also can increase audit efficiency. Firms found that greater familiarities with a practice area and a client enabled them to streamline their approaches and make the most of the time spent on each engagement.

- Planning properly is critical to audit efficiency. Some of the firms in fact many firms review the prior year’s working papers to familiarize themselves with client issues and to seek out past inefficiencies and possible improvements.

- Correlating Audit staff efforts to the level of risk and materiality helped increase efficiency. Firms should try to limit procedures in low risk areas and focus their attention on trouble spots.

When it comes to audit efficiency, sometimes less is more. Many professional firms have found it’s possible to slash the amount of time involved while still meeting professional standards. They have discovered that by working smarter, they can maintain—and even improve—quality even while cutting back on the hours invested in audit engagements and enhancing profit.

BEST PRACTICES

The study revealed that there were four important steps to achieving audit efficiency.

1. Manage and train the client. Professionals (CAs) can work much more efficiently when clients supply them with all the data they need. If a firm’s staff has to spend time doing catch-up book keeping work or locating and copying needed files, the length of the audit probably will increase and the firm is much less likely to realize 100% of the value of its fees.

“Too often we get in there and the client has things that aren’t reconciled or account analysis that isn’t done. We end up rolling all our extra work into the audit and not getting paid for it.”

To prevent this problem, firm has experimented with creating two separate groups: a traditional audit team and another, “swat” team that prepares clients for the audit. Introducing the swat team and a different engagement letter for its work “forces a conversation up front with the higher level people where we say, ‘Here’s what’s not ready, here’s what needs to happen, here’s how we can help and this is what it will cost.’”

At Weaver & Tidwell in Dallas, partner Gary Hoffman reviews the possible engagement efficiencies with clients at the planning conference. “We look at what added or saved time or money during the previous year’s engagement so we can reinforce the right client behaviour. The clients see how they can provide us with better assistance and the financial impact that will have on engagement time.”

The survey revealed other strategies for ensuring clients are prepared for their audits:

- Starting at the top. Practitioners meet with boards of directors and ask them to communicate audit value to organization staff members and urge them to cooperate in engagement preparation.

- Making it as easy as possible. Firms provide explicit lists of what is needed with clear examples and due dates.

- Charging for preparation work the auditors must do and mentioning the extra charge in the engagement letter.

- Discounting the fee when proper preparation is performed. Firms found a small inducement can cost less than taking on preparation work themselves.

- Rescheduling fieldwork if the client is not ready.

- Developing realistic expectations. Firms know clients won’t complete all the preparation work needed at first, but once they start with basic expectations, they can add more responsibilities each year.

2. Retain clients and staff.Firms agreed that a meaningful investment in an industry niche was an important contributor to efficiency. When a firm retains clients, it means that greater familiarity with the practice area and with particular clients enables practitioners to streamline their audit approaches and to make the most of the time they spend on each engagement. It also allowed them to offer clients valuable advice on best industry practices and to charge premium fees.

Lambert always looks ahead. At the end of an audit, “when you deliver the report, also deliver your next year’s engagement letter,” she advises. “It’s not at all unusual for the client to sign it and hand it right back. It’s a great way to keep the relationship going.”

Survey participants said staff retention was very important because it enhanced both their client-specific and industry experience. Firm strategies for achieving low employee turnover included

- Explicit and enforced anti overtime policies.

- A growth plan that offers opportunities for recognition and advancement to partner level.

- Flexible hours and casual dress policies.

- Competitive compensation and benefits.

- Keeping the work interesting, which can involve granting responsibility and including staff in the planning process.

Who Participated

The study included partners and senior managers at 14 firms located in California, Colorado, the District of Columbia, Indiana, Maryland, Nevada, Ohio, Virginia and Washington. They were selected on the basis of recommendations from state CPA society peer review directors and peer review team captains. The firms had consistent unmodified peer review reports, a significant portion of their practices devoted to NPOs and the overall appearance of successful firms. Firms averaged 43 people; 8 firms had fewer than 20 people while 6 had between 55 and 122.

The study included partners and senior managers at 14 firms located in California, Colorado, the District of Columbia, Indiana, Maryland, Nevada, Ohio, Virginia and Washington. They were selected on the basis of recommendations from state CPA society peer review directors and peer review team captains. The firms had consistent unmodified peer review reports, a significant portion of their practices devoted to NPOs and the overall appearance of successful firms. Firms averaged 43 people; 8 firms had fewer than 20 people while 6 had between 55 and 122.

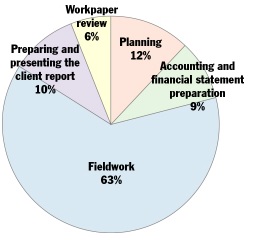

NPO audit breakdown. Firms averaged 125 hours per NPO audit, with the breakdown shown at right.

The percentage of time spent in planning varied from 2% to 25%. For a new client, firms averaged 14 extra hours per audit, spent mainly in planning but also some in the field and some in generating the final report.

3. Plan properly. The time survey participants spent on this part of the audit process varied greatly from firm to firm, with a range of 2% to 25%.

Planning is critical to audit efficiency, many practitioners believe. “Back in the mid- to late 1980s, we changed our audit approach,” says Tony Lynn of Davis, Lynn & Moots, in Springfield, Missouri. In the past “our philosophy was to go in, audit as much as we could and when our bags were full, come home. As a staff person, I didn’t understand why we did some procedures except that they were in the workpapers from the year before.”

Today, on any audit, Lynn’s firm spends time getting to know a client and its systems in advance. “We can understand its entire operation, as opposed to understanding a bunch of procedures that we’d done previously.” Since changing the firm’s approach, “we’ve been able to reduce hours on the engagement. We’re not just in there doing procedures; we’re doing an audit.”

As part of the planning process, the firms surveyed reviewed the prior year’s workpapers to familiarize themselves with client issues and to seek out possible past inefficiencies in their own work and possible improvements.

Other steps included

- Meeting with clients to discuss the process and identify client responsibilities.

- Downloading the client’s trial balance to the firm’s software.

- Sending confirmations.

- Preparing lead schedules.

- Reviewing planning decisions with the firm’s audit staff and considering the staff suggestions for improvement that were turned in at the end of the last year’s work.

However, not all successful firms have lengthy efficiency planning processes, the survey found. Some simply reviewed last year’s audit and considered what the firm could have done differently. Some created a final plan after the audit had begun, when current issues and problems were clear. These approaches generally applied in smaller firms with a high percentage of experienced staff.

4. Assess risk. Correlating audit efforts to the levels of risk and materiality has inherently a more efficient approach, the survey found.

“If you assess risk, it should affect your procedures,” says Lambert. Firms should strive actively to cut out procedures in the low-risk areas and focus instead on the problem spots.

When considering risk, Lambert recommends bringing the whole audit team together. “The senior people can talk about industry risks, while the middle-level people tend to know more about control issues and the competency of the client. The youngest people may not understand it all, but they can learn a lot. By putting the whole engagement team together, we help all of them understand the different types of risk.”

Analytical procedures (reasonable and predictive tests) were considered the most efficient by those surveyed. One firm’s audit team begins each step of the process by asking, Can we audit this analytically? Every participant is trying to use more analytical procedures and do less transaction testing because it

- Saves time.

- Uncovers what isn’t there instead of focusing on what is.

- Is more interesting to perform, leading to a deeper understanding of the client’s business.

- Areas in which predictive and reasonableness tests have replaced transaction testing and saved time include

- Rent payable or paid and rent receivable or received.

- Interest income.

- Payroll and payroll taxes.

- Revenue from direct mail fundraising.

- Postage expenses in direct mail fundraising.

- Prepaid expenses (rent, insurance).

- Professional fees.

- Revenue from annual meeting.

TIME EFFICIENCIES

Besides practice management and technical suggestions, firms also had a number of quick tips for enhancing efficiency. One step considered key to an efficient audit, saving as much as 20% to 30% of total time, was completing the audit in the field, including

- Reviewing work-papers.

- Clearing up points that arose while doing the review of the work-papers.

- Producing the draft report and management letter.

“People are less distracted when they finish the work in the field”

Other known tips are

- Use technology. Cut down on hard copy and use laptops and even portable printers to facilitate efficiency in the field.

- Include memos in the work-papers. These can stipulate test objectives; document steps performed and describe what was found.

- Organize work-papers along narrative lines. Arrange them so they describe what was done, why and the results.

- Keep it short. Restrict work-paper files to less than possible.

- Keep a summary of information received from the client rather than store all the data in the file for next year’s team to wade through.

- Conduct firm wide meetings on how to streamline work-papers.

- Keep in touch. Have the audit partner or managers available to staff in the field to reduce cycle time and total audit time; staff then can get quick answers and implement changes to the audit program.

- Be consistent. Standardize the format and flow of work-papers so they are easy to understand and all data contained in them are readily referenced.

OPTIONS FOR EVERY FIRM

The good news is there was not any one particular route to audit efficiency. Whether the firm was traditional or casual, it was still possible to identify efficiencies that improved profitability.

When any firm performs peer reviews, often “we see people who are over auditing and not understanding why. I usually ask, ‘What does this work paper give you?’ They often say, ‘I don’t know; we’ve just always done it that way.’ But if you can’t say why you’re doing something, you should get rid of it.”

(Author can be reached at ankurjainca2007@gmail.com)

Author Bio