WHAT IS VAR?

Value at Risk is basically a statistical tool to measure the expected loss at a particular time period from particular Stock or Whole Portfolio with given Confidence Level (Probability Level).

Say for Example, Mr. A wants to invest 2,00,000 in Stock of ABC Co. for 1 day S.D. of Stock is Say 5%. Mr. A wants to know the expected loss he can incur with 99% confidence level.

REQUIREMENTS FOR CALCULATION OF VAR?

1. Standard Deviation of Stock (Standard Deviation means a movement of Stock on-an-average at particular time frame)

2. Confidence level (We have to decide, at what confidence level we want to calculate expected loss)

3. Time Period (Time Period for which we want to invest in particular Stock.

4. Amount of Investment

5. Normal Distribution Table (To calculate Z Value)

FORMULA FOR VAR

VAR= S.D IN VALUE * Z VALUE

Where

S.D. in Value = Investment Amount*S.D of Stock

Z Value= No of S.D. from Mean (This we have see from Normal Distribution Table)

Continuing our Example,

Lets Calculate Expected Loss for Mr. A

VAR= S.D IN VALUE * Z VALUE

S.D. in Value= 2,00,000*5%= 10,000

VAR= 10000*Z Value

______________________________________

———–45%———— ————50%—————–

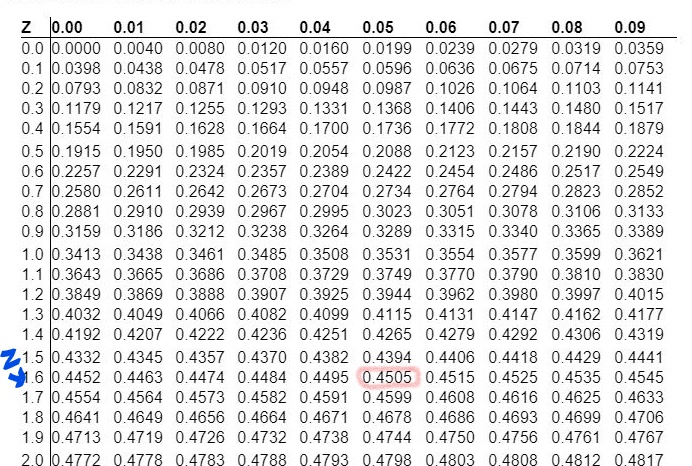

We have to see now Z Value for 45% in Normal Distribution Table,

We Got Z Value for 45% is 1.6

Note= For 100% Accuracy interpolation between 0.4505 and 0.4495 can be done.

VAR= 10,000 (S.D. in Value) * 1.6 (Z Value)

=16000.

Interpretation:

Mr. A can invest Rs. 2,00,000 for 1 Day with expected loss of 16,000 with 95% Confidence Level.

In other words, It is 95% probability that loss of Mr. A will not be exceeding 16,000 and 5% probability of incurring loss of more than 16,000 respectively.

Author Bio

Explained in simple language..Thanks