Karan Khatri

What is Accounting Fraud?

What is Accounting Fraud?

Accounting fraud is intentional manipulation of financial statements to create a window dressing of a company’s financial health. It involves an employee, account or the organization itself and is misleading to investors and shareholders. A company canfalsify its financial statements by overstating its revenue or assets, not recording expenses and under-recording liabilities.

For example, a company commits accounting fraud if it overstates its revenue. Suppose company ABC is actually operating at a loss and is not generating any revenues. On its financial statements, the company’s profits would be inflated and its net worth would be overstated. If the company overstates its revenues, it would drive its share price up and falsely depict the its true financial health.

Another example of a company committing accounting fraud is when it overstates its assets and under-records its liabilities. For example, suppose a company overstates its current assets and understates its current liabilities. This falsifies a company’s short-term liquidity. Suppose a company has current assets of Rs 1 Crore, and its current liabilities are Rs 5 Crore.

If the company overstates its current assets and understates its current liabilities, this will falsify the liquidity of the company. If the company states it has Rs 5 Crore in current assets and Rs 5,00,000 in current liabilities, potential investors will believe that the company has enough liquid assets to cover all of its liabilities.

A third example is if a company does not record its expenses. As a result, the company’s net income is overstated and expenses are understated on its income statement. This type of accounting fraud creates a window dressing of how much net income a company is receiving while, in reality, it may be losing money.

Why would someone do a Fraud?

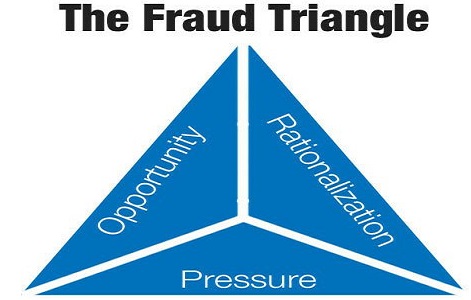

The easy answer is that they do it out of greed, but there’s more to the crime than just that. People need certain motivations to be driven to steal from their company. The Fraud Triangle presents three factors that can make one consider fraud:

- Pressure

- Rationalization

- Opportunity

Once those elements fall into place, the idea of fraud becomes more of a possibility. While the end goal may be the same, all three parts of The Fraud Triangle start off with different ideas.

- Pressure to Commit Fraud

The motivation behind the crime and can be either personal financial pressure, such as debt problems, or workplace debt problems, such as a shortfall in revenue. The pressure is seen by the individual as unsolvable by orthodox, legal, sanctioned routes and unshareable with others who may be able to offer assistance. A common example of a perceived unshareable financial problem is gambling debt. Maintenance of a lifestyle is another common example. Pressure can also be caused by other people. A spouse, relative, or friend might push a person down the fraudulent path. Even another employee looking to commit fraud may pressure another if that coworker would be needed to complete the crime. Pressure can force a variety of human responses, and sometimes that can lead to internal fraud.

- Opportunity to Commit Fraud

This is the biggest factor in The Fraud Triangle. Even if a person is under pressure to commit fraud or has rationalized the idea to the point of no return, it’s impossible to commit fraud without having an opportunity to do so. In this stage the worker sees a clear course of action by which they can abuse their position to solve the perceived unshareable financial problem in a way that – again, perceived by them – is unlikely to be discovered. In many cases the ability to solve the problem in secret is key to the perception of a viable opportunity.

- The Ability to Rationalise the Crime

Rationalization can come in multiple forms. Sometimes it’s a justification. It requires the fraudster to be able to justify the crime in a way that is acceptable to his or her internal moral compass. Most fraudsters are first-time criminals and do not see themselves as criminals, but rather a victim of circumstance. Rationalisations are often based on external factors, such as a need to take care of a family, or a dishonest employer which is seen to minimise or mitigate the harm done by the crime.

Some Worst Accounting Frauds of All Time

- Waste Management Scandal (1998) – Reported $1.7 Billion in fake earnings

- Enron Scandal (2001) – Huge Debts were off the balance sheet. Shareholders lost $74 billion, thousands of employees and investors lost their retirement accounts and many employees lost their jobs

- Worldcom Scandal (2002) – Inflated assets by as much as $11 billion, leading to 30,000 lost jobs and $ 180 billion in losses for investors

- Tyco Scandal (2002) – CEO & CFO stole $150 million and inflated company income by $500 million

- Healthsouth Scandal (2003) – Earnings numbers were allegedly inflated $1.4 billion to meet stockholder expectations

- Freddie Mac Scandal (2003) – $5 billion earnings were misstated

- American Insurance Group Scandal (2005) – Massive accounting fraud to the tune of $ 3.9 billion was alleged, along with bid-rigging and stock price manipulation

- Lehman Brothers Scandal (2008) – Hid over $50 billion in loans disguised as sales

- Bernie Madoff Scandal (2008) – Tricked investors out of $64.8 billion through the largest Poniz scheme ever

- Satyam Scandal (2009) – Falsely Boosted revenue by $ 1.5 billion

(Author can be reached at cakagyaan@gmail.com)

Sir.. a pvt co. Invites shares at a premium.. and invest the share premium proceeds in another related company shares that too at premium.. since company did spend share premium money in violation of companies act 1956.. can incometax officer is at liberty to treat the share premium money received as casual and non recurring receipt and taxed it accordingly.. plz reply