A. Preface

1. Our Finance Minister, Shrimati Nirmala Sitharaman, in her budget speech mentioned that more than Rs. 3.75 lakh croreis blocked in pending litigations from the Pre-GST Regime i.e., in Service Tax And Excise. In view of such huge funds being blocked, she proposed a “Legacy Dispute Resolution Scheme” (The Scheme) that would allow a quick disclosure of these litigations.

2. Such scheme shall become available as and when notified by the government in the Official Gazette.

3. The said scheme shall give relief from paymentof tax dues to the extent of 40% to 70% depending on the amount of tax dues involved.

4. The said scheme shall give relief from payment of interest and penalty

B. Who is eligible Declarant:

In terms of Clause 124 of said scheme, any person can file the declaration covering the amount payable by him except ineligible declarants.

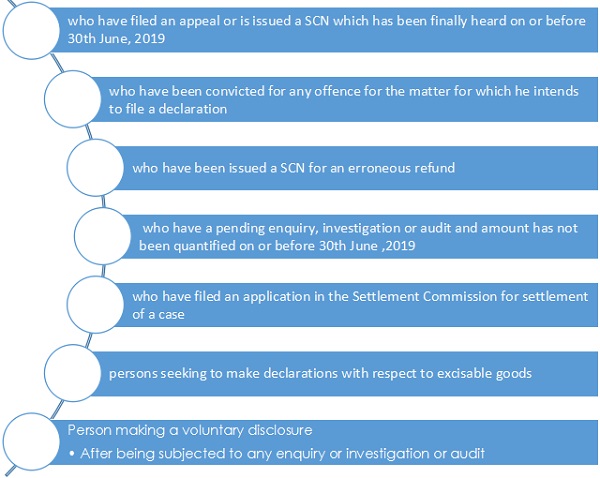

C. Who are In–eligible declarants?

The scheme is available to all persons except few persons as listed down in Clause 124 (1), as follows

Relief available under the Scheme

The relief available under the scheme shall be calculated as follows:

| Sr. No. | Particulars | Where tax payable is less than Rs.50 Lacs payable is more than Rs.50 Lacs | Where tax payable is more than Rs.50 Lacs |

| Payable | Payable | ||

| 1 | Tax dues at SCN stage | 30% | 50% |

| 2 | Tax dues at appeal stage [appeal being pending disposal as on 30th June 2019] | 30% | 50% |

| 3 | Tax dues at outstanding OIO/ OIA stage where appeal is not filed | 40% | 60% |

| 4 | Tax dues – in arrears or otherwise | 40% | 60% |

| 5 | Tax dues which have been declared in returns but not paid by the assesse | 40% | 60% |

| 6 | Tax dues which are linked to enquiry, investigation or audit – amount being quantified before 30th June 2019 | 30% | 50% |

| 7 | Tax dues at SCN stage with respect to penalties, late fees – where the amount of duty is Nil or has been paid | 0% | 0% |

| 8 | Voluntary Disclosure | 100% | 100% |

E. Procedureof making declaration

The person who wish to file declaration under this scheme shall follow the below mentioned step:

1. Eligible person shall file declaration in terms of clause 124(4) electronically.

2. The Designated committee shall verify the correctness of said declaration

3. If declared dues are accepted by DC then “Statement of amount payable” shall be issued electronically within 60 days from the date of such declaration.

4. However of declared dues is found to less than amount payable then DC shall issue “Estimate of amount payable” in electronic form with 30 days from such declaration. In this case declarant shall be granted personal hearing if he desires. After personal hearing a statement indicating the amount payable by declarant shall be issued within 60 days from date of receipt of application.

5. The declarant has to pay amount within 30 daysfrom date of above statement as mentioned in para 3 or 5 as the case may be.

F. Withdrawalof Appeal and Discharge Certificate:

1. Before Appellate forum other than High court and Supreme court:

Where the appeal, reference or reply to show cause notice was pending at appellate forum other than Supreme Court or High Court, then notwithstanding any other provisions under the erstwhile law, such appeal or reference or reply shall be deemed to be withdrawn.

2. Before High Court or Supreme Court:

Where the writ petition, appeal or reference was pending at Supreme Court or High Court, then the declarant shall have to file an application before the Court for withdrawing of such writ petition, appeal or reference with the leave of court and would have to submit the proof of withdrawal to DC in prescribed manner along with the proof payment of duty

3. Discharge Certificate:

After payment of the amount indicated in statement issued by DC and upon submitting the proof of withdrawal of appeal/ reference/ writ petition, the DC shall issue a discharge certificate within 30 days of producing proof of payment and such withdrawal

G. Acts Covered under this Scheme

1. the Central Excise Act, 1944 or the Central Excise Tariff Act, 1985 or Chapter V of the Finance Act, 1994 and the rules made thereunder.

2. the Agricultural Produce Cess Act,1940

3. the Coffee Act, 1942;

4. the Mica Mines Labour Welfare Fund Act, 1946; (iv) the Rubber Act, 1947; (v) the Salt Cess Act, 1953;

5. the Medicinal and Toilet Preparations (Excise Duties) Act, 1955;

6. the Additional Duties of Excise (Goods of Special Importance) Act, 1957;

7. the Mineral Products (Additional Duties of Excise and Customs) Act, 1958;

8. the Sugar (Special Excise Duty) Act, 1959;

9. the Textiles Committee Act, 1963;

10. the Produce Cess Act, 1966;

11. the Limestone and Dolomite Mines Labour Welfare Fund Act, 1972;

12. the Coal Mines (Conservation and Development) Act, 1974;

13. the Oil Industry (Development) Act, 1974;

14. the Tobacco Cess Act, 1975;

15. the Iron Ore Mines, Manganese Ore Mines and Chrome Ore Mines Labour Welfare Cess Act, 1976;

16. the Bidi Workers Welfare Cess Act, 1976;

17. the Additional Duties of Excise (Textiles and Textile Articles) Act, 1978;

18. the Sugar Cess Act, 1982;

19. the Jute Manufacturers Cess Act, 1983;

20. the Agricultural and Processed Food Products Export Cess Act, 1985;

21. the Spices Cess Act, 1986;

22. the Finance Act, 2004;

23. the Finance Act, 2007;

24. the Finance Act, 2015;

25. the Finance Act, 2016;

Our Comment:

- The Hon’ble Finance Minister in her first budget has said that the intention of this scheme is to curb/dispose the pending litigation related to Pre-GST regime. The said scheme is a welcome step and must be appreciated in as much it provide a onetime option to all those person who wish to dispose the pending litigation by paying the tax due @ 30 to 60%. Also there is a compete waiver of Interest and penalty.

- This scheme intends to curb the old litigation however there is no option of voluntary disclosure. In such case the object to curb pending litigation may not be achieved.

- Further DCs should not be given discretion to reject application if all the tests are satisfied. Further there is no clarity with regards to withdrawal of pending appeal in case declaration is filed. Government also needs to clarify that filing declaration shall not be treated as admission of liability in case of rejection of declaration by the DC.

- The declarant should carefully go through the scheme and ensure that he is eligible declarant under said scheme and he is ready to pay the liability as declared and finally accepted by DC.

Author Bio

sir how deducte in tax

please tell me the difference between declaration and voluntary Disclosure?