Pension: A Necessity

By

Dr. Deepak Mohanty1

I thank Professor (Dr.) Tarun Agarwal, Director, National Insurance Academy (NIA), Pune, for this opportunity to interact with the esteemed faculty and distinguished invitees.

There is considerable synergy between insurance and pension for old-age income security and wellbeing. There are two key concerns on retirement: drop in income and rise in health-related expenditure. In this scenario pension and health insurance could, to a great extent, mitigate these concerns. When we speak of pension, that is a predictable flow of regular income, annuity becomes an important instrument. In fact, the National Pension System (NPS) that PFRDA regulates, on exit a subscriber ought to have atleast 40 percent of her accumulated corpus in annuity to ensure a lifelong income.

I propose to speak on NPS and place it the overall context of our demography and labour force.

Pension provides a safety net to an individual, giving financial security during retirement. The notion of pension might not be the first thing on everyone’s mind when they start earning, though it ought to be. In the matter of pension an early start is a head start: small amounts squirreled away could yield substantial corpus by harnessing the power of compounding. People often have various financial priorities and may not always consider retirement planning until later in life. Factors like immediate consumption needs and other financial goals can take precedence. As people age and their priorities shift, the importance of having a pension or some form of retirement savings becomes increasingly apparent. When it comes to retirement security in India, there are certain schemes for organized sector workers, the prominent one being provident fund offered by the Employees’ Provident Fund Organisation (EPFO). Governments, both at the central and state levels, provide some social security benefits to low-income households. Given our large population and relatively low per capita income, it would be fiscally unsustainable for the governments to provide pension to every individual. However, it is important to bear in mind that benefit from any single scheme for an average person could never be adequate. It is therefore prudent for individuals to take their own initiative for maintaining standard of living post-retirement by starting retirement planning early.

India is at its demographic peak. Currently we are the world’s most populous young country with a population count of over 1.4 billion. In terms of economic growth, we are the fastest growing large economy. Our young population is an important factor that is driving growth and if expected to continue to do so in the near future catapulting India to a high-income country by the middle of this century.

India is also projected to age rapidly. Our old-age dependency ratio, i.e., population over 65 years of age per 100 working age (15-65 years) population has risen from 7.4 in 2000 to 10.1 in 2021. This trend is likely to accentuate: every fifth Indian is expected to be over 65 years by the middle of this century. Life expectancy has doubled since independence from 35 years in 1950 to 70 years at present and is expected to increase further. Its financial implication will be disproportionately large unless working-age population make provisions for their future.

The composition of our labour force creates its own challenge to retirement planning: In our total population of over 140 crore, around 3/4th (105 crore) are over 15 years of age2 . Out of these, 58 percent (61 crore) participated in the workforce3, as on December 2023. As per the Ministry of Labour, around 93 percent of the labour force, about 57 crore, is in unorganized sector where there is no statutory provision for social security. The rise of the gig economy and digital platforms has transformed the nature of work in India. Freelancing, online marketplaces, and app-based services have provided new avenues for employment, especially for young people and those seeking flexible work arrangements. However, in this work there is no employer-led social security.

India is also going through rapid social and cultural churn impacting post-retirement life. Traditionally, in India, multigenerational households were the norm, with elders living with their children and grandchildren in a joint family system. However, with changing lifestyles, urbanization, and evolving family structures, the concept of retirement homes or senior living communities is gaining popularity. According to a Position paper by NITI Aayog, 78 percent of our older population is currently living without any pension cover. So, unless we prepare for old age social security now, it will be increasingly challenging.

Against this demographic backdrop and labour market characteristics, where does the National Pension System (NPS) stand? NPS provides a good platform for the citizens of India, designed to deliver sustainable solution for having adequate retirement income in old-age. It is a defined contribution (DC) pension scheme which facilitates accumulation of a pension corpus during the working life of the subscriber with flexible investment choices.

NPS was initially introduced for the Central Government employees in 2004. It was subsequently adopted by most state governments to provide retirement benefit to their employees. Later on, NPS was opened for all citizens of India in 2009 and to the corporate sector in 2011. At present, NPS can be subscribed by any Indian citizen aged between 18-70 years and can also be adopted by any employer as a retirement benefit scheme for its employees on a voluntarily basis.

In terms of its operation, NPS has an unbundled architecture with each intermediary undertaking a specialized activity in a professional and cost-effective manner attaining economies of scale. This unique architecture helps minimizes risk of sole dependency on entities involved and eliminates risk of failure of the system.

NPS offers flexibility to the subscribers with respect to:

(i) Choosing the Central Recordkeeping Agency (CRA) – Subscriber can choose any

CRA out of three available registered CRAs for recordkeeping and administration of their retirement account.

(ii) Pension Fund Manager (PF) – Subscriber can choose any three out of eleven PFs registered with PFRDA for managing their funds in different asset classes including equity, corporate debt, government securities and alternate assets.

(iii) Investment Choices – There are two choices available – “Active-Choice” and “Auto-Choice”. Subscribers can choose “active choice” if they want to actively decide their investment composition into equity, corporate debt, government securities and alternate assets as per their preference. Alternatively, subscriber can also go for “auto-choices” under which they can choose between 3 Life Cycle funds, wherein the allocation under equity and corporate debt automatically reduces as age increases. Under auto choice, subscriber can go for conservative or moderate or aggressive choice as per their risk appetite.

(iv) Annuity Service Providers (ASP) – At the time of superannuation, the subscriber can choose any one ASP out of fifteen ASPs currently empaneled by PFRDA. Subscriber can even opt for multiple annuity-plans under one chosen ASP as per his agreement with the ASP.

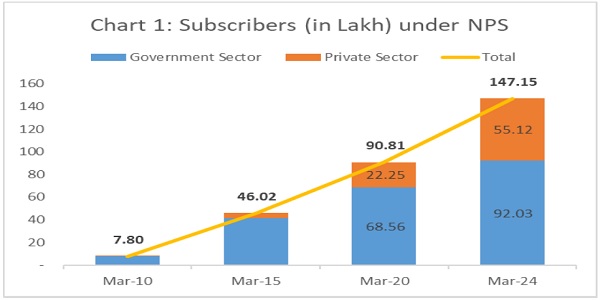

In the recent years NPS has shown steady progress. The number of subscribers under NPS have grown at a compounded annual growth rate (CAGR) of 13 percent since March 2020 from 90.81 lakh to 147.15 lakh in March 2024 (Chart 1). The growth rate of private sector subscribers (25 percent) is much higher as compared to government subscribers (8 percent). Similar trend is observed in the growth of Assets under management (AUM).

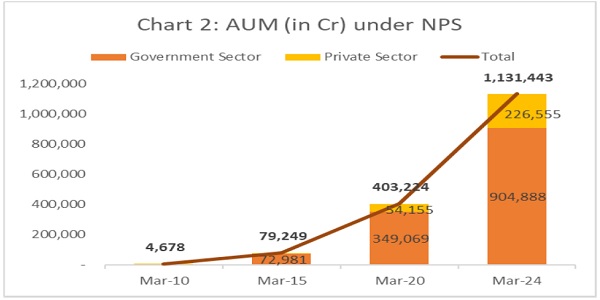

The Assets under management (AUM) of NPS have increased at a compounded annual growth rate (CAGR) of 29 percent since March 2020 from Rs. 4.03 lakh crore to Rs. 11.31 lakh crore (Chart 2). The growth rate of private sector AUM under NPS (43 percent) was much higher as compared to the government sector (27 percent).

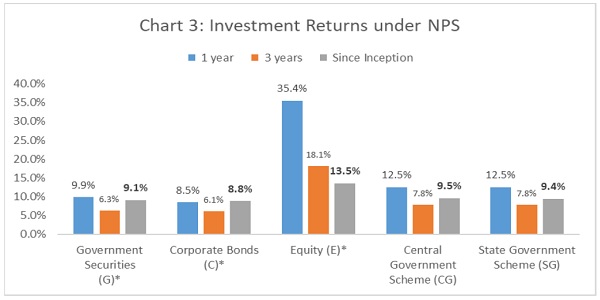

The growth rate of the AUM under NPS could partly be attributable to competitive investment returns generated by professional pension fund managers (Chart 3). For example, equity portfolio under NPS has provided a return of 35.4 percent during 202324; and since inception 13.5 percent per annum.

The AUM under NPS is deployed in various asset classes such as government securities, corporate bonds, equity and alternate assets (REITs / INVITs). The deployment into various assets class depends on the investment choice opted by the subscribers. The AUM under equity was about 19 percent and that under government security was about 54 percent of the entire corpus as of March 2024 (Chart 4).

Long way to “Pension for All”. Notwithstanding steady growth of NPS, we have so far covered only about 5 percent of India’s total population4. If we look at the broader basket of our retirement fund assets, including that with EPFO, insurance companies and mutual funds, it works out to 16.5 percent of GDP; with NPS at 3.9 percent of GDP. This is relatively low considering global average of 81 percent for OECD Countries in 2022. The assets under pension funds being long-term boosts investment in infrastructure. For example, 24 percent of NPS corpus is invested in corporate bonds, largely infrastructure. For a rapidly growing economy like ours availability of long-term funds becomes critical to build physical infrastructure. Also, the long-term investment of pension assets helps stabilizes financial markets.

Way Forward

The NPS has made pension available to all irrespective of one’s income and employment status. However, the take-up rate is low, even among people who have the income to contribute, partly due to low level of awareness. Going forward our effort is to increase coverage of NPS following a three-pronged strategy: Access, Awareness and Acceptance (AAA).

Access: We have been working on improving the accessibility of NPS both digitally and physically to every citizen of India. Digitally, we are reducing the journey time of digital onboarding for the ease of the subscriber. We have taken on board many fintech companies as Points of Presence (POPs) with us. On the other hand, under the physical channel, we are trying to increase the touch points by activation of the branches of our POPs, i.e. mostly commercial banks, to improve last mile connectivity of NPS.

Awareness: Financial literacy remains low, not only in our country but also globally. For example, OECD/INFE 2023-International Survey of Adult Financial Literacy showed that on an average, only one-third of people surveyed across 60 countries had adequate financial literacy. RBI-NCFE Financial Literacy Survey for India suggested that only 25 percent of people are thinking to make retirement savings. As in the standard-curriculum, aspects of personal finance are not generally covered, very few individuals actually understand; or if they understand, not able to reflect in financial decision making. It is essential to have the knowledge of basic financial concepts like compounding or time value of money, inflation or purchasing power of money, relation between risk and reward, financial frauds or scams.

As a regulator, we have taken several initiatives for promoting financial literacy such as empanelment of retirement planners, appointment of training agencies, awareness sessions for corporates and reaching out to social media though various initiatives and media agencies. However, considering the large population of our country, there is substantial gap that needs to be filled.

Acceptance: With greater financial awareness and flexible product features, we endeavor to increase the acceptance of NPS among the masses as a retirement solution. One critical aspect for acceptance of the product is the ability to pay. Currently, with per capita income of around US $2500, we are a lower middle-income country, as per the World Bank classification. With sustained GDP growth, the country shall progress to an upper middle-income country with per capita income of upwards of US $4,200 in the next decade. We aspire to be a high income developed country by the middle of the century. With this, we expect the ability of our citizen to pay for retirement income would also improve and NPS would be embraced by the society at large.

Currently, NPS is considered as a voluntary option by the corporate sector for their employees. Many countries have tried auto-enrolment to enhance pension coverage wherein the employees beyond a threshold salary level are auto-enrolled in to pension in some cases with opt out options. Such a nudge may create greater acceptance which is in the long-term interest of the employee.

Conclusion:

As a Regulator, PFRDA is endeavouring to strengthen the regulatory architecture to improve the product design, providing choices and expanding the touch points for easy accessibility of NPS.

In this direction, soon we would be launching a “balanced life cycle fund” with higher allocation to equity (upto 50 percent) in the younger age of contribution and the tapering of equity would start from the age of 45 years. This would help in maximizing the pension wealth in the longer-run while optimizing the risk and return. This product would be rolled out in a few months following system development.

Finally, I would like to say that pension as a product has no easy substitute, it is designed to save for retirement in a disciplined manner during the working-age for an individual to lead a dignified life post- retirement.

Thank you.

Notes:

1 Address at National Insurance Academy (NIA), Pune by Dr. Deepak Mohanty, Chairperson, Pension Fund Regulatory and Development Authority (PFRDA), on 03rd May 2024.

2 Population Projection Report 2020 (MoHFW)

3 LFPR 60% and WPR 58% in Dec 2023 as per PLFS.

4 Under both NPS and APY