Text of Rule 8: –

8. Non-Applicability.

Companies (Significant Beneficial Owners) Rules, 2018 shall not be made applicable to the extent the share of the reporting company is held by,

(a) the authority constituted under sub-section (5) of section 125 of the Act;

(b) its holding reporting company:

Provided that the details of such holding reporting company shall be reported in Form No. BEN-2.

(c) the Central Government, State Government or any local Authority;

(d) (i) a reporting company, or

(ii) a body corporate, or

(iii) an entity,

controlled by the Central Government or by any State Government or Governments, or partly by the Central Government and partly by one or more State Governments;

(e) Securities and Exchange Board of India registered Investment Vehicles such as mutual funds, Alternative Investment Funds (AIF), Real Estate Investment Trusts (REITs), Infrastructure Investment Trust (InvITs) regulated by the Securities and Exchange Board of India,

(f) Investment Vehicles regulated by Reserve Bank of India, or Insurance Regulatory and Development Authority of India, or Pension Fund Regulatory and Development Authority.

Explanation for Rule 8(b):

Rule 8(b) provides a relaxation to a reporting company which prima facie required to comply with the requirements of Companies (Significant Beneficial Owners) Rules, 2018 (hereinafter referred to as “SBO Rules”), but if Rule 8(b) is applicable, then despite such company having a clearly identifiable SBO, shall not be required to file particulars of such SBO in Form BEN-2.

For taking the relaxation under Rule 8(b) certain requisites become mandatory:

1. The reporting company shall be a subsidiary company in terms of Section 2(87) of the Companies Act, 2013.

2. The Holding Company must be a “Company” registered in India under the Companies Act, 2013 or under any previous company laws. That means, even an Indian Body Corporate’s Indian Subsidiary Companies will not be able to take the benefit.

3. The Holding Company should also be a “reporting company” under Rule 2(1)(f) of the SBO Rules, that means, the holding company itself must have its own identifiable SBO.

Why the requisites are mandatory?

The language of Rule 8(b), provide that the SBO Rules shall not be applicable to the extent of the shares of a reporting company is held by “holding reporting company”. The term “holding reporting company” itself makes it mandatory to have such requisites.

Let’s analyse:

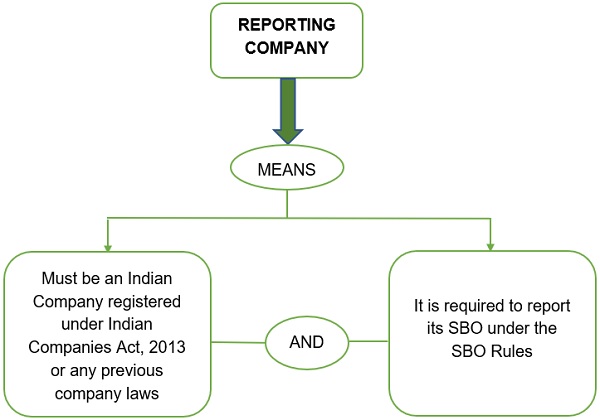

Meaning of Reporting Company:

As clearly mentioned in the diagram, the above mentioned are the two essentialities for any company to get fit into the definition of “reporting company” & hence, when the Rule 8(b) says that shares of any reporting company shall be held by a “holding reporting company” that definitely will mean that holding company shall also be a reporting company as per the SBO Rules, and a reporting company will always be an Indian Company. Therefore, the 3 requisites shall be fulfilled for taking the benefit under Rule 8(b).

Let’s learn through some illustrations:

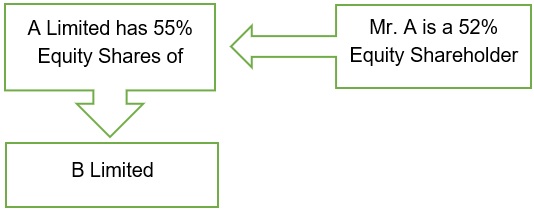

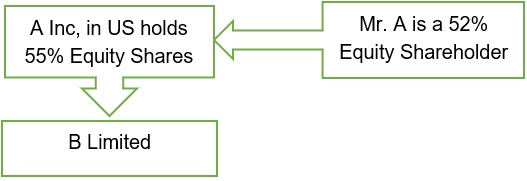

Illustration 1-

Is Mr. A an SBO for B Limited? – Answer is Yes. B Limited should file Form BEN-2.

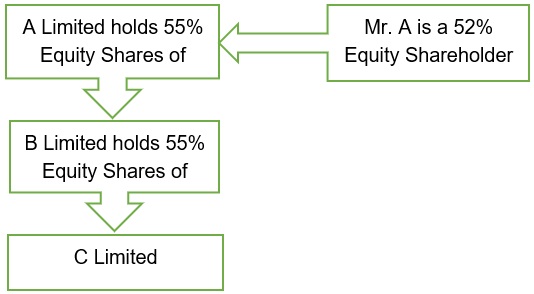

Illustration 2-

Is Mr. A an SBO for B Limited? – Answer is Yes.

Is Mr. A an SBO for C Limited? – Answer is No. Because, C Limited is fulfilling the 3 requisites for taking the benefit of Rule 8(b), i.e. first, it’s a subsidiary company, second, it’s holding company is an Indian Company, and third, the holding company has an identifiable SBO, Mr. A. But C Limited should file Form BEN-2 for filing details of its holding reporting company, B Limited under proviso to Rule 8(b).

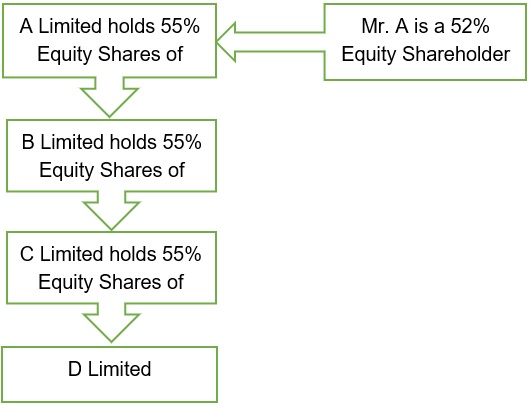

Illustration 3-

Is Mr. A an SBO for B Limited? – Answer is Yes. B Limited should file Form BEN-2

Is Mr. A an SBO for C Limited? – Answer is No. But filing of Form BEN-2 is mandatory under proviso to Rule 8(b) for filing details of its holding reporting company B Limited.

Is Mr. A an SBO for D Limited. Answer is No. It is also not required to file Form BEN-2.

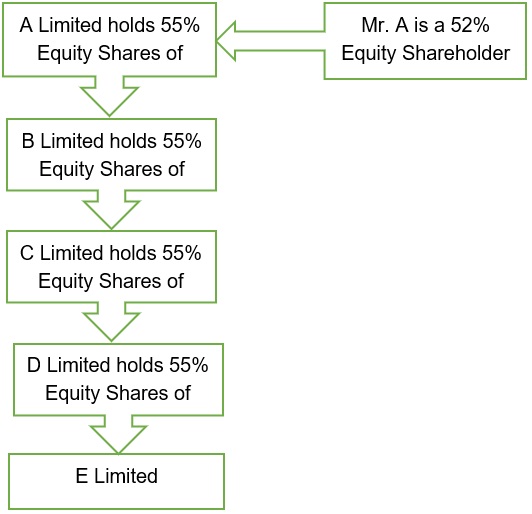

Illustration 4-

Is Mr. A an SBO for B Limited? – Answer is Yes. It is required to file Form BEN-2.

Is Mr. A an SBO for C Limited? – Answer is No. But filing of Form BEN-2 is mandatory under Rule 8(b)-proviso by C Limited.

Is Mr. A an SBO for D Limited? – Answer is No. Also, no filing of Form BEN-2 is required.

Is Mr. A an SBO for E Limited? – Answer is No. Also, no filing of Form BEN-2 is required.

Illustration 5-

Is Mr. A an SBO for B Limited? – Answer is Yes. B Limited should file Form BEN-2.

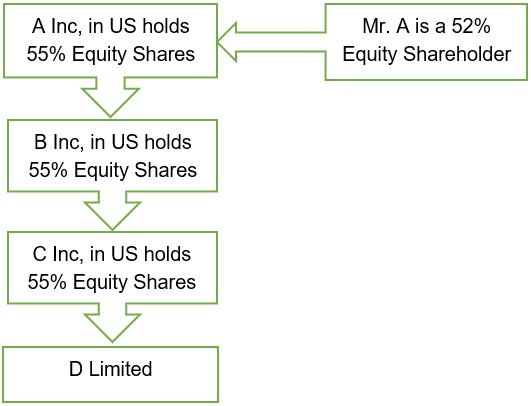

Illustration 6-

Is Mr. A an SBO for D Limited? – Answer is Yes. D Limited should file Form BEN-2.

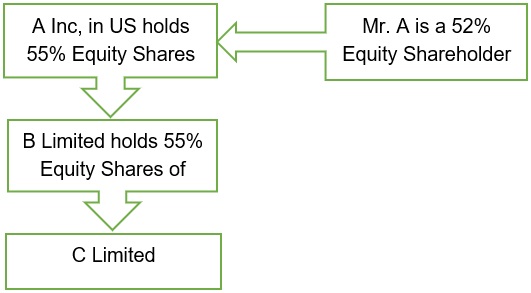

Illustration 7-

Is Mr. A an SBO for B Limited? – Answer is Yes. B Limited should file Form BEN-2.

Is Mr. A an SBO for C Limited? – Answer is No. But C Limited should file Form BEN-2 under Rule 8(b)-proviso.

Author Bio