Corporate Environments is Dynamic in nature it is ever changing. Globalization and liberalization have brought about significant changes in the attitudes and perceptions of the corporate world.

Corporate Environments is Dynamic in nature it is ever changing. Globalization and liberalization have brought about significant changes in the attitudes and perceptions of the corporate world.

Indian Accounting Standards (IndAS)is paradigm shift in accounting practices, It will reduce the diversity in accounting practices and bring transparency in financial reporting process that will helps to build trust and faith to stakeholders on Company’s financial statements.

Ind AS is a set of accounting rules, principles and policies which are converged with International Financial Reporting Standards (IFRS).

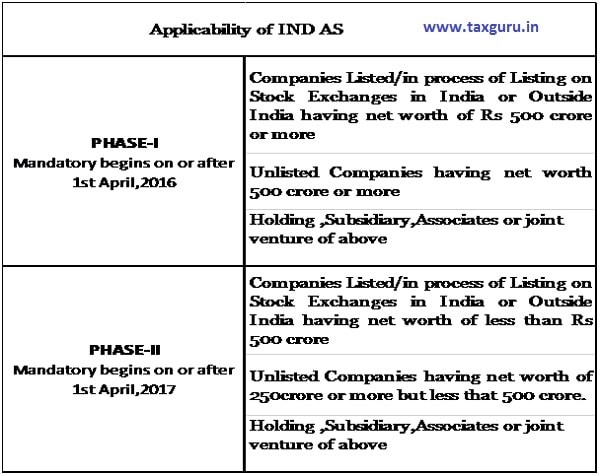

The Ministry of Corporate Affairs(MCA) vide its notification dated 16th February, 2015 announcing the Companies(Indian Accounting Standards) Rules, 2015 for phase- wise implementation of Indian Accounting Standards (Ind AS).

Non – Applicability of IND AS

- Insurance Companies, Banking Companies and Non – Banking Finance Companies,

- Companies listed or in process of being listed on SME exchange as referred to in chapter XB or on the institutional trading platform without initial public offering in accordance with the provisions of chapter XC of Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009.

- Overseas subsidiaries, associates, Joint Ventures of an Indian Company is not required to prepare its stand- alone financial statements as per the IND AS.

NOTES:

- “Net worth” has been defined to have the same meaning as per section 2(57) of the Companies Act, 2013. It is the aggregate value of the paid-up share capital and all reserves created out of the profits and securities premium account, after deducting the aggregate value of the accumulated losses, deferred expenditure and miscellaneous expenditure not written off, as per the audited balance sheet, but does not include reserves created out of revaluation of assets, write-back of depreciation and amalgamation.

- Ind AS applicable on consolidated as well as stand-alone financial statements.

- On the basis of above criteria, once a Company starts following the Ind AS, is shall be required to follow the Ind AS for all subsequent financial statements even if any of the criteria specified in this rule does not subsequently apply to it.

- Companies which is not fall on above criteria may voluntarily adopt the Ind AS, once Companies adopt Ind AS they cannot switch back.

- The Companies which are not required to follow Ind AS shall comply with the Accounting Standards as Specified to the Companies (Accounting Standards) Rules, 2006.

- The rules prescribed that if there any Conflict between Ind AS and a law, the provisions of the law shall prevail and the financial statements shall be prepared in conformity with it.

Conclusions:

Implementation of Ind AS in financial statements reporting process of Companies will brings loads of changes in the areas of revenue recognition, provisioning, capitalisation, depreciation,treatments, presentation etc. it will affect the profitability and net worth of the organisation.

Therefore, accounting practitioner, analyst, and stakeholder should adopt the changes and brings reporting process more reliable and flexible and should be par with International Financial Reporting Standards (IFRS).

About the author:

Mr. Ashish Pratihast, an associates member of The Institute of Company Secretaries of India (ICSI) and post graduate in Commerce.