CS S. Dhanapal

CS S. Dhanapal

Effective Date for CSR Applicability – Section 135 of the Companies Act 2013, Schedule VII and the relevant rules, namely Companies (Corporate Social Responsibility Policy) Rules, 2014 have been notified to become effective from 01st April 2014 vide MCA notification dated 27.02.2014.

Amendment to Schedule VII – Schedule VII which contains list of activities which can be undertaken by a company as part of its CSR initiatives has been amended vide this notification and companies must refer to the new list for undertaking qualified CSR activities.

Changes in CSR Rules – There are many welcome changes in the CSR Rules which have been notified now as compared to the draft rules which were issued for public comments previously. Many of the ambiguities in the Section and the draft rules have been addressed in the final notified rules.

CSR Applicability – Every company including its holding or subsidiary, and a foreign company defined under clause (42) of section 2 of the Act having its branch office or project office in India, which fulfills the criteria given below

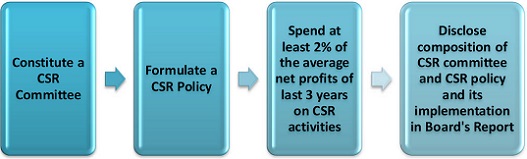

- CSR Mandate (What should the above companies do?) –

IMPORTANT CLARIFICATIONS INTRODUCED VIA RULES

- Meaning of Net Profit for CSR Purpose – “Net profit” means the net profit of a company as per its financial statement.

- Requirement of atleast 1 independent director in CSR Committee – Unlisted public companies and private companies which are not required to appoint an independent director shall have its CSR Committee without such director

- Requirement of atleast 3 directors in CSR Committee – a private company having only two directors on its Board shall constitute its CSR Committee with two such directors

- CSR Expenditure –

- Contribution of any amount directly or indirectly to any political party under section 182 of the Act, shall not be considered as CSR activity.

- Companies may build CSR capacities of their own personnel as well as those of their Implementing agencies but such expenditure shall not exceed 5% of total CSR expenditure of the company in one financial year.

- CSR Implementation through Trust/Society- The Board of a company may decide to undertake its CSR activities approved by the CSR Committee, through a registered trust or a registered society or a company established by the company or its holding or subsidiary or associate company under section 8 of the Act or otherwise.

- Non applicability in subsequent years – Once a company falls within the ambit of CSR applicability, it has to comply with all the CSR provisions until the completion of 3 consecutive years for which CSR applicability does not arise.

(Written by S.Dhanapal, Senior Partner, S Dhanapal & Associates, A firm of Practising Company Secretaries, Chennai.)

The Rule States That “the Company along with its holding and subsidiary”.

What does it mean.

Should we club the profit of all companies viz holding and subsidiary to claculate the eligible amount of CSR