Journey from Internal Audit to Forensic Audit

The authors here have tried to make an attempt to reach out to the fellow Seniors, members, students, etc. that in this age of digital age of AI, technology and (mis) information, FRAUDS are quite often form integral part of any financials. Any professional providing any type of services to any client should be diligent and must have an attitude of Professional Skepticism and pursue the issue to a logical end. This is a real-life case-study dedicated to the professionals, which clearly indicate that working honestly and providing value-addition to the client adds tremendous value in the professional life.

Case-Study: –

PQR Engineering Corporation (PQR) is a medium sized Global Company with a turnover of around 5,000 crores. It is engaged in EPCM (Engineering, Procurement, Construction Management) and LSTK (Lump Sum Turnkey Projects) jobs having its operations both in Indian as well as in overseas market. Generally, in EPCM job, the EPCM contractor provides consultancy to the contractors who provide the construction services, advise & assistance to the client/owner. In this model, the EPCM contractor is not involved in the actual construction work. In LSTK jobs, the contractor undertakes the responsibility for executing the complete contract work for a fixed price agreed before the contract begins. Therefore, in LSTK jobs the contract price is fixed by the client and does not change (unless there are “Change Orders”, duly approved by the Client) on the Income front. It is the expenses that requires greater attention and must be examined diligently and critically, as any overrun in costs involves losses to the company to that extent and affects the bottom line.

The auditors were the internal auditor of PQR, wherein their scope included routine internal audit and review of one project in every quarter, for which they were also given the open mandate to visit the sites. During a particular quarter, the auditor had selected 1 project (out of 13 ongoing projects across the length and breadth of India) for its review and started performing to apply checks as per the audit plan of the internal auditing firm. The audit plan inter alia also included one such area of Review of purchase orders issued by the company. While reviewing the purchase orders, the auditor observed one instance, whereby the scope of a particular vendor namely M/s. ABC Products Incorporate (ABC) was reduced by Rs. 80,814/- and these materials were procured from another vendor M/s. XYZ Industries at a price of Rs.1,59,500/- by issuing a fresh RUP (Request for urgent procurement). The cost comparison of ABC and XYZ has been tabulated below for reference:

| Sr. No. | Item Code/

Tag no. |

Qty involved | ABC Products Inc. | XYZ Industries | % Increase in Price | ||

| Rates | Total (Rs.) | Rates | Total (Rs.) | ||||

| 1 | CAGBSCAHAH | 1 | 808 | 808 | 5,000 | 5,000 | 619 |

| 2 | RBGBSCAHAH | 1 | 2,696 | 2,696 | 8,000 | 8,000 | 297 |

| 3 | TAHBSCAIAI | 1 | 12,750 | 12,750 | 39,500 | 39,500 | 310 |

| 4 | EAGBSCAJ | 2 | 5,940 | 11,879 | 6,500 | 13,000 | 109 |

| 5 | EAHBSCAH | 2 | 1,568 | 3,135 | 3,500 | 7,000 | 223 |

| 6 | TAGBSCAHAH | 1 | 850 | 850 | 8,000 | 8,000 | 941 |

| 7 | EAHBSCAL | 2 | 24,348 | 48,697 | 39,500 | 79,000 | 162 |

| Total | 10 | 80,814 | 159,500 | 197 | |||

The auditors were surprised by looking at the rates given to the offloaded vendor (XYZ), for which the obvious questions that need to be answered were:

a. Why were these items not supplied by the Original vendor?

b. How come the offloaded vendor has charged almost double? So, whether these additional costs are recovered from the original vendor or at least a penalty is charged for non-performance of the Contract?

c. How critical the materials were?

d. The nature of urgency?

The above issue was discussed with the Finance head of the Company and the finance head very quickly and easily responded that in a project of Rs. 2,854 Crores (spanning for 2-3 years), Rs. 80,000/- are peanuts and the auditors were also reminded about the past experience and helpful nature of the vendors. Unfortunately, the merit of the issue was not taken seriously by the Company at that point of time and the auditors were not convinced.

Pondering about the questions the site visit was due and the auditors visited the site. During site visit, while conducting the physical verification of stock, the auditors were surprised to observe that the materials which were procured at almost double rates (as mentioned above) were lying at the site. They then started to analyze the chronology of this particular issue. The sequence of events occurred were as follows:

| Sr. No. | Events | Date of the event |

| 1 | Original Purchase order issued to ABC | January 2014 |

| 2 | Contractual Delivery Date (CDD) of ABC | May 2014 |

| 3 | Materials Reduced from the scope of ABC | December 2014 |

| 4 | Raising of RUP on XYZ | December 2014 |

| 5 | CDD of XYZ | January 2015 |

| 6 | Actual receipt of material at site | April 2015 |

| 7 | Site visit of auditor, wherein the above materials were lying at the site. | January 2016. |

After Juxtaposing all the information, the auditors realized that it was the illusion of urgency which was created by the Company, shown to the management for overcoming the general purchase order process & procedures, and hence the RUP.

Keeping all the above facts in the mind, the auditors again started enquiring, wherein the following explanations were provided to the auditor.

a. The original vendor could not deliver in time; hence the materials were relocated (i.e, offloaded to another vendor)

b. As the material was urgently required at site, hence the RUP was done, by relaxing the procurement process, instead of normal purchase order.

c. For double cost it was explained that the offloaded vendor has charged for the opportunity cost & the premium for supplying within 20 days at site.

d. The penalty or the recovery of the additional costs from ABC will be done at the end of the project after reviewing the entire performance of the vendor.

Now the above said issue was forming the part of the detailed report, but it was not discussed with the Audit Committee in the March 2016 quarter, as the amount was considered IMMATERIAL by the Director – Finance (DOF). It was very clearly informed to the auditors that for Rs. 80,000 excess costs incurred, the Audit Committee’s time should not be wasted. On further emphasis by the auditors, the DOF signed and ratified the decision citing it as business decisions taken by the Company and somehow the said issue was not taken up with Audit Committee for the quarter ended March 2016.

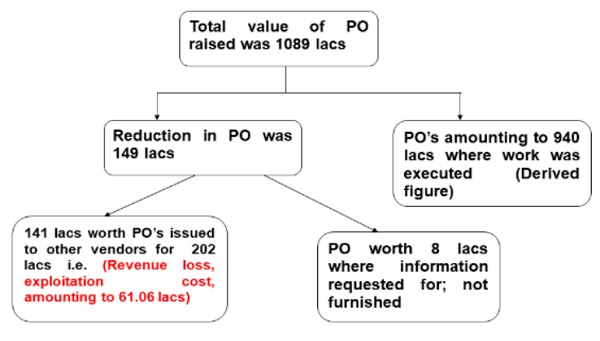

In the next quarter, i.e, June 2016 quarter, the audit partner-in-charge, decided to review all the purchase orders of ABC across all the projects (as there were 13 ongoing projects).

After conducting the thorough review of the purchase orders issued to ABC, the following summarized details were produced before audit partner-in-charge.

Now, the above facts speak for itself!!! When these facts were discussed with the DOF, he was uncomfortable, and he sounded out that there is some BIG ISSUE over here.

After 3-4 days, the DOF called the meeting with Partner-in-charge and appreciated the work of the Internal audit team and also took the charge to clean up this mess at the earliest. The DOF then called for an emergency Board Meeting, wherein the above facts were discussed with the management during June quarter’s report and also presented before the Audit Committee of the Company, wherein all the Committee members (including INDEPENDENT DIRECTORS) were taken aback by these findings.

Then as per the directions of the Audit Committee and DOF, the Company requested the audit firm to conduct the detailed study (thoroughly investigate) for all such cases and submit the report by next quarter meeting.

So, by this way a diligent and smart-working internal auditor got tremendous appreciation from the Company and its Audit Committee and also got one big new assignment. Also, the independent director who was part of the Audit Committee recommended the internal auditor in a big way to several leading business houses.

Conclusion:

In the above case, if the auditors had prima-facie relied upon the explanations provided by the auditee, then it would altogether be a different ball game. Hence in the above case, the auditors had critically evaluated all the facts by extending audit procedures, which has resulted into the fruitful result & an immense value-addition to the management.

Here the authors would like to emphasize the concept of professional skepticism and the spirit of not giving up easily due to element of materiality and lack of time, resource & costs constraints. It may sometime also happen that even after having the attitude of professional skepticism, some facts might go unreported/undetected (which would be very minimal, unless the top management has colluded and done something different), but documenting such critical evaluations done by the auditor will act as a detrimental factor against any allegations of misstatement/errors/fraud detected later for or against the company.

Compiled by:

CA. Govindsingh B. Purohit and CA. Kamlesh D. Malviya

Email govindsinghpurohit@chetandalal.com, kamleshmalviya@chetandalal.com

Cell – +91 97688 59386, + 91 96197 69473