All about Property Taxation along with latest changes proposed in Final Budget, 2024

As we know, definition of Capital Assets under Section 2(14) of Income Tax Act, 1961 includes property of any kind held by assessee, whether or not connected with business or not. If there is any gain or profit from transfer of capital assets then it shall be chargeable to tax under the head “Capital Gain” in the previous year in which transfer took place. As per above definition, capital asset includes immovable property hence if we sale immovable property then any profit or gain arises from transfer of that immovable property shall be taxable under the head “Capital Gain” in the year in which such property is sold.

For e.g. If property is sold in the year 2023-24 then any profit or gain arised from such property shall be taxable as Capital gain in the year 2023-24. Sometimes question arises in ordinary person mind that if we sale residential property then why we need to pay tax as we not consuming this property in our business or it is not commercial property. Now it is important to note that definition of capital asset has been drafted in such a way that it includes both residential as well as commercial property therefore we have to pay tax on sale of property irrespective of the nature of property. Our Honorable Finance Minister “Nirmala Sitharaman Ji” in the recent Final Budget of 2024 has proposed some important changes regarding taxation of property that will be discussed further in this article.

Pre Budget 2024 Position on Property taxation-:

Type of Capital Gain on Sale of Property

If the immovable property, being land or building, is sold after 24 months from the date of purchase then it shall be classified as Long Term Capital Assets and if it is sold before 24 months from the date of purchase then it shall be classified as Short Term Capital Assets.

Now the question arises why we need to divide the immovable property into Long Term Capital Asset and Short Term Capital Asset. This is because applicability of rate of tax on sale of capital asset is different on both Long Term Capital asset as well as Short Term Capital asset which are discussed below-:

For Long Term Capital Assets (i.e. immovable property sold after 24 months)

As per section 112 of Income tax Act, 1961 If we sale the Long Capital Asset then any profit or gain arises from sale of such property shall be taxable at flat rate of 20%.

For Short Term Capital asset (i.e. immovable property sold before 24 months)

If we sale the Short Term Capital Asset then any profit or gain arises from sale of such property shall be taxable at normal tax rates i.e. slab rate as applicable.

| Particulars | STCG on Property | LTCG on sale of Property |

| Tax rates | Slab Rates | 20% |

Benefit of indexation

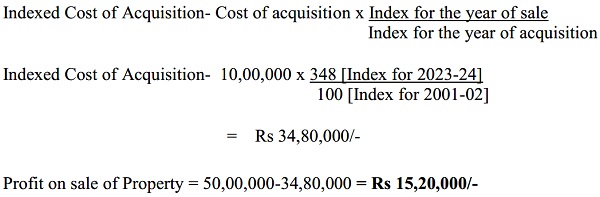

As we know Inflation rate is increasing day by day in the developing country like India. Therefore, suppose if we purchase the property in 2001-02 for Rs. 10, 00,000/-and sold it in year 2023-24 for Rs 50, 00,000/-. Now as we discussed above any profit or gain arises from sale of property shall be taxable under the head “Capital Gain” in the year in which property is sold. Calculation of profit or gain is discussed below-:

Sale Consideration i.e. sale value of property – Rs 50, 00,000

Purchase cost of property – Rs 10,00,000

Profit on sale – Rs 40,00,000 [50L-10L]

Now if we say profit of Rs 40,00,000 will be taxable under the head capital gain then it would be very unfair as propertyis purchased in 2001-02 and now if we take the same cost as it purchased in 2001-02 then it would not be fair as we know inflation is increasing day by day and value of property that was purchased in 2001-02 shall not same in year 2023-24 for the prospective of inflation rate..

Therefore Govt. gave the benefit of indexation on Long Term Capital Assets (i.e. sold after 24 months). Now whenever we calculate the profit or gain on sale of property then we will take indexed cost of acquisition instead of cost of acquisition.

Impact of Indexation in continuation with above example

Now we can clearly see the impact of indexation that, now Rs 15,20,000 shall be taxable as Capital Gain as compared to Capital Gain without indexation for Rs 40,00,000. It is important to note that we can take the benefit of indexation only on Long Term Capital Asset i.e. property sold after 24 months.

Calculation of Long Term Capital Gain/loss

| Particulars | Amount |

| Sale Consideration | xxxx |

| Less: Indexed Cost of Acquisition | xxxx |

| Less: Indexed Cost of Improvement | xxxx |

| Less: Transfer Expense | xxxx |

| Gross Long Term Capital Gain | xxxx |

| Less : Exemption u/s 54/54EC/54F | xxxx |

| Taxable Long Term Capital Gain | xxxx |

Some Important Points to be consider on sale of property

> If the property is purchased before 01.04.2001 then we can take the benefit of Fair Value of Property as on 01.04.2001. It means suppose if property is purchased in year 1988-89 for Rs 10,00,000/- and fair value as on 01.04.2001 is Rs 25,00,000/- then we can take the Rs 25,00,000/- as cost of acquisition for calculating indexed cost of acquisition.

> If the sale value exceeds the stamp duty value of property and difference is more than 10% of consideration then as per section 50C of the Income Tax Act, stamp duty value shall be considered as full value of consideration for calculating capital gain on sale of such property.

For e.g. – If Sale Value is Rs 45,00,000 and stamp duty value of the same property is Rs 50,00,000. Now the difference is Rs 5,00,000 which is more than the 10% of consideration i.e. Rs 4,50,000 [45,00,000*10%]. Therefore stamp duty value i.e. Rs 50,00,000 shall be considered as full value of consideration for calculating capital gain as per section 50C.

> If there is any transfer expense like brokerage charges, registration charges on sale of property etc. then seller can also take the deduction of these expenses while calculating capital gain on sale of such property.

> If we have incurred any major expense then we can take it as Cost of improvement and if there is long term capital gain then also take it as indexed cost of improvement in the same manner as we discussed for indexed cost of acquisition.

Latest Changes Proposed in Property Taxation by Final Budget of 2024

There are major two changes proposed by our Honorable Finance Minister in Final Budget of 2024 which are as follows-:

> LTCG Tax reduced to 12.5% from 20%

> Benefit of Indexation is removed

Let’s understand the effect of above changes with the help of example-:

Suppose Mr. A purchased the property in 2001-02 for Rs 1,00,00,000 and sold the same in year 2024-25 for Rs 8,45,00,000. We have assumed this sales value based upto annual property growth of 9.3% as data published by Govt. of India.

Pre Budget Position

Sale Value – Rs 8,45,00,000

Cost of Acquisition- Rs 1,00,00,000

Indexed cost of acquisition- Rs 3,63,00,000 [1crore x 363]

100

Taxable Capital Gain – Rs 4,82,00,000 [ 8,45,00,000-3,63,00,000]

Tax Rate on sale of property – 20%

Amount of Tax payable as per section 112 –Rs 96,40,000 [ 4,82,00,000*20%]

Post Budget Position

Sale Value – Rs 8,45,00,000

Cost of Acquisition- Rs 1,00,00,000

Indexed cost of acquisition- Not Available

Taxable Capital Gain – Rs 7,45,00,000 [ 8,45,00,000-1,00,00,000]

Tax Rate on sale of property – 12.5%

Amount of Tax payable as per section 112 – Rs 93,12,500 [ 7,45,00,000*12.5%]

Lower tax payable post budget – Rs. 3,27,500 [96,40,000-93,12,500]

Conclusion

As we can see from above pre-post budget analysis that Taxpayer have to pay lower tax of Rs 3,27,500 on sale of property. Even if the LTCG on sale of property is reduced to 12.5% from 20% but on the other side indexation benefit is removed which was very necessary in prospective of inflation rate. As we have discussed earlier that inflation is increasing day by day in developing country like India therefore Govt. gave the benefit of indexation earlier. However, now Govt. proposed to remove the benefit of indexation w.e.f. 23rd July, 2024. It is true that it will increase/ decrease the Govt. tax collection in case to case basis. But it would also result in increase in amount of tax on sale of property in short term like 5-10 years which can also lead to increase in black money in real estate sector. There is already huge amount of black money involved in real estate sector but after this change there is increase in black money in real estate sector.

Author Bio

sir, if an assessee sold a property in June 2024, can he take the method that is beneficial to him?