Impairment testing of non-financial assets is a difficult and time-consuming task; the input required for calculation of value-in-use requires the preparer of financial statements to make accounting judgments and estimates; the input, such as future cash flows, discount rates, terminal values, and so on, is based on data points collected from various departments of the entity, and several data points are market driven. In this article, we attempt to explain one such input, namely the discount rate to be used for discounting future cash flows generated by an asset subject to impairment testing in order to determine its value-in-use. We also attempt to answer the three questions/ambiguities that arise while selecting the discount rate.

1. Out of the three rates mentioned in standard which is the most appropriate rate to be selected?

2. What weights should be used to calculate the WACC of the entity? Especially when the entity has a dynamic capital structure that is subject to change in the future.

3. How should the pre-tax WACC be calculated?

Ind AS 36/IAS 36 require entities to measure value in use for assets subject to impairment testing by discounting future cash flows to their present value. The standard provides three discount rate options and specifies that the rate be pre-tax. The following are the standard’s guidance

As per para 55 of Ind AS 36/IAS 36

The discount rate (rates) shall be a pre-tax rate (rates) that reflect(s) current market assessments of:

(a) the time value of money; and

(b) the risks specific to the asset for which the future cash flow estimates have not been adjusted

As per para A17 to A19 of Appendix A of Ind AS 36/IAS 36

A17 As a starting point in making such an estimate, the entity might take into account the following rates:

(a) the entity’s weighted average cost of capital determined using techniques such as the Capital Asset Pricing Model;

(b) the entity’s incremental borrowing rate; and

(c) other market borrowing rates.

A18 However, these rates must be adjusted: (a) to reflect the way that the market would assess the specific risks associated with the asset’s estimated cash flows; and

(b) to exclude risks that are not relevant to the asset’s estimated cash flows or for which the estimated cash flows have been adjusted. Consideration should be given to risks such as country risk, currency risk and price risk.

A19 The discount rate is independent of the entity’s capital structure and the way the entity financed the purchase of the asset, because the future cash flows expected to arise from an asset do not depend on the way in which the entity financed the purchase of the asset

Out of the three rates mentioned in standard which is the most appropriate rate to be selected?

Although the standards provide three options, the weighted average cost of capital (WACC) is a widely used and accepted rate for discounting future cash flows. There is a good research paper titled The Discount Rate: A Note on IAS 36 by Sven Husmann, Martin Schmidt, and Thorsten Seidel on p.20061, which calculates and compares the value in use using all three alternatives and made a conclusion that how the WACC is most appropriate rate for discounting and how other two alternatives can show widely different result based upon the entity leverage.

Formula of WACC

WACC: wd * rd (1 – t) + we * re

Where:

w = weights d = debt e = equity r = cost (aka required rate of return) t = tax rate

What weights should be used to calculate the entity’s WACC?

The weights will be determined using the debt-to-equity ratio as of the date the value in use is calculated. The reference in para A19 of Appendix A of Ind AS 36/IAS 36 about The discount rate is independent of the entity’s capital structure is made with respect to Modigliani Miller’s2 widely accepted and time proven WACC theorem, which states that a firm’s market value is independent of its capital structure (its leverage): A leveraged entity’s market value equals the value of an unleveraged entity. In simple terms, even if an entity has a dynamic capital structure that will change in the future, according to the theorem, any change in the weight of debt and equity will be completely offset by the return of debt and equity.

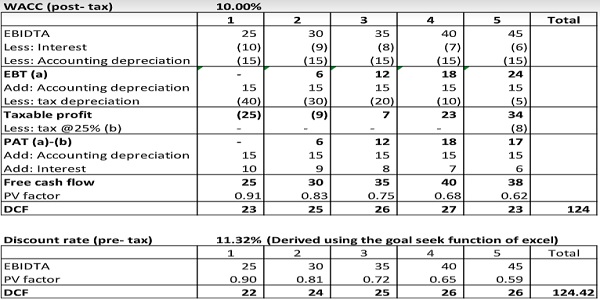

How should the pre-tax WACC be calculated?

Because of differences in depreciation rate and method, tax holidays, special allowances and disallowances, and other factors, an entity’s effective tax rate may differ from its nominal tax rate, and hence the pre-tax WACC is the rate that results;

(a) the present value of future cash flow excluding tax pay-outs;

equal the sum of

(b) the present value of future cash flow including tax pay-outs calculated using post tax WACC.

Illustrative example

For practical purposes, the following pre-tax WACC formula may be used, but it will not provide an accurate picture if the taxable profit and accounting profit are widely mismatched.

WACC pre-tax: wd * rd + we * re/ (1 – t)

Where:

w = weights d = debt e = equity r = cost (aka required rate of return) t = tax rate

References

1. <https://www.researchgate.net/publication/233224874_The_Discount_Rate_A_Note_on_IAS_36>

2. <https://en.wikipedia.org/wiki/Modigliani%E2%80%93Miller_theorem>