An entity shall classify financial assets as subsequently measured at amortized cost, fair value through other comprehensive income or fair value through profit & loss on the basis of both:

(a) The entity’s business model* for managing the financial assets and

(b) The contractual cash flow** characteristics of the financial asset.

*An entity’s business model refers to how an entity manages its financial asset in order to generate cash flows. IND AS 109 prescribes two business models: holding financial assets to collect contractual cash flows; and holding financial assets to collect contractual cash flows and selling. FVTPL is the residual category which is used for financial assets that are held for trading or if a financial asset does not fall in one of the two prescribed business models.

**Contractual Cash Flow = Principal + Interest on principal amount outstanding^^

^^Interest on principal amount outstanding = Time value of money (+) Credit Risk (+) Liquidity Risk (+) Cost associated with holding of financial instrument (+) profit margin

Para 1 – A financial asset shall be measured at amortized cost if both of the following conditions are met:

(a) The financial asset is held within a business model whose objective is to hold financial assets in order to collect contractual cash flows and

(b) The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

Para 2 – A financial asset shall be measured at fair value through other comprehensive income if both of the following conditions are met:

(a) The financial asset is held within a business model whose objective is achieved by both collecting contractual cash flows and selling financial assets and

(b) The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding.

For the purpose of applying para 1 & 2:

(a) Principal is the fair value of the financial asset at initial recognition.

(b) Interest consist of consideration for the time value of money, for the credit risk associated with the principal amount outstanding during a particular period of time and for the other basic landing risk and costs, as well as a profit margin.

Para 3 – A financial asset shall be measured at fair value through profit & loss unless it is measured at amortized cost in accordance with para 1 or at fair value through other comprehensive income in accordance with para 2. However, an entity may make an irrevocable election at initial recognition for particular investments in equity instruments that would otherwise be measured at fair value through profit & loss to present subsequent changes in fair value in other comprehensive income.

Option to designate a financial asset at fair value through profit & loss

Despite para 1, 2 & 3, an entity may, at initial recognition, irrevocably designate a financial asset as measured at fair value through profit & loss if doing so eliminates or significantly reduces a measurement or recognition inconsistency (sometimes referred to as an ‘accounting mismatch’) that would otherwise arise from measuring assets or liabilities or recognizing gains and losses on them on different basis.

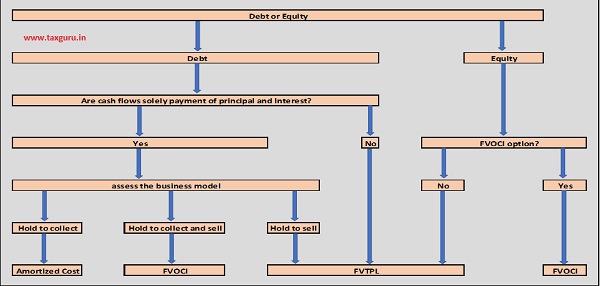

The below chart provides an overview of the classification requirements for financial assets

Illustration on Classification of Financial Assets

Alpha co. has entered into the following transactions involving financial instruments:

(a) Alpha gave loan to Beta during the year. Although Beta owns Alpha money, this transaction does not give rise to trade receivables. It is part of a portfolio that the company manages in order to collect the contractual cash flows.

Solution – this would be classified as “at amortized cost”.

(b) Alpha made an investment in 500 equity shares at Rs.10 per share to Lamda which are not held for trading, do not have a quoted price and their fair value cannot be reliably measured.

Solution – The equity investment in Lamda is classified as at fair value, since there cannot be any contractual cash flows towards principal and interest and hence amortised cost method cannot be used. The subsequent changes in fair value will be recognized in profit & loss unless an irrevocable election to classify them as fair value through OCI is made.

(c) Alpha made an investment of 200 equity shares at Rs.12 per share of Gamma quoted in an active market. However, this investment was not made or held for trading purpose.

Solution – The equity investment in Gamma is classified at fair value. According to IND AS 109, all investments in equity instruments and contracts on those instruments must be measured at fair value which would be determined by applying appropriate valuation technique.

(d) During the year, Alpha made a strategic investment in an equity instrument which the company, at the moment, has no intention of selling.

Solution – Unless Alpha decides to classify the strategic investment as a financial asset held at fair value through profit or loss, the investment should be classified as at fair value through OCI, through an irrevocable selection.

(e) Alpha has invested in debt securities, which are not quoted in an active market and are not held for trading.

Solution – The investment in debt securities should be classified as at amortized cost since it appears that the business model is to hold the assets to collect contractual cash flows of principal and interest.

(f) During the year, Alpha purchased debt securities of XYZ Ltd. These debt instruments are quoted in an active market and Alpha plans on holding on to them until maturity. However, if market interest rates fall significantly, Alpha will consider selling the debt securities to realize the associated gain.

Solution – In accordance with IND AS 109, if an entity holds investments to collect their contractual cash flows but would sell an investment in particular circumstances, the objective of an entity’s business model may still be to hold financial assets to collect the contractual cash flows. Hence this item should be classified as “at amortized cost”.

(g) During the year Alpha made another investment in Gamma, which was held for trading purposes.

Solution – The second investment in Gamma would be classified as a financial asset at fair value through profit or loss.

Classification of Financial Liabilities

Para 4 – An entity shall classify all financial liabilities as subsequently measured at amortized cost, except for:

(a) Financial liabilities at fair value through profit & loss. Such liabilities, including derivatives that are liabilities, shall be subsequently measured at fair value.

(b) Financial liabilities that arise when a transfer of asset does not qualify for derecognition* or when the continuing involvement approach applies.

*If a transfer does not result in derecognition because the entity has retained substantially all the risk and rewards of ownership of the transferred asset, the entity shall continue to recognize the transferred asset in its entirety and shall recognize a financial liability for the consideration received.

(c) Financial guarantee contracts*. After initial recognition, an issuer of such a contract shall subsequently measured it at higher of:

(i) The amount of loss allowance determined in accordance with Impairment – Expected Credit Loss (Para 5.5 of Ind AS 109) and

(ii) The amount initially recognized less, when appropriate, the cumulative amount of income recognized in accordance with the principals of IND AS 115 (Revenue from contracts with customers).

*As per IND AS 109, Financial Guarantee contract means “A contract that requires the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payment when due in accordance with the original or modified terms of a debt instrument”.

(d) Commitments to provide a loan at a below market interest rate. An issuer of such a commitment shall subsequently measure it at the higher of:

(i) The amount of loss allowance determined in accordance with Impairment – Expected Credit Loss (Para 5.5 of Ind AS 109) and

(ii) The amount initially recognized less, when appropriate, the cumulative amount of income recognized in accordance with the principals of IND AS 115 (Revenue from contracts with customers).

(e) Contingent consideration recognized by an acquirer in a business combination to which to which IND AS 103 (Business Combination) applies. Such contingent considerations shall be measured at fair value with changes recognized in profit & loss.

Illustration on Classification of Financial Assets

Measurement of Financial Liability through amortized cost.

Alpha Ltd. borrows Rs.10 Lakhs from Beta Ltd. under the following terms:

(a) The loan will carry 5% annual rate of interest, payable at the end of each year.

(b) Alpha Ltd. will make immediate payment of an origination fees of Rs.70,000 to Beta Ltd.

(c) The principal will be repaid in two installments, Rs.4 Lakhs at the end of year 3 and Rs.6 Lakhs at the end of year 5.

Show the loan account in the books of Alpha Ltd.

Solution –

Fair value of the loan given = Rs.10 Lakhs

Transaction Cost = Origination Fee = Rs.0.7 Lakhs

Fair Value, net of transaction cost = Rs.9.30 Lakhs

Effective interest rate is the discount rate at which present value of interest and principal payments over 5 years is equivalent to Rs.9.30 Lakhs. The rate is ascertained by trial and error method in the absence of having been given in the problem.

Present Value @6%

| Year | Cash flow Rs.’000 | DCF@6% | Present Value Rs.’000 |

| 1 | 50 | 0.943 | 47 |

| 2 | 50 | 0.890 | 44 |

| 3 | 450 | 0.839 | 378 |

| 4 | 30 | 0.792 | 24 |

| 5 | 630 | 0.747 | 471 |

| 964 |

Present Value @8%

| Year | Cash flow Rs.’000 | DCF@6% | Present Value Rs.’000 |

| 1 | 50 | 0.926 | 46 |

| 2 | 50 | 0.857 | 43 |

| 3 | 450 | 0.794 | 357 |

| 4 | 30 | 0.735 | 22 |

| 5 | 630 | 0.680 | 429 |

| 897 |

By interpolation the effective rate of interest would be

=6% + (8-6) / (964-897) X (964-930)

=7%

Statement of computation of interest cost (Rs.’000)

| Year | Amortised Cost (Opening) | Interest @7% | Cash Paid | Amortised Cost (Closing) |

| 1 | 930 | 65 | 50 | 945 |

| 2 | 945 | 66 | 50 | 961 |

| 3 | 961 | 67 | 450 | 578 |

| 4 | 578 | 41 | 30 | 589 |

| 5 | 589 | 41 | 630 | Nil |

In the books of Alpha Ltd.

Loan A/c

| Year | Particulars | Rs.’000 | Year | Particulars | Rs.’000 |

| 1 | To Bank

To Bank To Balance c/d |

70

50 945 |

1 | By Bank

By Interest |

1000

65 |

| 1065 | 1065 | ||||

| 2 | To Bank

To Balance c/d |

50

961 |

2 | By Balance b/f

By Interest |

945

66 |

| 1011 | 1011 | ||||

| 3 | To Bank

To Bank To Balance c/d |

50

400 578 |

3 | By Balance b/f

By Interest |

961

67 |

| 1028 | 1028 | ||||

| 4 | To Bank

To Balance c/d |

30

589 |

4 | By Balance b/f

By Interest |

578

41 |

| 619 | 619 | ||||

| 5 | To Bank | 630 | 5 | By Balance b/f

By Interest |

1000

65 |

| 630 | 630 |

Author Bio