CA, CS, CMA

Log in to FollowInformation related to to CA, CS, CMA, ICAI, ICSI, Exam, CAG, MEF, Audit Empanelment, Accounting Standard, IFRS, Auditing Standard, Accounting Principles.

CS Executive & Professional Programme Examination- Instructions- June 2022

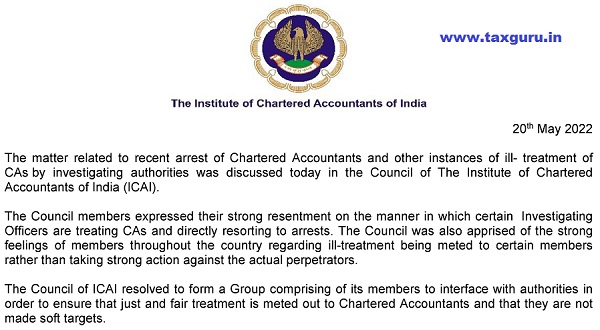

ICAI decisions on ill- treatment of CAs by GST investigating authorities

Empanelment of Maharashtra CA Firms with MAHAFPC

IND AS 40 Investment Property – from perspective of Real Estate Company

How to Choose between CA Or CS?

Disclosure of Compounded Financial Instrument as per IND As 109

Every Day is Holiday! How?

Update all pending UDINs at e-filing portal immediately: ICAI

Treatment of the Expesnes of Non-Operative Mines/Plants

MCA notifies applicability of Several provisions of CA, CMA & CS Amendment Act

रांची केस में सीए की हिरासत सिखलाती कि हर पैशेवर के लिए संस्थान द्वारा जारी आचार संहिता का पालन बेहद जरुरी

Relax time period for Resubmission of forms in LLP V3 modules – ICSI requests

Check CAG Provisional empanelment status

Regulatory updates for the Month of April 2022

Latest ICAI , ICSI, CMA News

Chartered Accountants or Company Secretaries , Cost Accountants are a group of extraordinary people. Wherever they go, they bring difference. They’re talented, ambitious and are in demand. If you are thinking about a career which offers respect, prestige, great financial rewards, and better prospects becoming a Chartered Accountant, Cost Accountnat or a Company Secretary is a perfect way to start. For becoming a CA, CMA or a CS you need to qualify the CA exam, CMA exam and the CS exam respectively. The CA, CMA and CS qualifications are exceptional prestigious and internationally respected which would offer you the skills, knowledge, and values to be a sought after business professional. The CA, CMA and CS qualifications comprises of relevant professional study and practical experience.

The ICAI (Institute of Chartered Accountants of India) is the empowering body for Chartered Accountants in India, The ICAI (The Institute of Chartered Accountants of India ) for Cost Accountantgs in India and the ICSI (Institute of Companies Secretaries of India) is the regulating body of Company Secretaries in India.

At Taxguru, we provide you with all the latest updates and announcement with respect to CA exam, CMA Exam and CS exam. Find all the latest news on ICAI and all the relevant updates related to CPT exam, IPCC and Finals. Get to know what’s new and what trending in the world of CS, CMA with all the latest news on ICSI, CMA here at Taxguru.

At Taxguru, we publish blogs and articles at regular intervals for the enlightenment of our readers who are pursuing CA, CMA or CS or have completed the esteemed professional course. We ensure that we bring you all the latest insights and guidance in your journey towards your goal to achieve success in CA, CMA and CS exams. We keep you posted on all important and significant ICAI news and ICSI news and ensure to keep updated with the trending information from the world of these profound professions.