Senior Citizens are the Individuals for whom various tax benefits are provided under the Income-tax Act which we are going to discuss in this Article which may be beneficials for a large number of taxpayers who are not aware of these provisions.

As per Income-tax Act, Senior Citizen means an Individual who has attained the age of 60 years or more during the previous year / financial year.

Further, as per the Circular No. 28/2016 dated July 27, 2016 issued by Central Board of Direct Taxes, a person born on April 1st would be considered to have attained a particular age on March 31st, the day preceding the anniversary of his birthday. Therefore, if an Individual has a birthday anniversary on April 1st 2025 and attain the age of 60 years on that, he will be considered as of 60 years of age as on March 31st 2025 (previous day). You can take the tax benefits of senior citizen for FY 2024-25 itself. Similar provisions shall applicable to Very Senior Citizens (80 years or above).

1. Tax Slab Rates applicable to a Senior Citizen and Very Senior Citizen

Under the Old Tax Regime, following are the tax slab rates applicable to a Resident Senior Citizen:

| Level of Income (INR) | Tax Rate |

| Upto INR 3 lakhs | NIL |

| INR 3 lakhs to INR 5 lakhs | 5% |

| INR 5 lakhs to INR 10 lakhs | 20% |

| More than INR 10 lakhs | 30% |

Under the Old Tax Regime, following are the tax slab rates applicable to a Resident Very Senior Citizen:

| Level of Income (INR) | Tax Rate |

| Upto INR 5 lakhs | NIL |

| INR 5 lakhs to INR 10 lakhs | 20% |

| More than INR 10 lakhs | 30% |

Under the Old Tax Regime, following are the tax slab rates applicable to a Non-Resident Senior Citizen / Very Senior Citizen:

| Level of Income (INR) | Tax Rate |

| Upto INR 2.50 lakhs | NIL |

| INR 2.50 lakhs to INR 5 lakhs | 5% |

| INR 5 lakhs to INR 10 lakhs | 20% |

| More than INR 10 lakhs | 30% |

Under the New Tax Regime, following are the tax slab rates applicable to a Senior Citizen (Resident / Non-Resident) for Financial Year (FY) 2024-25 (April 1, 2024 to March 31, 2025):

| Level of Income (INR) | Tax Rate |

| Upto INR 3 lakhs | NIL |

| INR 3 lakhs to INR 7 lakhs | 5% |

| INR 7 lakhs to INR 10 lakhs | 10% |

| INR 10 lakhs to INR 12 lakhs | 15% |

| INR 12 lakhs to INR 15 lakhs | 20% |

| More than INR 15 lakhs | 30% |

Under the New Tax Regime, following are the tax slab rates applicable to a Senior Citizen for FY 2025-26 (As per Budget 2025 Proposals):

| Level of Income (INR) | Tax Rate |

| Upto INR 4 lakhs | NIL |

| INR 4 lakhs to INR 8 lakhs | 5% |

| INR 8 lakhs to INR 12 lakhs | 10% |

| INR 12 lakhs to INR 16 lakhs | 15% |

| INR 16 lakhs to INR 20 lakhs | 20% |

| INR 20 lakhs to INR 24 lakhs | 25% |

| More than INR 24 lakhs | 30% |

2. Exemption from Payment of Advance Tax

- Advance Tax is required to be paid during the financial year in 4 instalments if your net estimated tax liability after reducing TDS, TCS withheld exceeds INR 10,000.

- In case you have not paid Advance Tax or short paid, you are liable to pay interest @ 1% per month for the shortfall under section 234B & 234C of the Income-tax Act at the time of filing of the Income-Tax Return.

- Further, the provisions relating to payment of Advance Tax are not applicable (even though net estimated tax liability exceeds INR 10,000) to a Resident Individual having age of 60 years or more and does not have any income chargeable under the head “Profit and Gains of Business or Profession”.

3. Exemption from filing of Income-Tax Return (Section 194P of the Income-tax Act)

- In case of an Individual, being a resident of India who is of the age of 75 years or above at any time during the previous year, who is having income of the nature of pension and no other income except the interest income from any account maintained by such Individual in the same bank in which he is receiving pension.

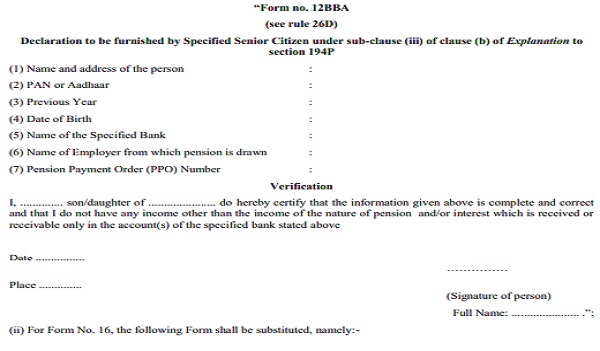

- Further, such Individual has furnished a declaration in Form 12BBA (under Rule 26D of the Income-tax Rules) in paper form to the bank containing the relevant details like Name, Address, Permanent Account Number (PAN), Previous Year, Date of Birth, Name of the Specified Bank, Name of Employer from which pension is drawn and Pension Payment Order (PPO) Number.

- The format of Form 12BBA is provided below:

- After providing the above details, the bank after giving effect to the deduction allowable under Chapter VI-A and rebate allowable under section 87A, compute the total income of such Individual for the relevant assessment year and deduct income-tax on such total income on the basis of the rates in force.

- Further, the provisions of section 139 shall not apply to a specified senior citizen for the assessment year relevant to the previous year in which the tax has been deducted.

4. Declaration in Form 15H

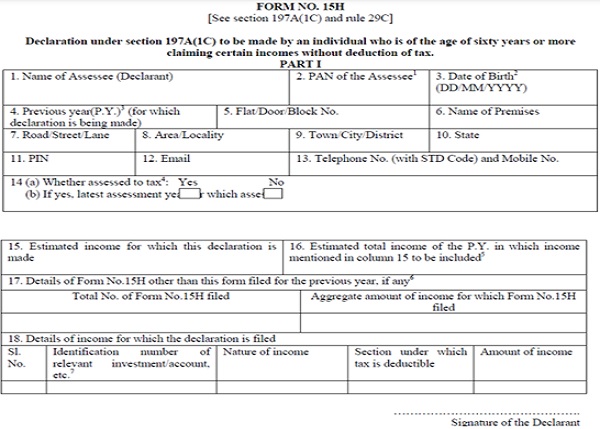

- As per section 197A(1C) of the Income-tax Act, in case of any Individual being a resident of India and is of the age of 60 years or more and the tax on his estimated total income of the previous year is NIL is required to provide declaration in Form 15H that the tax on his estimated total income of the previous year in which such income is to be included in computing his total income will be NIL.

- The declaration needs to be provided to the deductor responsible for making payment under section 192A (Payment of accumulated balance due to an employee from Provident Fund), section 193 (Interest on Securities), section 194 (Dividends), section 194A (Interest other than “Interest on securities”), section 194D (Insurance commission), section 194DA (Payment in respect of life insurance policy), section 194EE (Payments in respect of deposits under National Savings Scheme, etc.), section 194-I (Rent) or section 194K (Income in respect of units).

- Format of Form 15H provided below:

5. Reverse Mortgage Scheme

- As per section 10(43) of the Income-tax Act, any amount received by an individual as a loan, either in lump sum or in instalment, in a transaction of reverse mortgage referred in section 47(xvi) in relation to transfer of a capital asset in a transaction of reverse mortgage under a scheme notified by the Government.

- Further, Reverse Mortgage Scheme, 2008 (“Scheme”) was notified by Central Government vide Notification No. 93/2008 dated September 30, 2008.

- Under the scheme, a capital asset is mortgage by a person who is of the age of 60 years or more or any married couple, if either of the husband or wife who is of the age of 60 year or above against a loan obtained by him from approved lending institution.

- Further, under the scheme, reverse mortgage transaction occurs under which the loan may be disbursed to reverse mortgagor (person who has mortgaged his property) but does not include transaction of sale, or disposal, of the property for settlement of the loan except at the time of foreclosure of the loan agreement.

- Further, under the scheme, the approved lending institution may disburse the loan:

(a) to the reverse mortgagor by any one or more of the following modes, namely:

(i) periodic payments to be decided mutually between the approved lending institution and the reverse mortgagor;

(ii) lump-sum payment in one or more tranches, to the extent that the aggregate of the amount disbursed as lump sum payments does not exceed fifty per cent of the total loan amount sanctioned; or

(b) in part or in full, to the annuity sourcing institution for the purposes of periodic payments by way of annuity to the reverse mortgagor.

6. Deduction in respect of Health Insurance Premium (Section 80D)

- Under section 80D, where health insurance premium is paid by the taxpayer for himself and the taxpayer is an Individual resident in India who is of the age of 60 years or more at any time during the previous year, he is eligible to claim deduction of INR 50,000 under the Old Tax Regime.

- Further, under section 80D, where health insurance premium is paid by the taxpayer for parents who resident in India who is of the age of 60 years or more at any time during the previous year, he is eligible to claim additional deduction of INR 50,000 under the Old Tax Regime.

7. Deduction in respect of maintenance including medical treatment of a dependent who is a person with disability (Section 80DD)

- Where an assessee being an Individual or Hindu Undivided Family (HUF) who is a resident of India incur any expenditure for the medical treatment (including nursing), training and rehabilitation of a dependant, being a person with disability; or paid or deposited any amount under a scheme framed in this behalf by the Life Insurance Corporation or any other insurer or the Administrator or the specified company subject to the conditions specified and approved by the Board in this behalf for the maintenance of a dependant, being a person with disability.

- Further, dependent means in the case of an individual, the spouse, children, parents, brothers and sisters of the individual or any of them and in case of HUF, a member of HUF. Therefore, if parents are of 60 years or above and the assessee has incurred medical treatment expenditure on them, he is eligible to claim deduction under section 80DD.

- Further the amount of deduction is INR 75,000 and the amount of deduction increases to INR 1,00,000 for severe disability.

8. Deduction in respect of medical treatment etc (Section 80DDB)

- Where an assessee who is a resident of India has actually paid any amount for the medical treatment of such disease or ailment as specified for himself or a dependant, in case the assessee is an individual or for any member of a HUF, in case the assessee is an HUF.

- Further, dependent means in the case of an individual, the spouse, children, parents, brothers and sisters of the individual or any of them and in case of HUF, a member of HUF dependant wholly or mainly on such individual or HUF for his support and maintenance.

- Further, the amount of deduction shall be lower of amount actually paid of INR 40,000 and in case of a senior citizen being an Individual resident in India who is of the age of 60 years or more at any time during the relevant previous year, the INR 40,000 limit increases to INR 1,00,000.

9. Deduction in respect of interest on deposits in case of Senior Citizens (Section 80TTB)

- Where the gross total income of a senior citizen (an individual resident in India who is of the age of 60 years or more at any time during the relevant previous year), includes any income by way of interest on deposits with Bank, Co-operative Society engaged in the business of banking and a post office, deduction of lower of interest received or INR 50,000 is allowed as deduction under section 80TTB under the Old Tax Regime.

10. TDS on interest other than interest on securities (Section 194A)

- Any person responsible for paying to a resident any income by way of interest other than income by way of interest on securities, shall at the time of credit of such income to the account of payee or at the time of payment thereof, deduct TDS under section 194A on such interest at the rate of 10% if it exceeds INR 40,000 during the financial year.

- In case of senior citizen (an individual resident in India who is of the age of 60 years or more at any time during the relevant previous year), the limit of INR 40,000 increases to INR 50,000 and this limit is proposed to be increased to INR 1,00,000 by Budget 2025.

*****

Author can be reach out for any queries at email ID – canavneetsingh1@gmail.com

Disclaimer: This article serves an educational purpose and should not be considered as professional advice. Consultation with a qualified individual is recommended before making any decisions based on the content provided. The author bears no responsibility for any actions taken based on this article.

Author Bio

I am 75+ yrs of age. I have pension acct and three FDs in one bank and in another bank I have only a SB acct. From which bank I can avail the benefit of not filing ITR under sec. 194P.

You can file the declaration with the bank from where you are receiving the pension and interest on fixed deposit.

I am 74years,having pension, bank interest, and capital gains of 200000/-by selling two mutual fund units. Am I liable to pay advance tax for the AY 2025-26?

In your case, if you also qualify as Resident of India for the particular financial year, then you are not liable for payment of Advance Tax.

wonderful article for all senior citizens . Adequate advice obtained.

regards and sincere thanks

vinod Kumar Shukla,

Bhopal

Thank you for your kind words and appreciation.