Learn how to report Long Term Capital Gain (LTCG) on the sale of land and buildings in ITR 2. Follow the step-by-step procedure, complete with illustrations and screenshots, for a hassle-free filing experience. Understand the new ITR forms, filing dates, and more.

1. Income Tax Return filing date is approaching fast. The last date to file ITR 2 for the financial year 2022-23 is 31st July 2023. ITR 2 form is available for individuals and HUFs who have income from various avenues like capital gains from one or more properties, rental income, or income from other sources. Salaried employees having capital gain income can also file ITR 2.

2. CBDT (Central Board of Direct Taxes) has notified the new ITR forms for AY 2023-24 The online filing of ITR 2 is enabled on the portal: https://www.incometax.gov.in

3. This article covers the step-by-step procedure to report Long Term Capital Gain on the sale of Land & Buildings in ITR 2. An attempt has been made to simplify the procedure of filing ITR 2 with the help of Illustrations & Screenshots.

4. Illustration: Mr. Arindam transferred a residential property on 25th March 2023. The said property was purchased in 1998. The relevant details are as indicated below:

| Sl. | Particulars | Amount (Rs.) |

| (a) | Sale Consideration | 50,00,000 |

| (b) | Cost of Acquisition (Fair Market Value as on 01.4.2001) | 4,00,000 |

| (c) | Cost of improvement | 50,000 |

| (d) | Investment in specified Bonds (Sec 54EC) | 10,00,000 |

| (e) | Investment in Purchase of Residential property (Deduction u/s 54) | 20,00,000 |

| (f) | Income from Salary | 3,00,000 |

| (g) | Income from Dividend | 19,060 |

Step-by-Step Procedure to report the LTCG in ITR 2

(a) Login to www.incometax.gov.in

(b) The path is: – e-file>Income Tax Return > File Income Tax Return. Select AY 2021-22(Current AY) > online. Start New Filing> Individual> Select ITR Form > ITR 2> Let’s Get Started. Tick the reason for filing Tax. Taxable income is more than the basic exemption limit.

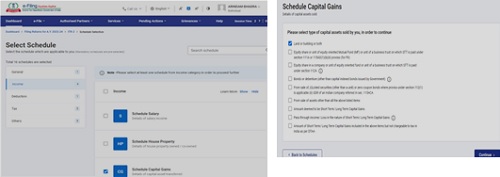

(c) Select Schedule Capital Gain (CG) & select the type of capital assets sold as “Land and building or both”.

(d) Click on Add details and enter the date of purchase & sale of the property.

(d) Enter the details i.e., Sale consideration, Cost of acquisition & Cost of improvement, if any. The system will automatically calculate the indexed cost of acquisition/improvement.

Please note – In case, the stamp duty value is more than 110% of the consideration value, the stamp duty value will be taken as sale consideration and capital gain tax will be calculated accordingly. (Refer to a (ii) & a (iii) above.)

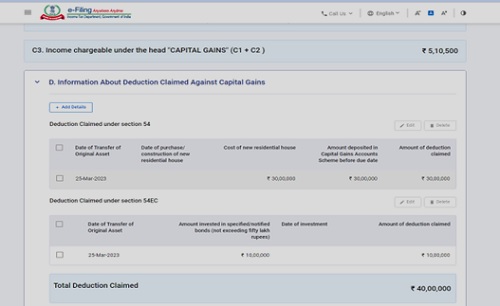

(e) Table D – Information about Deduction claimed against Capital Gain: Enter the details of amount incurred towards the purchase of new residential property or/and the amount invested in specified Bonds:-

(f) Table E – Set off Current Year Capital Losses with Current Year Capital Gains: This section will display the set off of current Capital losses with current Capital gain, if any. In our illustration, there are no capital losses in the current year.

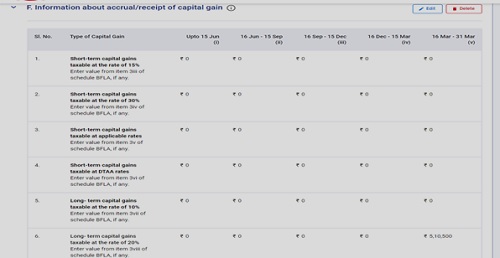

(g) Table F- Information about accrual/receipt of Capital gain: Enter the Capital Gain amount in the respective quarter in which the transfer took place.

(h) Click “confirm” in Schedule CYLA, BFLA, and CFL & Schedule Special Income. No details are required to be entered in these schedules. The details will be auto populated from the Capital Gain Schedule.

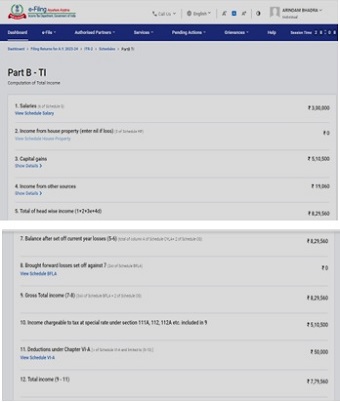

Computation of Total Income- Schedule TI: The computation of total income auto-populated from all the schedules can be viewed in this section.

6.1 Illustration: Mr. Arindam has entered the income details in the relevant schedules. The computation is auto-populated in Schedule TI.

| Sl | Particulars | Amt(Rs) |

| (a) | Income from Salary | 3,50,000 |

| (b) | Less: Standard Deduction | (50,000) |

| (c) | Taxable salary ( Schedule Salary) | 3,00,000 |

| (d) | Income from Capital gain ( Schedule SG) | 5,10,500 |

| (e) | Income from dividend ( Schedule OS) | 19,060 |

| (f) | Gross Total Income( c+d+e) | 8,29,560 |

| (g) | Deduction under section 80C ( Schedule VIA) | (50,000) |

| (h) | Total Income ( f-g) | 7,79,560 |

7. Computation of Tax Liability -Schedule TTI- Part B: In this schedule, the overall computation of tax liability on total income can be viewed.

7.1 Illustration: The total tax liability of Mr. Arindam will be auto-computed by the system and the same can be viewed in schedule TTI-Part B.

| Sl. | Particulars | Amt(Rs.) |

| (a) | Total taxable Income | 7,79,560 |

| (b) | Tax on LTCG at a special rate (20% on 5,10,500) | 1,02,100 |

| (c) | Tax at a normal rate: 5% (269060-250000) | 953 |

| (d) | Total Tax Liability (b+c) | 1,0,3053 |

| (e) | Health & Education Cess @ 4% on d | 4,122 |

| (f) | Total Tax Liability (d+e) | 1,07,175 |

8. Once the necessary schedules are ‘Confirmed’, review Part B TTI and then tap on ‘Preview Return’. Download the ITR and proceed with the declaration.

9. The ITR 2 can also be prepared offline using an Excel utility and submitted online. Both options require the filing of ITR online on the e-filing portal. The only difference between both modes is preparing the ITR online vs offline through an Excel utility. For offline preparation of ITR, one needs to download the applicable ITR, fill out the form offline, save the generated JSON file, and then upload it.

*****

Disclaimer: The information provided is for general informational purposes only and should not be considered as legal, financial, or professional advice. I do not guarantee the completeness, accuracy, reliability, suitability, or availability of the article or its content. Any reliance you place on this information is strictly at your own risk. It is advisable to consult a qualified professional or seek specific advice based on your individual circumstances. I am not liable for any loss or damage resulting from the use of this article or reliance on the provided information.

The author can be approached at caanitabhadra@gmail.com

Author Bio

ADD-on (To Supplement/Dilate):

“2. CBDT (Central Board of Direct Taxes) has NOTIFIED THE NEW ITR forms for AY 2023-24 The online filing of ITR 2 is enabled on the portal: https://www.incometax.gov.in”

FONT (supplied)

In an attempt to locate the material changes if any, need to focus on :

1. STEP >

“(d) Enter the details i.e., Sale consideration, Cost of acquisition & Cost of improvement, if any. The system will automatically calculate the indexed cost of acquisition/improvement.”

Cost of acquisition with indexation

Cost of Improvement with indexation

COMMENT : Does that mean/imply that, it is now open to a tax payer , – if prudently chooses not to adopt FMV as of FY 2001-02 and consequently not to invite any dispute with the REVENUE , to claim the Original Cost of acquisition (ACTUAL) as indexed for the FY 2000-21 as per the old table and indexed for the FY 2001-22 to the date (FY) of transfer/sale as per the new table !?

2. “For calculation of capital gain on Land or building, the full value of consideration should be the minimum stamp duty value of such property. In case, the STAMPDUTY VALUE stamp duty is more than 110% of the CONSIDERATION VALUE consideration value, the stamp duty value WILL BE TAKEN AS sale consideration and capital gain tax will be calculated accordingly.”

COMMENT :There could conceivably be instances in which tax payer does either not accept but dispute for valid reasons , or is not in a position, to go by STAMP DUTY VALUE. In such cases, does the system permit taxpayer not to fill in the related columns in the tax return FORM ? If not, how then taxpayer has to otherwise take such a stand, not without due merits, as indicated ?!

Back / OVER to the author/ other experts in field practice, for sparing and sharing independent opinion for enlightenment / useful guidance !

The taxpayer can opt actual cost of acquisition or FMV as on 01.04.2001. Indexation will not be as per the old table but the new index table.

As per Act, if Stamp duty value is 110% of the actual consideration, stamp duty value will be taken as consideration. The option for not accepting the provision is not provided to the tax payer. However, if the taxpayer is not agreed with the stamp duty valuation, he can request Assessing Officer to get value from registered valuer.

The taxpayer has option to choose Fair Market Value as on 01.04.2001 or the actual cost of acquisition, whichever is higher. The higher cost of acquisition will reduce his capital gain tax liability

The two ‘replies’ of the author of the write -up , honestly speaking, do not seem to specifically cover/clarify any of the specific points raised through my comments.

For instance, whether or not , THE SYSTEM in place will permit a taxpayer to skip filling in the DATA pertaining to ‘stamp duty value’ but instead, in the column requiring ‘cost of acquisition’, permits filling in INDEXED COST ACQUISITION as of the year 2000-21 has to be tried in a given case; not answered off hand by surmise !? Any way, for enabling the writer to examine in depth the points of surroundng controversy, have sent to her e’mail ID a couple of LINKS (Articles) to go through !

“4. Illustration: Mr. Arindam transferred a residential property on 25th March 2023. The said property was purchased in 1998. The relevant details are as indicated below:

Sl. Particulars Amount (Rs.)

(a) Sale Consideration 50,00,000

(b) Cost of Acquisition (Fair Market Value as on 01.4.2001) 4,00,000

Read more at: https://taxguru.in/income-tax/itr-2-capital-gain-tax-sale-land-building.html

As regards the Item (b), according to a critical view, – as shared and reshared, a difficult question arises as to whether it will, at all, be prudent for taxpayer to choose and opt for claiming, based on an independent valuation, as FMV, if that be found to be higher than the ‘actual cost of acquisition’ / ‘indexed cost of acquisition’?!

ALERT: Suggest considering, by doing so, the inevitable possibility / consequence of getting into, otherwise avoidable, disputes/ long drawn litigation!?

courtesy