Case Law Details

PRPL Enterprises Private Limited Vs CIT (ITAT Mumbai)

Mumbai ITAT Allows 60% Depreciation on Computer Software and Restricts Section 14A Disallowance to Assessee’s Suo Motu Computation

The Mumbai ITAT held that computer software, including licensed application software such as SAP, AutoCAD, MS Office, Adobe Acrobat and similar software, is eligible for 60% depreciation under the entry “Computers including computer software” in Appendix I to the Income-tax Rules. The Tribunal rejected the Revenue’s view that independently purchased software constitutes an intangible asset entitled only to 25% depreciation under section 32(1)(ii). Relying on several High Court and Tribunal decisions, it held that computer software falls within the specific depreciation schedule applicable to computers and directed the Assessing Officer to allow depreciation at 60%.

On the issue of section 14A, the Tribunal found that the assessee had not earned any dividend income during the year and had earned only ₹3,952 as exempt share of profit from an LLP. It also noted that the Assessing Officer had computed an enormous disallowance of over ₹82.26 crore under Rule 8D despite the assessee having already made a suo motu disallowance of ₹9,11,435. Considering the facts, the Tribunal accepted the assessee’s voluntary disallowance and directed the Assessing Officer to restrict the disallowance under section 14A to ₹9,11,435. Further, following the Special Bench decision in Vireet Investment (P.) Ltd., it held that the section 14A disallowance cannot be added back while computing book profits under section 115JB. Consequently, the appeal was allowed.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

The captioned appeal is filed by the assessee, challenging the order of the Commissioner of Income Tax Appeals, National Faceless Appeal Centre (NFAC), Delhi [in short, “the Ld. CIT(A)”], dated 08.09.2025 for the Assessment Year (AY) 2015-16,arises from the assessment order under section 143(3) of the Income Tax Act, 1961 [in short, “the Act”] dated 26.12.2017, passed by Deputy Commissioner of Income Tax Circle-7(3)(2), Mumbai [in short, “the Ld.AO”]. The grounds of appeal raised by the assessee are as under:

“GROUND NO. I: DISALLOWANCE OF THE CLAIM OF DEPRECIATION ON ADDITIONS TO COMPUTER SOFTWARE OF RS 29.23,184/-:

1. On the facts and circumstances of the case and in law, the AO erred in recalculating depreciation on computer software @25% instead of @ 60% as claimed by the Appellant and thereby disallowed the excess depreciation on the alleged ground that software purchased separately and independent from computer purchases amounts to “intangible assets”.

2. He further erred in calculating the amount of depreciation ignoring the second proviso to section 32(1)(ii) of the Act and thereby making a higher addition to the total income.

3. The Appellant prays that the AO be directed to allow depreciation @60% on computer software as claimed by the Appellant and accordingly delete the disallowance made amounting to Rs. 29,23,184/-.

4. Without Prejudice to the above, the Appellant prays that the software purchased be allowed as business expenditure u/s 37(1) of the Act.

5. In any case, the amount of disallowance, if any, be restricted to Rs. 20,80,549/- as correctly computed as per the provisions of the Act.

GROUND NO. II: DISALLOWANCE AMOUNTING TO RS. 92,92,31,540/- U/S. 14A OF THE ACT READ WITH RULE 8D OF THE INCOME-TAX RULES, 1962 (“THE RULES”):

1. On the facts and circumstances of the case and in law, the AO erred in making a disallowance of Rs. 92,92,31,540/- u/s 14A of the Act r.w.r. 8D of the Rules including the suo moto disallowance made by the Appellant amounting to Rs. 9,11,435/-.

2. The AO failed to appreciate and ought to have held that:

a. No disallowance is called for where investments are made for strategic purpose;

b. The AO is duty bound to assess the correct income irrespective of the income returned by the Appellant;

c. Without prejudice to above, Application of Rule 8D of the Rules is not automatic;

d. Without prejudice to above, the investments made in debentures yielding taxable interest income should be excluded for the purpose of computing disallowance u/s 14A of the Act;

e. Without prejudice to above, only investments yielding exempt income should be considered while computing disallowance u/s 14A of the Act r.w.r. 8D of the Rules and thus current capital investment held in Limited Liability Partnership generating taxable interest income should not be considered.

f. Without prejudice to above, for computing disallowance u/s. 14A of the Act, net interest expenses after setting off against interest income is to be taken into consideration:

g. Without prejudice to above, only those investments which have yielded exempt income during the year should be considered while computing disallowance u/s 14A of the Act; and

h. Without prejudice to above, Disallowance u/s 14A of the Act should be restricted to the exempt income earned;

3. The Appellant prays that the disallowance u/s 14A of the Act r.w.r 8D of the Rules amounting to Rs. 92,92,31,540/-, including the suo moto disallowance made by the Appellant, be deleted or be appropriately reduced.

WITHOUT PREJUDICE TO GROUND NO. II.

GROUND NO. III: ADDITION OF DISALLOWANCE OF RS. 92,83,20,105/- UNDER SECTION 14A OF THE ACT R.W.R 8D OF THE RULES FOR THE PURPOSES COMPUTING BOOK PROFITS U/S 115JB OF THE ACT:

1. On the facts and in the circumstances of the case and in law, the AO erred in making the addition of the disallowances of Rs. 92,83,20,105/- made under section 14A of the Act r.w.r 8D of the Rules to the book profits computed u/s 115JB of the Act.

2. The Appellant prays that the AO be directed to delete the addition of disallowances u/s. 14A of the Act r.w.r 8D of the Rules while computation of book profits u/s 115JB of the Act.

GROUND NO. IV: RECOMPUTING THE LOSSES AND UNABSORBED DEPRECIATION TO BE CARRIED FORWARD:

1. Consequent to the above the Appellant prays that the AO be directed to re-compute the eligible losses and unabsorbed depreciation for the captioned year to be carried forward to subsequent years after set off.

2. The Appellant further prays that based on the outcome of the appeals filed in the respective years, the AO be directed to re-compute the eligible losses and unabsorbed depreciation brought forward from AY 2012-13 to AY 2014-15 to be set off in the captioned year and to be carried forward to the subsequent years.

GROUND NO. V: CHARGING INTEREST U/S, 234B AND 234C OF THE ACT:

1. On the facts and circumstances of the case and in law, the AO erred in levying interest amounting to Rs. 2,48,40,288/- and Rs. 16,46,944/- u/s 234B and 234C of the Act respectively.

2. The Appellant prays that the AO be directed to delete the levy of interest made u/s. 234B and 234C of the Act.”

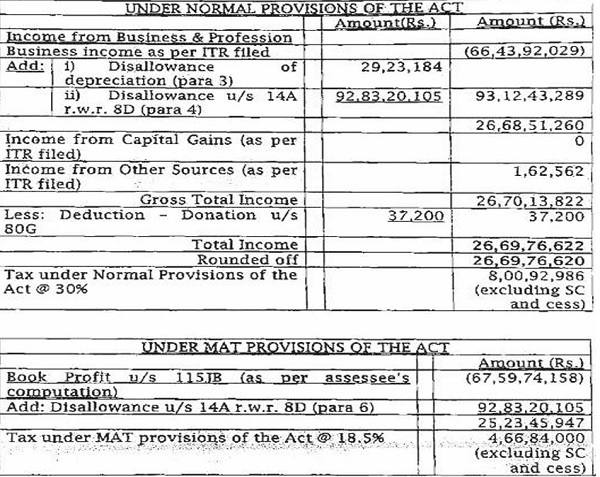

2. Briefly stated, the assessee is a company, engaged in the business of real estate/real estate development year was filed on 29.09.201 5, declaring total loss of Rs.65,07,56,00 of assessee was selected f r scrutiny and accordingly, notice u/s 12.04.2016 was issued. Further notice u/s 142(1) dated 29.02.201 questionnaire was issued. During the course of assessment proceedings, certain issues were raised by the Ld. AO which were responded by the assessee. However, the Ld. AO was not convinced with the submissions/clarification of the assessee, therefore, the Ld . AO had recomputed the return of income of the assessee by making certain disallowances. Accordingly, the assess d income of assessee has been recomputed as under:

3. Being aggrieved with the aforesaid disallowances, the assessee preferred an appeal before the Ld. CIT(A), who had discussed and deliberated on the issues, however being not convinced with the submission of assessee, Ld. CIT(A) had dismissed assessee’s grounds of appeal, the assessee, therefore, is in appeal before us.

4. AT the outset, Ld. AR of the assessee submitted that the disallowances made by the Ld. AO regarding assessee’s claim for depreciation and the disallowance u/s 14A are not in accordance with the provisions of Act or settled principles under the jurisprudence of Hon’ble Courts. Therefore, both the disallowances are subject to reversal and otherwise the expenditure for purchase of software is allowable as business expenditure u/s 37(1) of the Act.

5. Per contra, Ld. DR representing the revenue vehemently supported the orders of Revenue Authorities and requested to uphold the same.

6. We have considered the rival submissions, perused the material available on record and jurisprudence relied upon by the assessee. Our adjudication towards the grounds of assessee’s appeal are as under:

7. Ground No. I -Disallowance of claim of depreciation on addition to computer software of Rs.20,80,548/- :

While making the aforesaid disallowance, the Ld. AO has observed that the assessee has made additions on account of computer software purchase during the year, under the head intangible assets with sub-head computer software for Rs.83,51,955/-. Ld. AO referred to the provisions of section 32 once again and has mentioned that it is an established fact that software is a depreciable and intangible asset, which is entitled for depreciation at the rate of 25% under part B of Depreciation Schedule in Appendix I of the Income Tax Rules. However, the assessee has claimed depreciation at the rate of 60% instead of 25%. Accordingly, the claim of deduction has been reduced from Rs.50,11,173/-instead of 20,87,989/- and the excess depreciation claimed by the assessee for Rs.29,23,184/- is added back to the total income of assessee.

8. When the issue was carried before Ld. CIT(A), the assessee submitted that the software purchase is covered by Appendix I, Part A Item III (5) which prescribes 60% for “Computer including computer software”, therefore, the assessee shall be allowed 60% depreciation instead of 25%. Ld. CIT(A) observed that the software purchase cannot be the integral part of any computer system, therefore, the Ld. AO had rightly restricted the depreciation to 25% as such software is covered within the ambit of “Business or Commercial Rights” u/s 32(1)(ii). Further, the assessee had itself capitalized the software under the head intangible asset, therefore the Ld. AO has rightly made the disallowance of Rs.29,23,184/- and the same is, therefore, sustainable.

9. On the aforesaid issue, the assessee is in appeal against the decision of Ld. CIT(A) in sustaining the disallowance made by the Ld. AO, whereas the Ld. CIT DR supports the impugned order passed by Ld. CIT(A).

10. It is appraised, at the outset that the aforesaid addition was subsequently reduced to Rs.20,80,548/- vide rectification order u/s 154 dated 20thFebruary, 2018.

11. The sole issue now before us is, whether the computer software purchased by the assessee during the year is eligible for depreciation at the rate of 60% as claimed by the assessee or at the rate of 25% as determined by the Ld. AO. On this aspect, Ld. AR referred the details of software, which are placed at page no.80 of the assessee’s paper book, as they were furnished before the Ld. AO. These softwares are Autodesk Software AutoCAD Software, Sales force software customization, Adobe Acrobat Software, Windows 7 pro software, Office 2013, MS Project 2013, AutoCAD Software, SAP License, Adobe Acrobat Software. Sample bills for purchase of such softwares were also furnished before the Ld. AO. Admittedly, the genuineness of purchase of software has not been doubted by the Ld. AO, he only doubted the classification of it as an asset, according to him the software purchased by the assessee are intangible assets and, therefore, are entitled for depreciation at the rate of 25% only. On this issue, Ld. AR placed his reliance on various decisions listed as under:

Arkema Chemicals India (P.) Ltd v. ACIT [2022] 139 taxmann.com 540 (Mum. Trib) 7

CIT v. I-Flex Solutions Ltd [2014] 46 taxmann.com 88 (Bombay HC)

Owens-Corning (India) (P.) Ltd. v. ACIT [2018] 93 taxmann.com 223 (Mumbai -Trib)

Piramal Healthcare Limited v. DCIT [ITA No.1257/Mum/2014] (Mum. Trib.) – Relevant extracts

PRL Developers (P.) Ltd. v. ACIT [2024] 164 taxmann.com 328 (Mumbai – Trib.)

Indian Potash Ltd. v. DCIT [2025] 176 taxmann.com 822 (Delhi – Trib)

DCIT v. Vodafone Business Services Ltd. [ITA No.297/Ahd/2020] (Ahm. Trib)

Plintron Mobility Solutions (P.) Ltd. v. ITO [2021] 133 taxmann.com 366 (Chennai – Trib)

PCIT v. Times Internet Ltd. [2023] 156 taxmann.com 577 (Delhi HC)

CIT v. Computer Age Management Services (P.) Ltd. [2019] 109 taxmann.com 134 (Madras HC)

Amway India Enterprises v. DCIT [2008] 111 ITD 112 (Delhi – Trib) (SB) ACIT v. Indiabulls Ventures Ltd. [ITA No. 1475/Del/2017] (Delhi – Trib)

Cognizant Technology Solutions India Pvt. v. DCIT [ITA No. 160/Chny/2022] (Chennai Trib.)

Caterpillar India P. Ltd v. DCIT [ITA No. 2749/Chny/2017] (Chennai – Trib.)

12. Ld. AR also submitted a brief synopsis extracted from the relevant case laws on the aforesaid issue which is extracted as under:

“Mumbai Tribunal in the case of Arkema Chemicals India (P.) Ltd v. ACIT [2022] 139 taxmann.com 540 [Page 1 to 4 of Legal Paper Book (“LPB”)]:

8………… The issue involved in this appeal is where the assessee has purchased license of ERP SAP, assessee is entitled to the deprecation at the rate of 60% as covered in New Appendix I of Rule 5 of ITAT Rules in heading of machinery and plant in part A of tangible assets at serial 3 3 number 5 “computers including computer software (see note 7 below this table) entitled to depreciation at the rate of 60% or in Para B being licenses, intangible assets entitled to deprecation at the rate of 25%. We find that entry number 5 under Part A allows depreciation at the rate of 60% on computers including computer software. Note-7 states that computer software means any computer programme recorded on any disk, tape, perforated media or other information storage device. Apparently, it does not make any difference between application system software or application software. Further, part B of appendix-1 prescribed deprecation at the rate of 25% on certain intangible assets such as knowhow, patents, copy rights trademarks, license fee, franchise or any other business or commercial right of similar nature. Therefore, the question that arises is the license obtained by the assessee would fall in the definition of computer software so as to make it eligible as tangible asset and then depreciation rate at the rate of 60% will apply.

We now find that the issue is squarely covered in favour of the assessee by the decision of Hon’ble Madras High Court in the case of Computer Age Management Services (P.) Ltd. (supra) wherein depreciation held that software lincense acquired by the assessee was in nature of application software and is eligible for deprecation at the rate of 60%”

(Emphasis added)

Mumbai Tribunal in the case of Piramal Healthcare Limited v. DCIT [ITA No. 1257/Mum/2014] (Mum. Trib.):

“14. The A.O during the course of the assessment proceedings observed that the assessee had during the year incurred software expenses on upgradation of its existing software viz. MFGPRO, MS Office etc. It was noticed by him that the assessee had claimed depreciation on the capitalized value of the software expenses @ 60% the A.O holding a conviction that as the licence to use the software amounted to an intangible asset in the form of rights/ficenses, therefore, the same would be entitled for depreciation @ 25% as against 60%

15. We find that the issue before us is as to whether an independent purchase of software which admittedly formed part of the profit making apparatus of the assesses business and was capitalized in its books of accounts’ would be entitled for depreciation @ 60% (as claimed by the assessee) or 25% (as allowed by the AO). Admittedly, the claim of the assessee towards depreciation on computer software @ 60% was allowed by the CIT(A) in its own case for A.Y 2008-09. The revenue had not carried the aforesaid order of the CIT(A) any further in appeal before the Tribunal, which thus had attained finality. Be that as it may, we find that the ITAT, Mumbai in the case of Owens and Coming (India) P. Ltd. Vs. ACIT, Range 7(3)(i), Mumbai (2018) 93 taxamann.com223 (Mum). had observed that the revenue was in error in restricting the assesses claim of depreciation on computer software @ 60% to 25%. In fact, the Tribunal while concluding as hereinabove, had taken support of the judgment of the Hon’ble High Court Bombay in the case of CIT Vs. Saraswat Infotech Ltd. [ITA (L) No. 1243 of 2012: dated 15.01.2013).

16…. In terms of our aforesaid observations, we are of the considered view that the assessee had rightly claimed depreciation on computer software @ 60%…”

Ahmedabad Tribunal in the case of DCIT v. Vodafone Business Services Ltd. [ITA No.297/Ahd/2020] [Page 24 to 29 of LPB], held as under.

3. Facts relating to the computer software, on which the assessee had claimed depreciation at the rate of 60%, noted in the order of the AO at para-3 is that, it related to SAP products which the AO noted was a customized licensed product. The assessee had incurred expenditure to the tune of Rs. 17,30,28,684/-on purchase of the said SAP product and claimed depreciation at the rate of 60% thereon which was reduced to 25% by the AO holding that the application software being licensed was an intangible asset, and accordingly, depreciation at the rate of 25% was applicable to it….

7. We have heard rival contentions and have gone through the orders of the authorities below. We see no reason to interfere in the order of the Ld.CIT(A) allowing assesses claim of depreciation on licensed software @ 60%. Undeniably assesses claim to 60% depreciation on this software in the preceding years, A.Y 2010-11 to 2012-13, has been consistently upheld by the ITAT. The Ld.DR has sought to distinguish the said decisions pointing out that the claim has been allowed following the ratio laid down by the ITAT in the case of Zydus Infrastructure(supra) wherein the claim related to depreciation on systems software, while in the present case the issue relates to applications softwares. But we find that this distinction has been held to be of no consequence in various decisions of the ITAT and even the Hon’ble High Court. The Hon’ble High Court of Madras in the case of Computer Age Management Services (supra) has categorically held that items listed in Appendix I, prescribing rates of depreciation for different assets under the Act, have to be literally interpreted since the entry is in a taxing statute. In the matter before it the issue was identical, of rate of depreciation applicable to softwares, which as per the Revenue qualified as intangible assets since the softwares were actually licenses granted. The Hon’ble high court held that since computer software has been defined in Appendix as any computer program recorded on disc, tape or other information storage device, it has to be identified accordingly and the description could not be ignored. Therefore irrespective of the usage of the software, the Hon’ble high court held that as long as it fell within the definition provided in the appendix it qualified as computer software for enhanced rate of depreciation of 60%…”

(Emphasis added)”

13. Considering the observations of Tribunal in aforesaid cases, any expenditure incurred by the assessee on software or on upgradation of existing software are in the nature of computer and software covered by new Appendix-I (effective from AY 2006-07 onwards) under the block, machinery and plant at Sr. No. III (5) “Computers including computer software”. Accordingly, the addition made by Ld. AO treating such expenditure to be covered by the provisions of section 32(1)(ii) and by Ld. CIT(A) as a business and commercial right was a misconception, which cannot succeed. We thus, in backdrop of such deliberations direct the Ld. AO to allow the depreciation of software as per rate under Appendix-I Clause III Sub-Clause (5) of the Income Tax Rules as applicable for the year under consideration. In result, the ground No 1 of appeal of assessee is allowed.

14. Ground No.2 – Disallowance amounting to Rs.82,26,54,371/- u/s 14A of the Act read with Rule 8D of the Income Tax Rules, 1961:

On this issue, it is submitted by the Ld. AR that during the year under consideration, the assessee had not earned any dividend income from its investment in equity shares. The assessee has earned share of profit from one of its investments in LLP amounting to Rs.3,952/- only which has been claimed as exempt. Further, the assessee had suo motu made a disallowance of Rs.9,11,435/-u/s 14A of the Act. The Ld. AO has computed the disallowance u/s 14A r.w.r 8D by considering the investment in shares of LLP (both fixed and current capital) and debentures, and determined a disallowance of Rs.92,92,31,540/-. The Ld. AO was of the opinion that the current capital in LLP also has the potential to generate exempt income and, therefore, included both fixed and current capital for the purpose of computing disallowance u/s 14A r.w.r 8D.

15. Ld. CIT(A) discussed the issue, he rejected the contentions of the assessee that the disallowance should be restricted to exempt income only, where the assessee has placed the reliance on Maxopp Investments Ltd. (SC) and other decisions. The Ld. CIT(A) placed his reliance on the decision of Bombay High Court in the case of Godrej & Boyce and Delhi ITAT in Cheminvest Ltd. and held that expenditure has to be disallowed when investments are capable of generating exempt income. Further, the Ld. CIT(A) recorded proper satisfaction that assessee’s claim was incorrect. Hence, invocation of Rule 8D was justified. Ld. CIT(A) accordingly sustained the addition made by Ld. AO and rejected the ground of appeal of assessee.

16. Before us, Ld. Counsel of assessee submitted that the disallowance made by the Ld. AO for Rs.92,92,31,540/- was further reduced to Rs. 82,26,54,371/-vide rectification order u/s 154 of the Act dated 20.02.2018 by excluding the investment in debenture from the computation. It is submitted that the assessee has not earned any dividend income from the shares in which it has invested is an undisputed fact. On the issue of disallowance of section 14A, the assessee has raised various propositions and has submitted relevant case laws as under:

Proposition 1: LLP agreements/ understanding between parties cannot be ignored

CIT v. Arun Dua [1990] 186 ITR 494 (Cal. HC)

Proposition 2: In case of investments in LLP, provisions of section 14A of the Actis not applicable in case of no profit during the year

CIT v. Delite Enterprises [ITA No. 110 of 2009) (Bom HC)

PCIT v. Dipesh Lalchand Shah [2022] 143 taxmann.com 419 (Guj. HC) DCIT v. Apex Realty Pvt Ltd [ITA No. 6265/Mum/2014] (Mum. Trib.) A. H. Baldota v. ACIT [2006] 10 SOT 757 (Mum. Trib.)

Proposition 3: Without prejudice, where sharing of profit of a firm was not dependent on contribution of funds by partners, interest paid by partner on capital borrowed, could not be disallowed u/s 14A

ACIT v. Novel Enterprises [2012] 52 SOT 127 (Mum Trib.)

Proposition 4: Without prejudice, disallowance u/s 14A of the Act to be restricted to amount of exempt income earned during the year PCIT v. State Bank of Patalia [2018] 99 taxmann.com 286 (SC)

PCIT v. Caraf Builders & Constructions (P.) Ltd. 120191414 ΓTR 122 (Delhi HC) and SLP dismissed by SC [2019] 112 taxmann.com 322

Unilever Industries (P.) Ltd. v. DCIT [2024] 205 ITD 212 (Mum. Trib.) PCIT v. McDonald’s India (P.) Ltd. [2019] 101 taxmann.com 86(Delhi HC)

Proposition 5: Without prejudice, in calculation of disallowance u/s 14A r.w.r. 8D, only those investments which yielded exempt income during the year to be considered

S. Krishnamurthy v. ACIT [ITA No. 6207/Mum/2012] (Mum. Trib.)

Geecee Ventures Ltd. v. DCIT [2025] 174 taxmann.com 1285 (Mum. Trib.) DCIT v. Reliance Power Ltd. [2025] 179 taxmann.com 622 (Mum. Trib.)

ACIT v. Zee Media Corporation Ltd. [ITA No. 2166/Mum/2016) (Mum. Trib) ACIT v. Vireet Investments (P) Ltd [2017] 58 ITR(T) 313 (Delhi HC SB) ACB India Ltd. v. ACIT [2015] 374 ITR 108 (Delhi HC)

Proposition 6: Without prejudice, while calculating disallowance u/s 14A of the Act, net interest paid on loan should be taken into consideration

CIT v. Jubliant Enterprises (P.) Ltd. (2019) 416 ITR 58 (Bom HC)

PCIT v. Nirma Credit Capital Pvt. Ltd. (2017) 85 taxmann.com 72 (Guj. HC)

PCIT v. Nirma Credit Capital Pvt. Ltd. (ITA No. 980/Ahd/2012) (Ahm Trib.)

Piramal Enterprise Ltd. (As a sucessor to PHL Holdings Pvt. Ltd) v. ITO (ITA No. 3536/Mum./2010 (Mum. Trib)

Proposition 7: Amendment inserted vide Finance Act 2022 is prospective in nature Aasan Corporate Solutions Private Limited v. DCIT (ITA 5524/Mum/2024) (Mum. Trib.)

Proposition 8: In absence of exempt income earned, suo-moto disallowance also requires to be deleted

HDFC v. ACIT (ITA 5480/Mum/2014 (ITA No. 5481/Mum/2014) (Mum. Trib) Piramal Estates Private Limited (Formerly known as Alpex International Private Limited) v. ACIT (ITA No. 779/Mum/2014) (Mum. Trib)

Aditya Birla Nuvo Limited v. ACIT (ITA No. 4220/Mum/2015) (Mum. Trib.)

Proposition 9: Without prejudice, no 14A disallowance should be made in absence of satifaction recorded.

Godrej & Boyce Manufacturing Company Ltd. v. DCIT [2017] 81 taxmann. com 111 (SC)

PCIT v. Vedanta Ltd [2019] 102 taxmann.com 95 (Delhi HC)

PCIT v. Godrej & Boyce Mfg. Co. Ltd [2023] 149 taxmann.com 222 (Bom. HC)

17. To support the propositions, a short note was also submitted before us which is extracted as under:

“Proposition 1: There is no mandatory requirement in law (i.e. LLP Act) to contribute capital in order to be a partner in LLP

8. The Appellant submits that there is no mandate in the law to contribute any capital order to be entitled to the share of profit in a LLP. Whether under the Indian Partnership Act, 1932 or under LLP Act,2008, in order to become a partner and get share of profit, there is no sine qua non to contribute to capital.

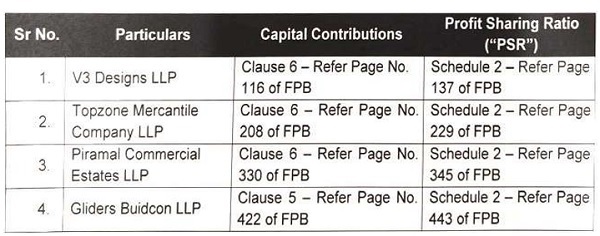

9. However, as per section 33 of the Limited Liability Partnership Act, 2008, the obligation of a partner to contribute money shall be as per the limited liability partnership agreement. Accordingly, as per the terms of the LLP deeds, there are specific clauses governing the fixed and current capital by partner, which is summarised below on specimen basis:

The Appellant submits that the relevant clauses governing capital contribution clearly provide that the fixed capital shall be maintained in the ratio specified in Schedule 2 (i.e., the PSR). Further, attention is invited to sub point 6 of relevant clause for capital contribution, which clearly states that “The partners may be entitled to received interest on their current capital as may be decided by the Partners from time to time”.

Accordingly, a partner is only required to introduce fixed capital in the LP in order to be entitled to a share of profits in terms of the LLP Deed.

10. The Appellant submit that in fact, current capital is capable of generating taxable income in the form of interest. In support of its contention, the Appellant places reliance on the judgment of Mumbai Tribunal in the case of ACIT v. Novel Enterprises [2012] 52 SOT 127, wherein the Mumbai Tribunal upheld the action of the CIT(A) as under.

“5. Being aggrieved, the assessee moved its grievance before the CIT(A), who deleted the additions, wherein the CIT(A) observed: “3.3 I have considered the submissions made for the appellants and the assessment order. On careful consideration of the facts of the case and the provisions of the Act, I agree with the appellant that the provisions of section 14A are not applicable in the present case. The appellant had raised interest bearing loan from Reliance Capital Ltd. The said Loan had been utilized by the appellant for the purchase of shares and also for making capital contribution to M/s Shreenath Enterprises in which the appellant was a partner.

The Assessing Officer has given the details of capital contributed by all the three partners including the appellant in order to substantiate his contention that the share of profit received by the partner is directly in proportion to the capital contributed by the partners. On the other hand, the appellant is of the view that there is no connection between the funds contributed by the appellant and the share of profit received from the partnership firm. M/s. Shreenath Enterprises, being a partnership firm, is governed by the Indian Partnership Act, 1932. There is no provision in the said Act as regards the contribution of capital by the partners. In other words, the Act does not contemplate or stipulate capital contribution by the partner as one of the conditions for a partnership firm……, including the appellant, are entitled to the profit sharing as per the partnership deed and the same was not dependent.on.contribution of funds made by the partners. Clause (8) of the partnership deed deals with the, capita/loans introduced by the partners to the firm. It clearly states that the partners may introduce capital and or give Loan to the firm which shall carry interest @ 12% annum or any other rate has been mutually agreed upon”

we subscribe to 9. We have gone through the submissions and also the orders of the Revenue authorities and we have no hesitation of accepting the decision of the CIT(A), to which

(Emphasis added)

11. Accordingly, the Appellant submits that the suo motu disallowance of Rs. 9,11,435/-as computed by it deserves to be accepted, as the same has been determined by considering fixed capital in LLPs.

Without Prejudice to Proposition 1:

12. The Appellant submits that it is well settled law that no disallowance u/s 14A r.w.r 8D is warranted in respect of investments wherein no share of profit has been earned. The Appellant places reliance on the following judicial precedents in support of its contention:

CIT v. Delite Enterprises [ITA No. 110 of 2009) (Bom HC) [Page 42-42 of LPB]

PCIT v. Dipesh Lalchand Shah [2022] 143 taxmann.com 419 (Guj. HC) [Page 44-50 of LPB] A. H. Baldota v. ACIT [2006] 10 SOT 757 (Mum. Trib.) (Page 55-63 of LPB]

DCIT v. Apex Realty Pvt Ltd [ITA No. 6265/Mum/2014] (Mum. Trib.) [Page 51-54 of LPB]

With this, the Appellant submits its further proposition as under:

Proposition 2: In calculation of disallowance u/s 14A r.w.r. 8D, only those investments which yielded exempt income during the year to be considered:

13. The Appellant submits that in calculation of disallowance u/s 14A r.w.r 8D, only thoseinvestments which has yielded exempt income during the year is to be considered. In support of its contention, the Appellant places reliance on the following judicial precedents:

ACIT v. Vireet Investments (P) Ltd [2017] 58 ITR(T) 313 (Delhi HC SB)

S. Krishnamurthy v. ACIT (ITA No. 6207/Mum/2012) (Mum. Trib.) [Page 67-73 of LPB]

ACB India Ltd. v. ACIT [2015] 374 ITR 108 (Delhi HC) [Page 67-73 of LPB]

14. During the year under consideration, the Appellant has earned exempt income i.e. share of profit from only one LLP, namely PRL Properties LLP.

Proposition 3: Only ‘net interest expenditure’ can be considered for making disallowance u/s. 14A of the Act:

15. Further, the Appellant submits that even if disallowance u/s 14A r.w.r 8D be made, net interest expenditure should be considered along with those investments which has earned exempt income during the year. In this regards, the Appellant places reliance on the following judicial

ADDITIONS

CIT v. Jubliant Enterprises (P.) Ltd. (2019) 416 ITR 58 (Bom HC) [Page 106-107 of LPB]

PCIT v. Nirma Credit Capital Pvt. Ltd. (ITA No. 980/Ahd/2012) (Ahm Trib.) [Page 115 to 117 of LPB)

Piramal Enterprise Ltd. (As a success or to PHL Holdings Pvt. Ltd) v. ITO (ITA No. 3536/Mum./2010 (Mum. Trib)

16. Accordingly, in view of proposition 2 and 3, the Appellant submits that disallowance u/s 14Aof the Act to be computed only based on fixed capital of PRL Properties LLP: i If gross interest expenditure is taken into consideration-restricted at Rs. 10,681

ii. If net interest expenditure is taken into consideration – restricted at Rs. 4,753/-deleted. Thus, the excess disallowance including the suo moto disallowance made by the Appellant be

Without Prejudice to Proposition 1, 2 & 3:

Proposition 4: The disallowance u/s 14A r.w.r 8D should be restricted to exempt income earned during the year:

17. The Appellant submits that the disallowance, if any, should be restricted to exempt income earned during the year. In support of its contention, the Appellant places reliance on the following judicial precedents: PCIT v. State Bank of Patalia [2018] 99 com286 (SC) [Page 91-93 of LPB]

PCIT v. Caraf Builders & Constructions (P.) Ltd. [2019] 414 ITR 122 (Delhi HC) and SLP dismissed by SC [2019] 112 taxmann.com 322 [Page 94-101 of LPB]

Unilever Industries (P.) Ltd. v. DCIT [2024] 205 ITD 212 (Mum. Trib.) [Page 102-105 of LPB]

18. As stated above, during the year under consideration, the Appellant has earned share of profit of Rs. 3,952/- only from PRL Properties LLP which it has claimed as exempt during the year.

19. Accordingly, the disallowance u/s 14A r.w.r 8D should be restricted to exempt income of Rs. 3.952/-

The Appellant humbly submits that based on alternative contentions, the disallowance u/s 14A of the Act r.w.r 8D of Rs. 82,26,54,371/- be deleted including the suo motu disallowance restricted as per thes contentions stated above.

In view of the foregoing, the Appellant humbly submits that the suo-moto disallowance computed considering the fixed capital balances invested in LLPs be accepted. However considering the nominal exempt income earned during the year, in the event Your Honour is inclined to allow the appeal on the other propositions as set out above, it is respectfully requested that the issue relating to disallowance under section 14A in respect of current capital balances in LLPs be kept open, so as to enable the Appellant to agitate the same in subsequent years.”

18. We have considered the rival submissions, perused the material available on record and the jurisprudence relied upon by the parties. Under the factual matrix of the present case, it is brought to our knowledge that the assessee is engaged in the business of real estate and holds investment in shares and partnership interest in LLP which operates as SPV engaged in real estate activities. It is also claimed that the assessee has not earned any dividend income from its investment in the shares, however, the share of profit from one of its investment LLP was amounting to Rs.3952/- which has been claimed as exempt. The assessee also suo motu made a disallowance of Rs.9,11,435/- u/s 14A Act.

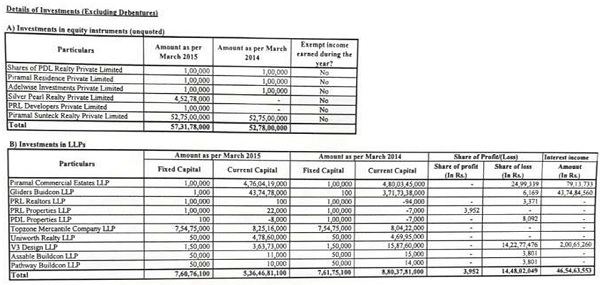

19. Before us, the Ld. AR of assessee submitted that the disallowance of Rs.92.92 crores made by the Ld. AO was subsequently reduced to 82.25 crores vide rectification order u/s 154 dated 20thFebruary, 2018. It is suited by Ld. AR that the assessee’s investments are in equity instruments and inertia LLPs, a statement showing opening and closing balance of such investment and exempt income earned during the year is furnished. The same is extracted hereunder for the sake of interpretation and reference:

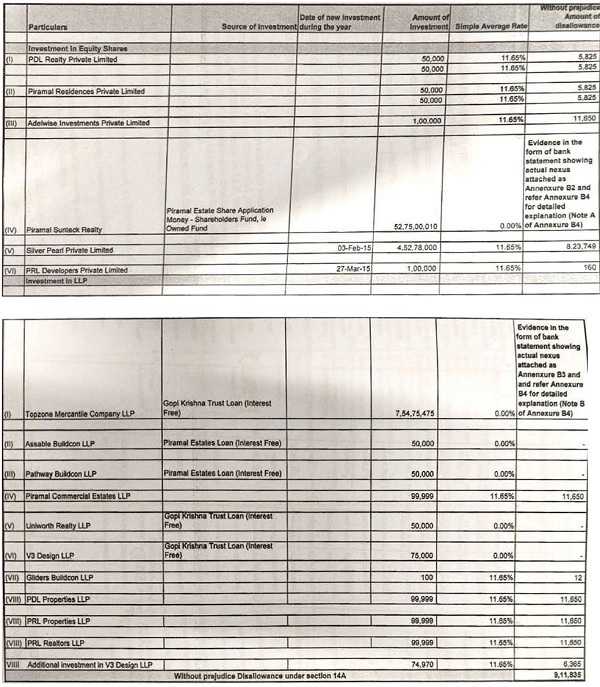

20. Referring to the afore said information, it is submitted that the assessee has not earned any dividend from its investment in equity instruments, therefore, there was no need of any disallowance u/s 14A r.w.r 8D, as the disallowance has to be restricted to the extent of exempt income earned during the year only, reliance has been placed on the decision in the case of PCIT vs. State Bank of Patiala and other decisions (referred to supra). Regarding assessee’s investment in LLPs, it is submitted that the contribution in capital made by the assessee in different LLPs as per chart furnished hereinabove, the assessee has made fixed capital contribution as well as contribution towards current capital of the LLPs. It is clarified that the assessee is entitled for share in profit of the LLP, which is exempt from tax on fixed capital contributions and the income for current year under this head was Rs.3952/-, which the assessee itself has claimed as exempt during the year and, therefore, the disallowance u/s 14A r.w.r 8D should be restricted to such exempt income of Rs.3952/-only. Regarding assessee’s contribution towards the current capital, it is submitted that such amount contributed by the assessee in LLPs has the potential to earn interest income which in any case is taxable in the hands of assessee under the head income from business, therefore, no disallowance on such investments would be required u/s 14A r.w.r 8D, being generating taxable income. It is also submitted that the assessee has worked out a suo motu disallowance of Rs.9,11,435/-, the working of which has been furnished before us at page nos.88 and 89 of the assessee’s paper book. The details so furnished are extracted hereunder for the sake of completeness of facts:

21. On perusal of afore aid chart, it can be gathered that the assessee has shown an average income f om the investment made in aforesaid concerns in the form of investment in equity shares and investment in LLP. It is also the submission by Ld. AR, the addition could have been made only to the extent of exempt income earned by assessee, however, the suo motu disallowance computed considering the fixed capital balance investment in LLP be accepted. It is also requested to keep the issue of current capital balance in LLP as open so that the assessee would be at liberty to agitate the same in subsequent years. We, without going into each and every proposition of the assessee as prayed by the Ld. AR find it appropriate to settle the issue by allowing the assessee to continue with the suo motu disallowance made by it and direct the AO to restrict the same to the extent of Rs.9,11,435/-.In result, the Ground of Appeal No.2 of assessee is allowed in above terms.

22. Ground No.3 – Regarding addition of disallowance of Rs.82,26,54,371/- u/s 14A of the Act r.w.r. 8D of the Income Tax Rules for the purpose of computing book profit u/s 115JB of the Act:

On the issue, Ld. AR submitted as under:

“1. Facts of the case and Action of Commissioner of Income-tax (Appeals) [“the CIT(A)”]:

1. The Ld. AO added back the disallowance made u/s 14A r.w.r BD of Rs. 82,26,54,371/- in calculation of book profit u/s 115JB of the Act.

2. The Hon’ble CIT(A) upheld the action of the AO

II. Submissions before the Hon’ble Tribunal:

1. The Appellant submits that the disallowance made under Rule 8D cannot be added to book profit as per section 115JB of the Act. The Appellant places reliance on the following judicial precedents in support of its contention:

CIT v. Bengal Finance & Investments Pvt. Ltd (ITA 337 of 2013) (Bom. HC) [Page 147-148 of LPB]

ACIT v. Trapti Trading & Investments Private Limited (I.T.A. No. 4851/Mum/2025) (Mum. Trib) [Page 149-154 of LPB]

ACIT v. Vireet Investment (P.) Ltd. [2017] 82 taxmann.com 415 (Delhi Trib.)

2. In view of the foregoing, the Appellant prays that the addition to book profit, if any, should be restricted to suo moto disallowance of Rs. 9,11,435/- or restricted to exempt income earned of Rs. 3,952/-”

23. We find that the aforesaid ground of appeal of the assessee is squarely covered by the decision of Hon’ble Special Bench Delhi Tribunal in the case of ACIT vs. Vireet Investment (P.) Ltd. [2017] 82 com415 (Delhi Trib.). Therefore, the disallowance made by Ld. AO cannot be added back to the book profit computed under the provisions of section 115JB of the Act. The disallowance, thus, so made by the Ld. AO is liable to be deleted.

24. Ground No.4 – Charging of interest u/s 234B and 234C of the Act:

The ground, being consequential in nature, needs to be revisited by the Ld. AO while giving effect to this order of the Tribunal.

25. In result, the appeal of assessee is allowed in above terms.

Order pronounced in the open court on 24-06-2026.

Author Bio