#ITAT Judgments

Log in to FollowITAT Judgment contain Income Tax related Judgments from Income Tax Appellate Tribunal Across India which includes ITAT Mumbai, Chennai, Delhi, Kolkutta, Hyderabad etc.

Income Tax

Income Tax

Foreign Tax Credit Cannot Be Denied for Delayed Form 67 Filing: ITAT Mumbai

Income Tax

Income Tax

Strategic Investments of Bank Taxable as Capital Gains, Not Business Income: ITAT Ahmedabad

Income Tax

Income Tax

State DISCOM Tariff, Not IEX Rates, to Benchmark Captive Power Transfers Under Section 80-IA: ITAT Delhi

Income Tax

Income Tax

Section 80P Deduction Allowed on Interest & Dividend Income of Co-op Credit Society: ITAT Pune

Income Tax

Income Tax

Section 80P Deduction Allowed on Interest Earned from Bank Deposits by Co-operative Credit Society: ITAT Pune

Income Tax

Income Tax

Section 80P Deduction Allowed on Interest from Co-operative Bank Deposits: ITAT Pune

Income Tax

Income Tax

Income Declared in Original Return Cannot Be Reduced in Section 148 Return: ITAT Hyderabad

Income Tax

Income Tax

Registered Sale Deed Triggers Capital Gains Despite Dispute Over Consideration: ITAT Hyderabad

Income Tax

Income Tax

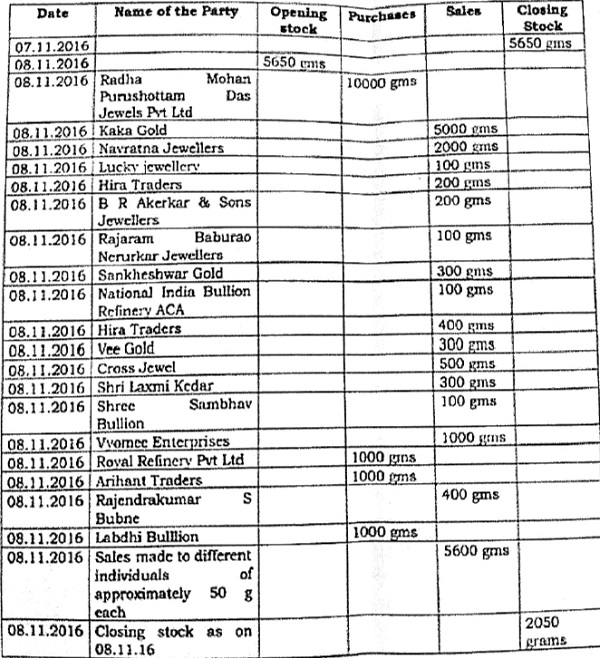

ITAT Mumbai Deletes Section 68 Addition on Recorded Cash Sales

Income Tax

Income Tax