The Reserve Bank of India (RBI) has come out with a revised prompt corrective action (PCA) framework for banks, spelling out certain thresholds, the breach of which could invite resolutions such as a merger with another bank or even shutting down of the bank. The Reserve bank of India ask bank to improve their Financial position (by putting four Parameters), Otherwise they will put Restriction with regards to Dividend distribution, branch expansion, management compensation and directors’ fees etc. This will definitely will shrink the Business of the Bank, thus they have no option left except to get merge with other powerful bank.

There are four Parameters includes in PCA norms:

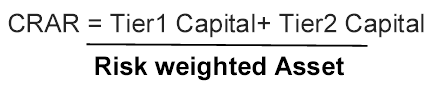

CAPITAL: CRAR- Minimum regulatory prescription for capital to risk assets ratio + applicable capital conservation buffer(CCB) current minimum RBI prescription of 10.25% (9% minimum total capital plus 1.25%* of CCB as on March 31, 2017)

*CCB would be 1.875% and 2.5% as on March 31, 2018 and March 31, 2019 respectively.

And/ Or

Regulatory pre-specified trigger of Common Equity Tier 1 (CET 1min) + applicable capital conservation buffer(CCB) current minimum RBI prescription of 6.75% (5.5% plus 1.25%* of CCB as on March 31, 2017) Breach of either CRAR or CET 1 ratio to trigger PCA

The capital conservation buffer is designed to ensure that banks build up capital buffers outside periods of stress which can be drawn down as losses are incurred.

Breach of ‘Risk Threshold 3’ of CET1 by a bank would identify a bank as a likely candidate for resolution through tools like amalgamation, reconstruction, winding up, etc.

Let us understand how to calculate CRAR/CET1

Capital adequacy ratio is defined as:

TIER 1 CAPITAL = (paid up capital + statutory reserves + disclosed free reserves) – (equity investments in subsidiary + intangible assets + current & brought-forward losses)

TIER 2 CAPITAL = A) Undisclosed Reserves + B) General Loss reserves + C) hybrid debt capital instruments and subordinated debts

Risk weighted assets – Fund Based : Risk weighted assets mean fund based assets such as cash, loans, investments and other assets. Degrees of credit risk expressed as percentage weights have been assigned by the national regulator to each such assets. The notional amount of the asset is multiplied by the risk weight assigned to the asset to arrive at the risk weighted asset number. Risk weight for different assets vary e.g. 0% on a Government Dated Security and 20% on a AAA rated foreign bank etc.

Bank “A” has assets totaling 100 units, consisting of:

- Cash: 50 units

- Government bonds: 100 units

- Mortgage loans: 120 units

- Other loans: 320 units

- Other assets: 120 units

Bank “A” has debt of 950 units, all of which are deposits. By definition, equity is equal to assets minus debt, or 5 units.

Bank A’s risk-weighted assets are calculated as follows

| Cash | 50 *0%=0 |

| Government securities | 100*0% =0 |

| Mortgage loans | 120*50%= 60 |

| Other loans | 320*100%= 320 |

| Other assets | 120*100 =120 |

| Total risk | |

| Weighted assets | 500 |

| Equity | 50 |

| CRAR (Equity/RWA) | 10% |

Tier 1 capital is calculated as common equity tier 1 (CET1) capital plus additional Tier 1 capital (AT1). Common equity Tier 1 comprises of a bank’s core capital and includes common shares, stock surpluses resulting from the issue of common shares, retained earnings, common shares issued by subsidiaries and held by third parties, and accumulated other comprehensive income (AOCI).

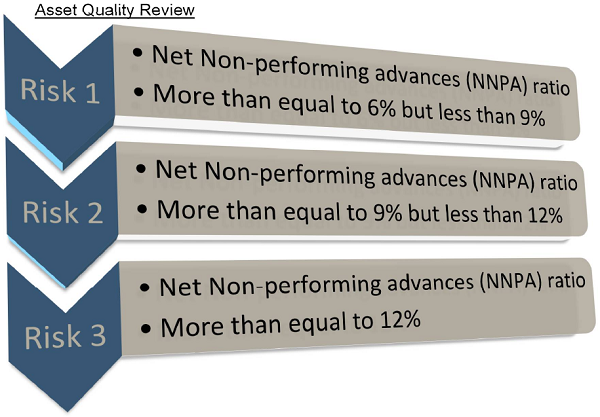

| Net Non-performing advances (NNPA) ratio

Gross NPA – (Balance in Interest Suspense account + DICGC/ECGC claims received and held pending adjustment + Part payment received and kept in suspense account + Total provisions held). |

NPA ratio = Net non-performing assets /Net Advances

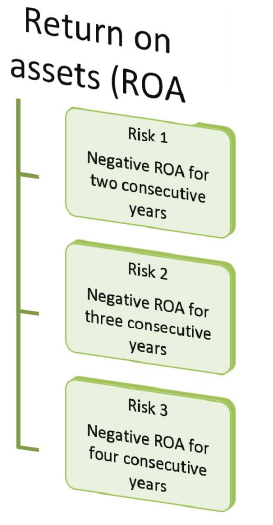

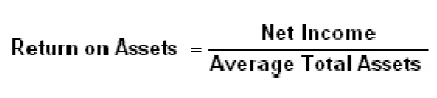

Profitability: It is calculated based on the Return on asset of the bank

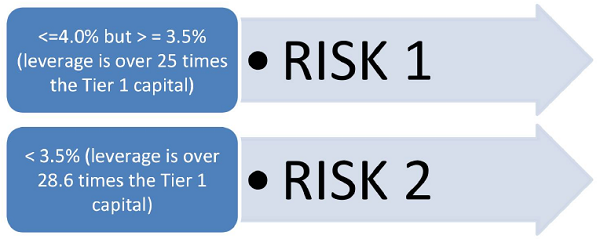

Leverage Ratio: The Tier 1 leverage ratio is the relationship between a banking organization’s core capital and its total assets. The Tier 1 leverage ratio is calculated by dividing Tier 1 capital by a bank’s average total consolidated assets and certain off-balance sheet exposures. Similarly to the Tier 1 capital ratio, the Tier 1 leverage ratio is used as a tool by central monetary authorities to ensure the capital adequacy of banks and to place constraints on the degree to which a financial company can leverage its capital base.

Asset Quality Review as on Dec 2016 shows that most of the banks are struggling from Asset Quality.

| Mandatory and discretionary actions | ||

| Specifications | Mandatory actions | Discretionary actions |

| Risk Threshold 1 | Restriction on dividend distribution/remittance of profits.

Promoters/owners/parent in the case of foreign banks to bring in capital |

Common menu

Special Supervisory Interactions Strategy related Governance related Capital related Credit risk related Market risk related HR related Profitability related Operations related Any other |

| Risk Threshold 2 | In addition to mandatory actions of Threshold 1,

Restriction on branch expansion; domestic and/or overseas Higher provisions as part of the coverage regime |

|

| Risk Threshold 3 | In addition to mandatory actions of Threshold 1,

Restriction on branch expansion; domestic and/or overseas Restriction on management compensation and directors’ fees, as applicable |

|

Author can be reached at DeepakRathore.8888@gmail.com

Author Bio

well explained with good Presentation skill

Good work

Keep it up