Introduction: –

From the traditional offline banking system to the online based banking operations, offering payment and receipt services through digital platforms, core banking system and many more features have been adopted by this industry for the benefit and conveyance of the customers worldwide. This has added value to the business operations and provided the ease of carrying out many activities which otherwise would have been a great hassle for them.

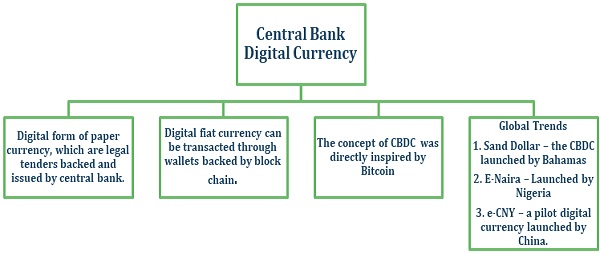

However, even after such multitude of changes, the future of money is still under the process of technical advancement. And one of such advancement is the upcoming concept of Central Bank Digital Currency. Central bank digital currencies (CBDCs) are a form of digital currency issued by a country’s central bank. They are similar to cryptocurrencies, except that their value is fixed by the central bank and equivalent to the country’s fiat currency. Many countries are developing CBDCs, and some have already implemented them.

Page Contents

Brief facts of Central Bank Digital Currency (CBDC):

Types of CBDCs

Types of CBDCs

Wholesale CBDC

These are exclusively used by central banks, commercial banks or other financial institutions to settle large value interbank transactions.

Retail CBDC

These digital currencies are used by the consumers and businesses. Retail CBDC eliminate intermediary risk. This is further bifurcated into 2 types –

- Token-based retail CBDCs – these are accessible with private keys or public keys or both. This method of validation allows users to execute transactions anonymously.

- Account-based CBDC – this type of CBDC requires digital identification to access an account.

Benefits of implementing CBDC

1. Removes the cost of implementing a financial structure within a country to bring financial access to the unbanked population.

2. Can lower cross-border transaction costs by reducing the complex distribution systems and increasing jurisdictional cooperation between governments.

3. Eliminates the third party risk of events like bank failures or bank runs. Any residual risk that remains in the system rests with the central bank.

4. CBDCs can help reduce the costs and risks associated with physical cash handling. They can reduce the need for cash handling and transportation, which can be expensive and pose security risks.

5. CBDCs can also help prevent counterfeiting and theft, which can be significant issues with physical cash.

6. The upgradation can provide increased security and transparency. They offer strong encryption and authentication protocols that can help prevent fraud and cyberattacks.

Challenges of adopting CBDC

1. The first issue to tackle is the heightened risk to the privacy of users. The central bank could potentially end up handling an enormous amount of data regarding user transactions

2. With the ability to provide digital currency directly to its citizens, one concern is that depositors would shift out of the banking system. Customers may deem the safety, liquidity, solvability, and publicity of CBDCs to be more attractive, weakening the balance sheet position of commercial banks.

3. Faster obsolescence of technology could pose a threat to the CBDC ecosystem calling for higher costs of upgradation.

4. It may create operational risks of intermediaries as the staff will have to be retrained and groomed to work in the CBDC environment.

Conclusion

In the near future, digital money transactions brought about by CBDC are probably going to bring about a pragmatic revolution in the economy. The entire monetary infrastructure will become more efficient and streamlined with the implementation of this currency system. It will not only be more convenient, but it will also support the government’s objective of transitioning toward a digital economy.

But with the changes in the system, the CBDCs must prioritize the security and privacy. Robust cybersecurity measures should be in place to protect against hacking and fraud. Simultaneously, mechanisms for ensuring user privacy and data protection should be established and maintained.

(This article represents the views of the authors only and does not intent to give any kind of legal opinion on any matter)

Authors: Shripriya Aithal | Consultant | +918779984264 | shripriya.aithal@masd.co.in

Author Bio