Salaried individuals are issued form 16 from their employersat the end of financial year. The details mentioned thereon are helpful in filing income tax return.

This article attempts to explain everything a tax payer should know about form 16 before filing income tax return. It is to be noted that form 26AS is of utmost importance and an aid to e file correct return to avoid any future complications and hassle free processing.

Form 16 is a certificate of deduction of tax at source from salary under section 192, issued by employer in respect of employee. It is an undertaking showing the details of tax deducted and deposited with Income Tax department by employer. The certificate is generated by employer from TRACES portal. It is always advisable to verify the TDS details with particulars of form 26AS.

Form 26AS is an annual tax statement under section 203AA that shows the tax credit in respect of an assessee. It reflects the details of tax deposited with the Government in respect of assessee from all sources. The new form 26AS contains information about TDS,TCS, details of tax paid, details of paid refund, details of specified financial transactions, information regarding pending and completed proceedings, TDS defaults, details of turnover as per GSTR-3B etc. to make assessment easy and fair. It can be viewed or downloaded from my account tab >> view form 26AS after logging in your account.

It is always advisable to verify the details of every TDS certificate issued from deductor with form 26AS. Any variation should be brought to the notice of deductor, so that he may revise the TDS return.

Understanding form 16

Form 16 has two parts Part A and Part B. Please ensure form 16 given by your employer is from TRACES. A valid form 16 has 7 character alphabet unique certificate number and it has TDS – CPS logo on the left top and national emblem on the right. Refer to the image below:

Form 16 Part A

The part A of form 16 provides details of tax deducted and deposited for all quarters of financial year. However, if there is change in employment during the year or case of more than one employer, every employer shall issue a separate part A of the certificate in form 16 for the period of employment with respective employers.

The Part A of form 16 contains following information:

1. Name and Address of Employer

2. Name and Address of Employee

3. PAN and TAN of Deductor/Employer

4. PAN of employee

5. Address of Commissioner of Income Tax having jurisdiction in respect of TDS statement of assessee.

6. Assessment Year

7. Period of employment

8. Quarter wise summary of amount paid and TDS thereon in respect of employee

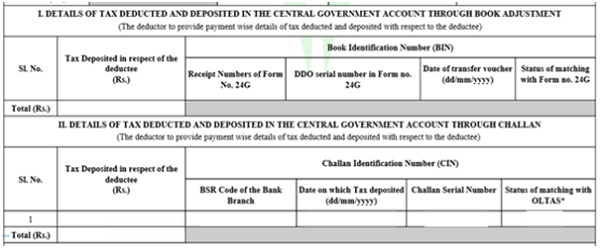

9. Details of tax deducted and deposited in Central Government Account (1) through book adjustment if the deductor is Government and tax is paid without production of Income Tax Challan (2)through challan if Government deductor has paid tax accompanying Income Tax Challan or the deductor in non-Government.

In this case, if your employer is non-Government, your TDS details will be reflected in II item. In case if deductor is Government the TDS details can be reflected in I or II depending upon the case.

The total tax deducted and deposited should be verified from form 26AS.

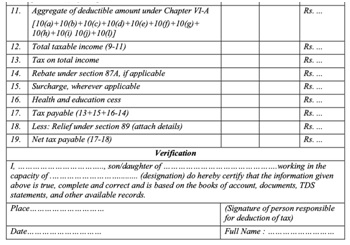

10. Verification

Form 16 Part B

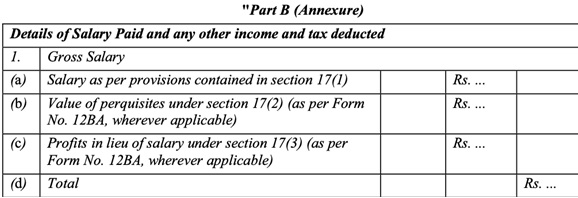

Part B of form 16 is an annexure to part A issued by employer. In case of more than one employer, the part B may be issued by every employer or by last employer at the option of assessee.

The part B contains particulars of salary, deductions under chapter VIA and tax calculations. This section is a reference section for filing your ITR. The assessee should report salary break up, allowances and exemptions referring to form 16.

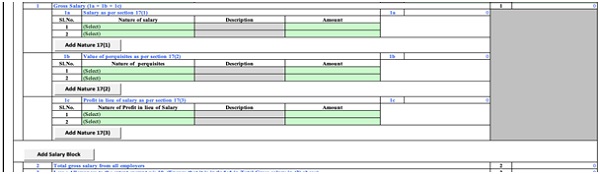

1. Gross salary contains three parts:

All the three sections should be reported in salary section of your ITR.

Part B

ITR-1 form

ITR-2 form

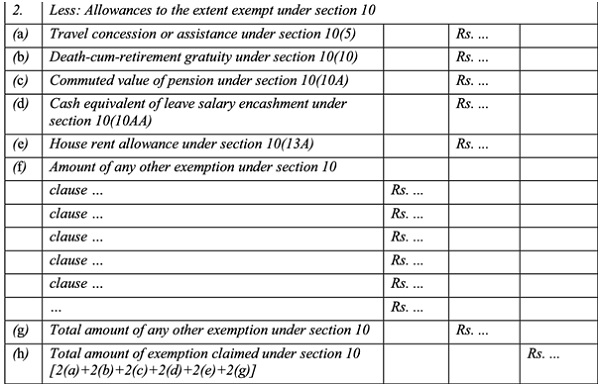

2. The gross salary so arrived is reduced by exempt allowances

Part B

Refer to the exemption in this section and verify the exemption you are claiming.

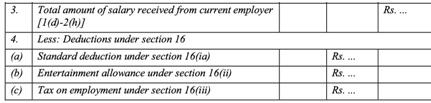

Point 3 will give salary received from employer before deductions under section 16.

Point 4 standard deduction u/s 16(ia) is Rs. 50,000 or salary whichever is less. The deductible amount is automatically reflected. The other two are permissible depending upon the case. The same columns will be visible in your ITR utility.

At this point income chargeable u/h salaries is arrived as reflected in point 6 of form 16.

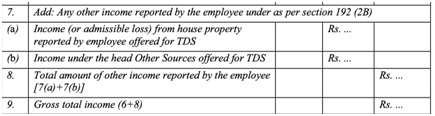

If employee has reported income from any other source (House property and other sources) with employer for the purpose of TDS, it will be reflected in point 7 and the same should be entered or verified in ITR utility.

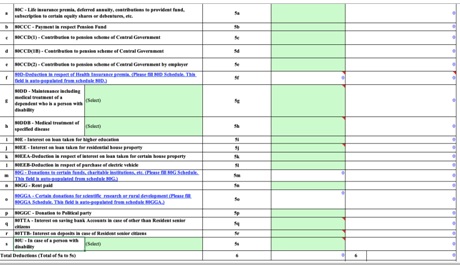

After adding income from all stated sources, Gross total income is arrived and deductions under Chapter VI-A is claimed herefrom.

The deductions allowed by employer on the basis of proof of investment submitted will be shown in form 16 and the details can be reflected in VIA tab in ITR utility. (in case of ITR1 there is no separate tab for VIA, the information has to be entered or verified in ‘income details’).

ITR-1 utility

ITR-2 utility

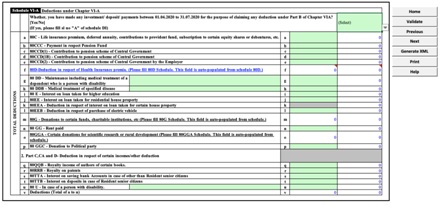

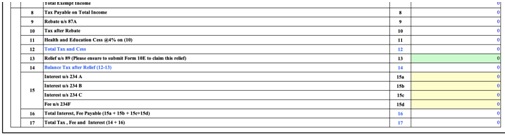

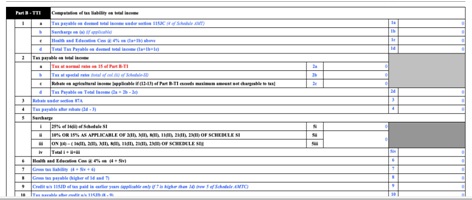

After allowing deduction under chapter VI-A from Gross Total Income, total taxable income is arrived and tax calculations are made. This calculation is available in ITR-1 utility in same sequence. In other utilities the calculations are shown in Part B TI-TTI.

ITR-1 utility

ITR-2 utility

Last is verification from employer with Date, place of issue and signature.

Please note that author has used ITR-1 and ITR-2 offline utility for reference. The process is same for other utilities too.

Any queries can be written to author @ leena36a@gmail.com.

Author Bio