In layman’s language, cryptocurrency is a digital currency designed to buy goods and services, like other currencies. However, since the beginning, it has always been controversial because of its independent nature, which means that it works without agents such as banks, financial institutions, or local authorities.

Today, more than 1,500 currencies, such as Bitcoin, Ethereum, Litecoin, Dogecoin, Ripple, Matic, etc., are traded in the world of digital currencies. Investments in the trading of cryptocurrencies have increased significantly.

Is crypto a ‘currency’ or an ‘asset

Crypto and NFT are classified as “Virtual Digital Assets” and section 2(47A) has been added to the Income Tax Act to define this term. The definition is comprehensive but includes any information, code, number, or symbol (not Indian currency or foreign currency), derived by cryptographic means. In simple terms, VDA means all types of crypto assets, including NFTs, tokens, and cryptocurrencies but will not include gift cards or passes.

Is crypto tax in India?

Yes, profits from cryptocurrency are taxable in India. The position of the government on cryptocurrency and other VDA is explained in the Budget 2022.

How is Cryptocurrency taxed in India-

In India, cryptocurrency is categorized as a Virtual digital asset and is subjected to tax.

The Income from buying and selling cryptocurrency is taxed at the rate of 30% (plus 4% cess) as per section 115BBH.

Section 194S imposes a 1% tax deducted at source (TDS) on the transfer of crypto assets from July 01, 2022, if the transaction exceeds 50,000 (or 10,000 in some cases) in a similar financial year.

Crypto taxes apply to all investors, whether private or corporate, who transfer digital assets every year.

The rate of tax is similar for short-term and long-term income, and it applies to any type of gain received by the investor.

Transactions of Crypto are liable to tax in India?

If you participate in any of these transactions, you will be required to pay a 30% tax:

- Spend Crypto currencies to buy goods or services.

- Swap Crypto currency for other Crypto currency.

- Dealing with Cryptocurrency by using fiat currency like (INR).

- Collect Crypto currency as payment for services.

- Earning Crypto currency as a gift.

- Quarry Crypto currency.

- Depiction a salary in crypto.

- Staking crypto and get the benefit of staking.

- Collect Airdrops.

How to calculate taxes on crypto-

Now that you know that you will pay 30% tax on your profit in crypto, let’s see how to calculate the profit.

Profit is nothing but –

(Selling price – Cost Price)

Explaining TDS on Crypto Transactions-

When you buy or sell crypto currency, you may be required to pay Tax Deduction at Source (TDS). This means that a certain percentage of the transaction amount will be deducted from the source and paid to the government. The remaining amount will be paid to the seller. In India, the TDS rate for crypto is 1%. Starting July 01, 2022, customers will need to pay TDS withholding tax at a rate of 1% when paying for Crypto/NFT transfers. If the transaction takes place on an exchange, the exchange may deduct the TDS and pay the remaining amount to the seller. Indian businesses automatically deduct TDS, while individuals dealing on foreign exchanges must manually subtract TDS and file their TDS. Here’s an example: if you buy crypto currency worth INR 10,000, the TDS deducted will be INR 100, and you will receive INR 9,900. To calculate the TDS for your crypto transactions accurately, you can use the formula: Transaction amount x TDS rate.

- P2P Transactions: In the case of P2P transactions, the customer will be responsible for subtracting TDS and filing 26QE or 26Q, whichever is applicable.

Example-

1. Let’s say that someone in the UK has 1 BTC, which they want to sell

2. A customer listed their 1 BTC on a P2P exchange at a price of $30,500.

Crypto-to-Crypto Transactions:

Tax-

Trading: A 30% crypto tax is charged when you trade crypto.

Exchange: A similar tax of 30% is also applied in such cases.

TDS-

TDS will be applied both to buyer and seller at 1%.

Example –

If you use 2500 Ethereum to buy Rs 2500 worth of Bitcoin, you must pay 1% TDS of both side of transactions ( Buy and sale).

Rs. 25 – On Ethereum

Rs. 25 – On Bitcoin

Airdrops and Tax Implications-

Airdrops refer to the distribution of cryptocurrency tokens or coins directly to a designated wallet address, often without any cost. This process aims to promote awareness of the token and boost the circulation of new currency during its initial stages. However, it’s important to note that a 30% tax may apply to airdrops.

Rule 11UA determines the tax amount for airdrops. If you acquire cryptocurrency through airdrops and later sell, exchange, or spend your tokens, you will be subject to a 30% tax on your income. This tax is calculated based on the market value of the token on the day it was received on an exchange or DEX.

For example-

• However, if you receive 20,000 ABC tokens through an airdrop on April 1, 2022, and also acquire ABC tokens that are traded on an exchange or DEX, then you will be subject to a 30% tax on the profit made.

• If Token ABC is valued at Rs 10 on the day it was received, the tax will be calculated at 30% on Rs 2,00,000 (20,000* Rs 10).

• If you decide to sell these tokens at Rs 500000 then the cost will be Rs 200000, and the remaining Rs 300000 will be taxed at 30%.But if you receive crypto as payment for goods or service or by an airdrop, the amount you received will be taxed as ordinary Income tax rates.

Tax implications on Mining crypto currency-

Mining is a complex process and technology that supports bit coin transactions on the Bit coin network by the use of powerful computers. It is similar to the process of supporting blocks in the block chain and payments in Bit coin. The people involved in this mining process are called miners.

When it comes to mining crypto currency, it’s important to keep in mind that any income received from mining will be subject to a flat 30% tax. It’s worth noting that the cost of acquisition for the crypto mining will be considered as ‘Zero’ when computing the gains at the time of sale. Additionally, expenses such as electricity or infrastructure costs cannot be included in the cost of acquisition. It’s important to stay informed about the tax laws surrounding crypto currency mining in your country to ensure compliance and avoid penalties.

The tax amount for crypto assets that are received at mining is determined by Rule 11UA. If you acquire crypto currency through those assets and later sell, exchange, or spend your tokens, you will be subject to a 30% tax on your income. This tax is calculated based on the market value of the asset on the day it was received on an exchange or DEX.

Tax implication on funding/Pirating-

In terms of crypto currencies, pirating (or molding) refers to the process of creating new blocks on the block chain using a Proof of Stake algorithm in exchange for payment in the form of newly issued coins and fees.

When you buy crypto currency, you may have to pay taxes on your income. How much you earn on your deposit depends on the annual percentage rate (APR) offered by the lender. For example, if you fund 100 coins at 10% APR, you will earn 10% interest per year.

This income, you earn from the funding will be taxed at 30%. In addition, when you sell your crypto assets, you will have to pay an additional 30% tax as capital gain tax.

Tax implication on Crypto Gifts-

You can get crypto gifts in the form of gift cards, crypto tokens, or crypto boxes. In Budget 2022, Digital Assets (VDA) are classified as movable assets. Therefore, if you receive crypto gifts, they will be paid under the category of ‘Other source income’ as per the Income Tax Act with normal taxes if the value is more than Rs 50,000.

If you receive crypto as a gift from your family, it will not be paid out. However, if the gift comes from a non-family member and the value is more than INR 50,000, then tax must be paid. If Gifts received on special occasions, such as inheritance, will, marriage, or death, are also tax-free.

How to disclose Crypto Currency by Income Tax Return-

To properly file your taxes for the 2022-23 financial year and 2023-24 assessment year, it’s important to report any profits earned from crypto currency using the appropriate ITR forms. Depending on how often you trade and the type of transactions you make, your crypto earnings may be categorized as either business income or capital gains. Based on the analysis of tax and consulting firms, you should report this type of income in the ‘VDA Schedule’ in ITR-2 or ITR-3. ITR-1 or ITR-4 forms cannot be used to record any of this income.

Reporting of Crypto Income in appropriate forms are as follows-

Income from business-

If a person holds the VDA for sale in the ordinary course of business, the profit from such business is taxable as business income and you should use ITR-3 form to report it as Income in Income tax Return.

Income from capital gain-

On the other hand, if the VDA is held as a capital asset (such as equity, shares, mutual funds, etc.), the income will be taxed under the heading “Capital Gains.” and you should use ITR-2 to report them.

Therefore, depending on the type of VDA holding and its purpose (trade or investment), the income will be divided from tax under the head of business income (PGBP) or capital gains.

Any proceeds from the sale of VDA should be accompanied by a ‘VDA Schedule’ reported in ITR form (ITR-2 or ITR-3, as applicable). Setting up a VDA requires information such as date of purchase, date of sale, type of income for tax purposes (capital or income business), sales price, and revenue from the sale of VDA.

If the VDA received as a gift has been exempted from the recipient, the value received by the previous recipient will be the cost of the acquisition. However, if the value of the VDA is taxable to the recipient under section 56 (2) (x) at the time of receipt, then this value is calculated as the cost of acquisition.

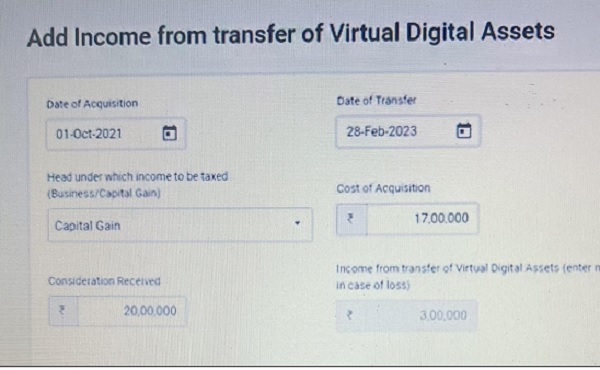

For example, Mr A sold a cryptocurrency of Rs 20 lakh on February 28, 2023. He received this cryptocurrency on October 1, 2021, for an amount of Rs 17 lakh. While reporting this capital gain transaction in ITR, the income should be reported as below in ‘Procedure’-

SET OFF OF LOSSES OF CRYPTO CURRENCY –

According to section 115BBH, loss caused by crypto cannot be set off from any profits, including profits from cryptocurrency. Hence, an investor cannot deduct the previous year’s losses on crypto assets while filing ITR this year.

In addition, investors in India are not allowed to receive money related to their crypto activities, except for the purchase price.

For example, Mr. X bought Rs 60,000 worth of Bitcoins and later sold them for Rs 80,000. He also bought Ethereum worth Rs 40,000 and sold it at Rs 30,000. This exchange pays a transaction fee of Rs 1,000. The tax on these two transactions should be compared below:

|

Currency Bitcoin |

Purchase (In Rs.) 60000 | Sell (In Rs.) 80000 | Net Profit or (Loss) 20000 | Tax Rate 30% | Tax Amount 6000 |

| Ethereum Total | 40000 | 30000 | (10000) | 30% | – 6000 |

Here, a loss of Rs 10,000 will not be allowed for set off out of Rs 20,000 gain amount. All income above Rs 20,000 is taxed at 30%. Also, a transaction amount of Rs 1,000 is not allowed for the subtraction.