1. The income tax return filed by the taxpayer is processed by the Central Processing Centre (CPC) of the Income Tax Department. The CPC (Centralized Processing Centre) in Bangalore is in-charge of handling all the primary processing of assessments. The CPC processes return without any interaction with the taxpayer and in a jurisdiction-free manner.

2. After processing the ITR, the department sends a notice cum communication to the registered e-mail address. The registered e-mail address is the one you use while e-filing your returns.

2.1 As technology is growing, so is the Income Tax Department. Now with the sending of Intimation u/s 143(1), a text message is also sent on the registered mobile number:-

2.2 TEXT MESSAGE:- ITR for AY 2020-21 and PAN abcxxxxx1r has been processed at CPC. Intimation u/s 143(1) has been sent to your registered email ID. If not received check-in SPAM folder.

3. If you have not received an e-mail communicating processing of your Return. You can find out the communication status from e-filing website in the following manner.

3.1 Login to https://www.incometaxindiaefiling.gov.in/home

3.2 Go to view return > My Account > view e-filed Return > Income Tax Return >

3.3 Click on Ack No. – AY 2020-21. The following details will be displayed:-

4. TIME LIMIT FOR INTIMATION UNDER SEC 143(1): Intimation under section 143(1) can be sent by the department within one year from the end of the financial year in which the return of income is filed. For Example: If the return for FY 2019-20 was filed on 31/10/2020 then no intimation shall be sent after 31.03.2022.

5. PASSWORD TO OPEN INTIMATION The notice you receive via e-mail will be a password-protected file. Your password will be your PAN in lowercase followed by your date of birth. For example, if your PAN is ABCDE1234F and your date of birth is 03 June 1966, your password will be abcde1234f03061966.

6. FORMAT OF INTIMATION: Intimation under sec 143(1) for Assessment year 2020-21 is in the following format:-

7. VERIFY THE DETAILS: The next step is to check that the personal details provided in the notice are correct. Pay special attention to the name, PAN, and address. Once you’re sure all the details are correct, you need to compare your income tax computation with that of the department

7.1 The details in the intimation notice will have income details along with details of any tax-saving deductions reported by you with a table indicating the amount as computed by the department under section 143(1) in the following manner:-

8. There will be following three possible scenarios:-

8.1 DETAILS PROVIDED IN THE TAX RETURNS MATCHES WITH COMPUTATION BY THE DEPARTMENT: In case the details provided in the tax returns matches with that of the computerized returns, and the tax return has been processed without any adjustments. Intimation notice received will be with no demand or no refund and the taxpayer need not do anything.

8.2 REFUND IS DUE. If there is any income tax refund due, then the income tax department will automatically transfer to the bank account indicated for this purpose in ITR once it is processed. It would be reflected in the intimation notice as well

The department will only notify that income tax refund has been processed without asking for any bank accounts.”Therefore, taxpayers are advised not to fall for SMS or email stating that income tax refund is due and that it is required to provide bank details to receive the same.

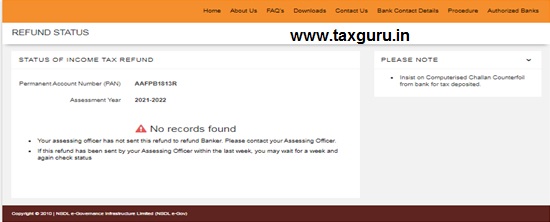

8.2.1 HOW TO CHECK THE REFUND STATUS: In case, refund is reflected in intimation notice and it has not credited to your bank account ,you can check status in the following manner

Google -“REFUND STATUS OLTAS”. You will navigate to the site:https://tin.tin.nsdl.com/oltas/refund-status-pan.html Enter your PAN No.

Refund Status will be shown as follows:

8.3 MISMATCH IN DETAILS: There may be a case where the income reported by the taxpayer in the ITR under each head (in one column) is not matched with the income under that head as computed by the income tax department (in another column).

There will be a discrepancy in the taxable income computed by the tax department and what the taxpayer has filed in his ITR due to following reasons :-

(a) Arithmetic error (if any)

(b) Incorrect claim – For example, a taxpayer has claimed deduction available for specific purposes ie deduction available to sr. citizen claimed by a normal taxpayer

(c) Loss claimed by the taxpayer – Return for the previous year for which set off of loss is claimed was furnished beyond the due date

(d) Disallowance of Expenditure in the Audit Report is not considered in computing the total income indicated in the Return filed

The taxable income computed by the department can be higher or lower due to which it will either show that such taxpayer has to pay additional tax or that a refund is due to him.

10. WHAT SHOULD BE DONE ON RECEIVING INTIMATION U/S 143(1)

In case there is an amount due and the tax is payable as per the department’s calculation. If you agree with the tax amount payable you would be required to pay the amount of outstanding taxes.

In case you do not agree with the calculations done by the income tax department you can opt to file an online request for rectification of your income-tax return under section 154 or file an appeal under section 246A.

11. TIME LIMIT TO RESPONSE AGAINST INTIMATION: The time limit of 30 days from the date of receiving the intimation is given to the recipient of the notice. If the recipient fails to respond, the return is processed after making the necessary adjustment(s) u/s 143(1)(a), without providing any further opportunities in this matter.

12. REQUEST FOR REPROCESSING THE RETURN: In case you have received arrear and claim for relief under section 89(1) in Assessment Year 2020-21, you may have received the below text message from the Income Tax Department in context with the filed ITR :-

“Dear Taxpayer, For ABCxxxxxDE and AY: 2020-21 claim of relief u/s 89 of IT Act was disallowed inadvertently. Error is regretted. Order u/s 154 rectifying the intimation would be issued expeditiously”.

If you have received such an error that means there is some clerical error from the Income Tax Department end, it says the error is regretted and the order u/s 154 rectifying such error that happened at the income tax department, they will rectify the same by the intimation that would be issued expeditiously.

In case, you have uploaded Form 10E correctly and even then your claim of relief is not considered, you can either wait for correction from the department for rectified intimation or else you can request online for reprocessing of your return. Follow the steps indicated below to file a reprocessing request:-

(a) Login to your Income Tax Portal Dashboard

(b) Select Income Tax Return, under “View e-Filed Returns/ Forms”

(c ) Select the Acknowledgement Number for the relevant assessment year

(d) Select the “Submit rectification request” link

(e) Under Request type, select “only reprocessing the data

For AY 2020-21, the reprocessing option is not yet active. You can wait for some more time for submitting the reprocessing request.

___________

The author can be approached at caanitabhadra@gmail.com

Author Bio