Yadvendra Dhabhai Vs ITO (ITAT Jodhpur)

The assessee appealed against the order of the Commissioner of Income Tax (Appeals), dated 21.07.2025, relating to AY 2021-22. The dispute concerned the rejection of the assessee’s rectification application under Section 154 by the Centralized Processing Centre (CPC), which had treated employees’ contribution towards PF and ESI amounting to Rs. 1,85,03,917 as delayed deposits.

The assessee submitted that while processing the return under Section 143(1), CPC made an addition on account of delayed deposit of employees’ contribution as per the due dates prescribed under the respective Acts, even though the amounts had been deposited before the due date for filing the return under Section 139(1). The assessee’s rectification application under Section 154 was rejected, and the CIT(A) upheld the addition relying on the Supreme Court decision in Checkmate Services Pvt. Ltd. v. CIT.

The assessee argued that the delay occurred due to the severe disruptions caused by the COVID-19 pandemic, which adversely affected business operations and liquidity. It was pointed out that the Employees’ Provident Fund Organisation (EPFO), through Circular No. C-I/Misc./2020-21/Vol.I/1112 dated 15.05.2020, had granted relaxation from levy of damages and penalties for delayed deposits during the lockdown period. According to the assessee, the failure to consider this relaxation constituted a mistake apparent from the record. It was further contended that the issue remained debatable and was under consideration before the Supreme Court.

The Revenue argued that although no penalty proceedings had been initiated by the PF and ESI authorities, the statutory due dates themselves had not been extended and, therefore, the addition was justified.

After considering the submissions and examining the record, the Tribunal observed that the CPC rejected the rectification application without adequately considering the extraordinary circumstances arising from the COVID-19 pandemic and the EPFO circular granting relaxation from penalties. The Tribunal noted that the issue regarding the due date for deposit of PF and ESI contributions was pending examination before the Supreme Court in Woodland (Aero Club) Pvt. Ltd., indicating that it involved interpretation of law.

The Tribunal held that such a debatable issue fell outside the scope of prima facie adjustments permissible under Section 143(1). It further observed that the EPFO’s decision not to initiate penalty proceedings acknowledged the genuine hardship caused by the pandemic and reflected an intention to provide relief under exceptional circumstances. The Tribunal stated that delays during the COVID-19 period should be viewed pragmatically rather than through a strict technical approach.

Accordingly, the Tribunal held that the CIT(A)’s order rejecting the assessee’s Section 154 application failed to appreciate the genuine hardships of the COVID-19 period. The addition of Rs. 1,85,03,917 was deleted, and the assessee’s appeal was allowed.

FULL TEXT OF THE ORDER OF ITAT JODHPUR

This appeal by assessee is filed against the order of Ld. Commissioner of Income Tax Appeal ADDL/JCIT (A)-9 Delhi [hereinafter referred to JCIT(A)] dated 21.07.2025 with respect to Assessment Year 2021-22 challenging therein rejection of its application by CPC filed u/s 154 treating employees contribution to PF and ESI amounting to Rs. 1,85,03,917/- as delayed deposit.

2. At the outset, the Ld. Counsel for the assessee has submitted that the CPC while processing return of income u/s 143(1) made an addition on account of delayed deposit of employees contribution as per due dates prescribed under respective Acts, though such payments were admittedly deposited before the due date of filing the return of income u/s 139(1). He further submitted that the CPC has rejected its application filed u/s 154 of the Income Tax Act, 1961 dated 29.12.2022. The Ld. CIT(A) has upheld the addition relying on the decision of Hon’ble Supreme Court in the case of Checkmate Services Pvt. Ltd. Vs. CIT 448 ITR 519 (SC).

3. The AR submitted that the CPC considered his application filed u/s 154 and concluded with the observation that the assessee’s request has been examined and the said intimation u/s 143(1) stands rectify by upholding the 143(1) order without changing the assessed income u/s 143(1) of the Income Tax Act. The AR contended that the addition made by CPC u/s 143(1)(a) was not justified in disallowance of the employees contribution to PF and ESI deposited delayed to the due date under the respective Act but before due date of filing of return of income due to the COVID-19 pandemic.

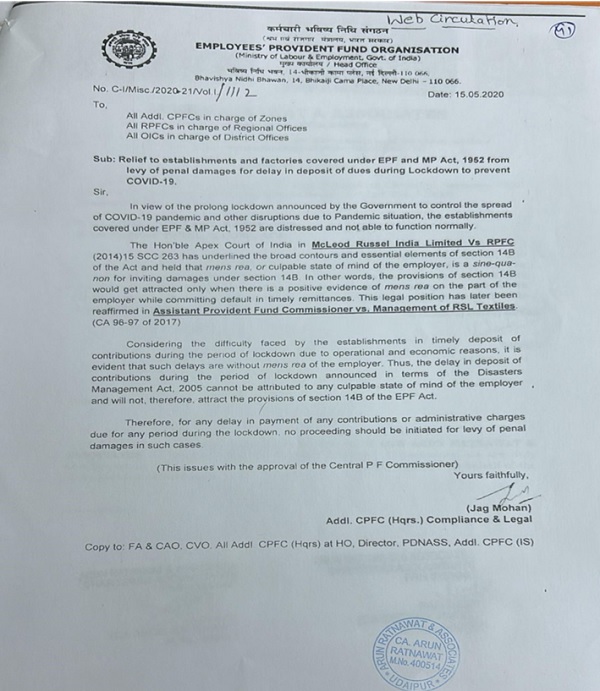

4. The AR further submitted that the unprecedented disruption caused by Covid-19 pandemic severely interrupted business operations and liquidity that caused such hardships that the Employees Provident Fund Organization (in short “the EPFO”) granted extension from levy of damages and penalties for delayed deposit of PF and ESI during the lockdown period. A copy of relevant notification is filed for reference on the record which reads as under:

5. Thus, the Ld. AR has contended that the EPFO has issued the above circular No. C-I/Misc./2020-21/Vol.I/1112 dated 15.05.2020 in view of the prolonged lockdown announced by Government to control the spread of COVID-19 pandemic and that any delay in payment of any employer contribution or administrative charge due for any period during the lockdown, no proceedings be initiated for levy of penal damages in such cases. The appellant’s said delay has been covered under exempted period for which relaxation has been granted by EPFO from levy of damages and penalties for any delayed deposits of PF and ESI during the lockdown period under the PF and ESI Act. He accordingly, pleaded that it is a prima facie mistake, in not considering the COVID period and that it is being a debatable issue yet pending under review before the Hon’ble Apex Court for consideration. The AR pleaded that the addition made may be deleted, in support, he placed reliance on the following judgments:

- ACIT Vs. Ashiana Housing Ltd.

- Maria Fernandes Cheryl Vs. ITO

- Kishore Hira Bhandari Vs. ITO

- Kalpesh Synthetics Pvt. Ltd. Vs. DCIT (ITAT Mumbai)

- Mohangarh Engineers & Construction Company Vs. CPC (ITAT Jodhpur)

- Crescent Roadways Pvt. Ltd. Vs. CPC (ITAT Kolkata)

6. The Ld. DR on the other hand placed reliance on the impugned order. He submitted that although no penalty proceedings were initiated by the PF and ESI Department but the due dates were not extended. She pleaded that the impugned order may be sustained.

7. Having heard both the sides and perusal of record, we find that the CPC has rejected the application filed by the assessee u/s 154 to grant relief on account of delayed payment of employer contribution to PF and ESI even brushing aside the unprecedented disruption caused by COVID-19 pandemic and that the circular issued by EPFO granting relaxation from levy of damages and penalties for delay deposits during the lockdown period. The claim of deduction on deposit of employer contribution to PF and ESI before the due date under respective Act or due date of filing of return of income u/s 139(1) of the Act is a debatable issue. Recently, the Hon’ble Supreme Court has issued a notice in the case of Woodland (Aero Club) Pvt. Ltd. SLP No. 1532 of 2026 in the month of January, 2026 to examine the issue of due date for deposit of employer contribution to PF and ESI interpretation amid lingering conflicts where the proceedings are pending and judgment is awaited.

8. Considering the EPFO aforesaid circular on granting relaxation from levy of damages and penalty for delay deposit during the lockdown period and that the issue being subjudice for review before the Supreme Court, shows that it is an issue which involves interpretation of law at the level of Hon’ble Apex Court which is out of the scope of the provisions of Section 143(1) to make prima facie adjustments by CPC to the return of income of the assessee. It is further emphasized that the EPFO vide circular dated 15.05.2020, the due dates were extended as also observed by the Ld. CIT(A) that no penalty proceedings were initiated as the due dates were extended. In our view, the relaxation from penalties makes is apparently clear that the EPFO authorities has acknowledged genuine hardship hence intended to grant relief to the appellant assessee from levy of penalty amount on acceptance of delayed payments under the exceptional circumstances like COVID-19 pandemic. Meaning thereby that the relaxation of penalty by the competent authority from Employees Fund Organization, Ministry of Labour and Employees, Government of India, acknowledges the genuine hardship and intended to grant relief. In such circumstances of COVID-19 pandemic, the non-levy of penalty tantamount to acceptance of delay under exceptional circumstances the absence of formal extension of due date does not negate the intent of relief. Therefore, such delays during the COVID-19 pandemic are deserves to be viewed pragmatically and not in a strict technical manner. Accordingly, we hold that the impugned order of the Ld. CIT(A) in rejecting the application of the assessee filed u/s 154 of the Income Tax Act is perverse to the facts on record by not appreciating the genuine hardships of COVID-19 period as duly acknowledged by EPFO authorities.

8. In the above view, we accept the grievance of the assessee as genuine and as such, delete the addition of Rs. 1,85,03,917/-.

9. Thus, the appeal of the assessee is allowed.

Order pronounced in the open court on 21/05/2026.