Vatsal Ponda

Article explains What is AMP Expenditure, Why is AMP Expenditure covered under the ambit of Transfer Pricing, Why was Intensity Adjustment used instead of BLT and How is Intensity Adjustment used?

Article explains What is AMP Expenditure, Why is AMP Expenditure covered under the ambit of Transfer Pricing, Why was Intensity Adjustment used instead of BLT and How is Intensity Adjustment used?

Page Contents

What is AMP Expenditure?

♣ AMP refers to Advertisement, Marketing and Promotion Expenses.

♣ AMP Expenses are usually incurred by the company in for increasing the revenue of the company and enhancing the value of the companies brand value.

Why is AMP Expenditure covered under the ambit of Transfer Pricing?

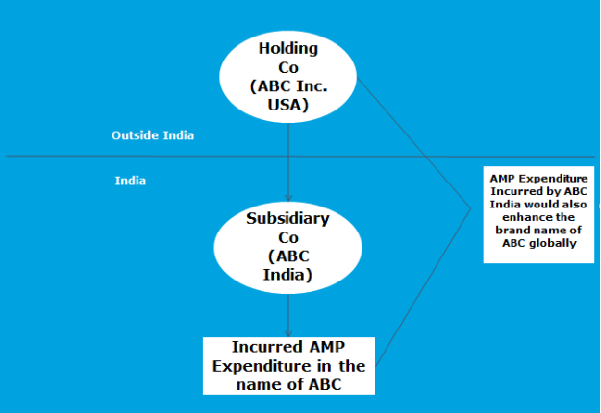

- As seen in the above example ABC India is subsidiary of ABC.

- ABC India also incurred AMP Expenditure in the name of ABC as it is also selling goods naming brand ABC.

- As this expenditure incurred would help ABC India to enhance the sales, but unknowingly it would also enhance the Brand value globally.

- The Income Tax department in this scenario is of the view that ABC India should be reimbursed for the expenses which is incurred by ABC India to enhance the brand value globally and has referred this transaction as an international transaction.

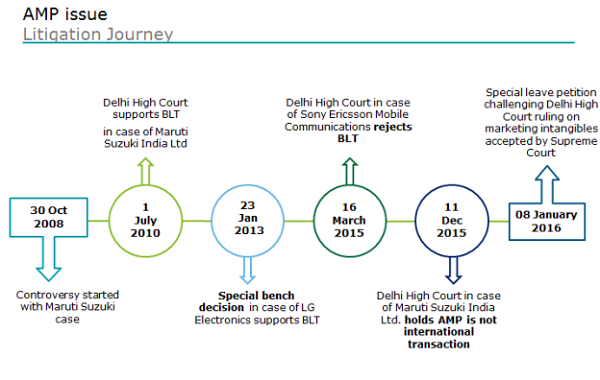

- However, there are a lot of case in which the assessee had objected that AMP is not an international transaction and the same question is in front of Supreme Court currently.

How would it be practically possible to delineate the expenditure in to expenses utilized to increasing the revenue of ABC India and enhancing the Brand value of ABC Globally?

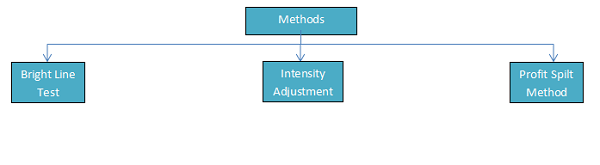

- There were many precedents in the past which was able to delineate the AMP Expenses into utilized for increasing the revenue and enhancing the brand value.

- The methods which were used for the same can be seen as follows:

How are the above method used practically?

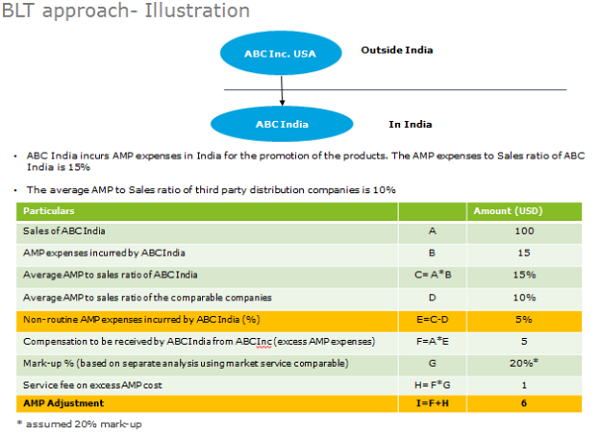

Bright Line Test (BLT)

- Under the BLT test first of all we calculate % of AMP expenditure to sales of both the tested party and comparable.

- We evaluate the difference between the same, if % of tested party is more than that of the comparable we can see that the profit of tested party would be less and there is a part of such excess expenditure for the purpose of enhancing the brand value.

- Now we multiply the difference % with the sales of the tested party, this amount should be then increased by the mark-up which a normal market support services would charge in an uncontrolled transaction.

- This amount should have been charged to ABC Inc. USA as there was an enhancement of the brand value globally due to the AMP expenses incurred by ABC India.

Intensity Adjustment

Why was Intensity Adjustment used instead of BLT?

- In the earlier case of LG Electronics the special bench of Delhi ITAT had approved BLT as an appropriate method.

- However In the case of Sony Ericsson Mobile Communications the Delhi High court had rejected the Bright Line Test.

- BLT was rejected saying the “bright line test” has no statutory mandate and a broad-brush approach is not mandated or prescribed. The court further added that using BLT would mean adding words in the statute as BLT is not mentioned anywhere in the Income Tax Act,1961 and using BLT is not in accordance to the Law.

- The department taking into consideration the judgment of Sony Ericsson Mobile Communications used AMP adjustment in the case of Luxottica India Eyewear Pvt saying that AMP is not an international transaction but a function.

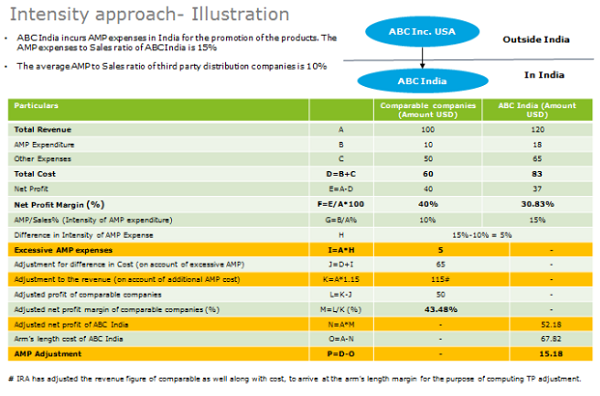

How is Intensity Adjustment used?

- The Department had used TNMM over RPM which was used by the assesse.

- As the name refers, similar is the manner of the adjustment.

- As AMP is now a function we have to make an intensity adjustment to the comparable as in the below illustration % of AMP to sale of the tested party is more than that of the comparable, we have to equalize the position of the comparable by increasing the AMP Expenditure up to the extent of the tested party.

- As now we have increased the AMP expenses of the comparable department also has to increase the revenue of the comparable.

- Net profit margin of comparable is computed after adjusting the AMP intensity to the cost and enhanced revenue thereof

- Arm’s length profit for the assessee is determined using net profit margin of comparable computed above

- Arm’s length cost has been arrived after reducing arm’s length profit from the revenue of Indian taxpayer

- The excess cost is computed and made the TP adjustment accordingly

Profit Split Method

- Percentage of AMP expenditure incurred by Indian taxpayer and comparable (considered as routine) are computed and non-routine AMP expenditure is determined

- Operating profit on sales percentage of the comparable and Indian taxpayer (excluding non-routine AMP expenditure) is computed and difference is determined as “Residual Profit”

- Appropriate allocation keys are applied by IRA (using FAR contribution analysis) to arrive at the AE’s share of profit and the same is thereafter multiplied to revenue figure of Indian taxpayer to arrive at residual profit belonging to AE

- AEs residual profit is reduced from non-routine expenditure (arrived earlier) to make the TP adjustment.

–

Kindly Refer to

Privacy Policy &

Complete Terms of Use and Disclaimer.

Author Bio