Introduction: When determining the issue price of equity shares, it’s essential to consider several factors including face value, intrinsic value, and market value. However, one of the most pivotal considerations is the income tax implications, specifically the fair market value (FMV) as defined under the Income Tax Act. This article explores the significance of FMV in setting the issue price and the potential tax impacts associated with different pricing scenarios.

Fair Market Value’s Role in Equity Share Pricing

There are typically three values for equity share;

1. Face Value

2. Intrinsic Value

2. Market Value

Face Value is nothing but the value which was set per equity share during the time of inception of the company read with changes as on date, if any. Generally the value of equity capital is valued in face value for books, except for Ind-AS.

Intrinsic Value is the actual worth of the equity share after estimation. This is the fair value in which the share can be traded.

Market value is the value in which the equity shares are traded in the market.

What should be the issue price?

To decide on issue price, (inter-alia) of various factors, one important and essential consideration should “Income Tax”. In most of the cases, “Income Tax” plays a huge role in driving the issue price. Why is it important? Let’s discuss.

As per the provisions of the Income tax Act, the term what we discussed i.e “intrinsic value” is called as “Fair Market Value” (FMV).

It is always advisable to issue equity share at the “Fair Market Value”. FMV is determined either by Chartered Accountant or Merchant Banker, in accordance with various provisions prescribed under Rule 11 UA of the Income Tax Rules. Let us not go into detail of the methodology of valuation of FMV, as it is outside the scope of the intention of this article. Let us all assume, a “Fair Market Value” would be determined in accordance to Rule 11 UA.

Now, having in hands the FMV, there might be three (3) possible probabilities;

| S. No | Particulars on Probability | Impact on Income Tax |

| 1. | Issue Price = FMV | No |

| 2. | Issue Price > FMV | Yes |

| 3. | Issue Price < FMV | Still Yes |

Important considerations to be observed;

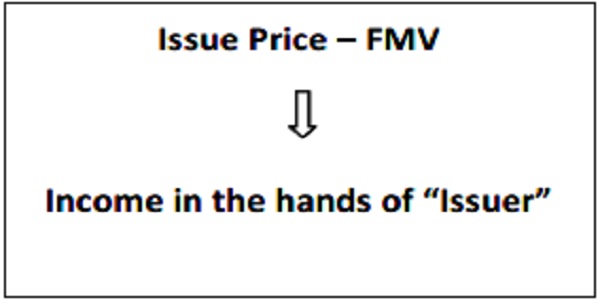

Section 56(2)(viib) of the Income Tax Act, 1971:

1. If, issue price is more than the Face Value. (and)

2. If, issue price > FMV

The Net amount received by the issuer over and above the FMV, shall be treated as income in the hands of the issuer.

Non-Applicability or exceptions;

The above said shall not apply where the consideration for issue of shares is received—

(i) by a venture capital undertaking from a venture capital company or a venture capital fund or a specified fund; or

(ii) by a company from a class or classes of persons as may be notified by the Central Government in this behalf:

Section 56(2)(xc) of the Income tax Act, 1971:

1. If, issue price < FMV

The Net amount the investor had invested in the equity less that its FMV, shall be treated as income in the hands of the investor. (if aggregate FMV is more than Rs. 50,000)

Conclusion:

The intention of the author is not hereby to guide on what should be fixed as Issue Price. The issue price may be fixed equal to the FMV or more than the FMV or even less than the FMV. It’s still completely and purely a commercial decision. The only intention of the author is throw some light on the above said provisions before such commercial decisions are taken, to make such decisions more efficient.

*****

Disclaimer: Any views construed in the above article cannot qualify as opinion or advice. Whatsoever views expressed by the author is just for informational purposes only. Any reliance on the above article is at the reader’s own risk. The content is based on research by author based on factual information available at the time of publishing. Author can be reached out at his E-Mail for any advice or opinion in this regard.

Author Bio