Karan Khatri

Introduction

Introduction

Applicability of transfer pricing provisions was earlier limited to International Transactions only. With effect from 01.04.2013, the scope of Transfer Pricing provisions is extended to ‘Specified Domestic Transactions’ and is accordingly applicable from A.Y. 2013-14.

With the applicability of Transfer Pricing provisions on Specified Domestic Transactions, now it is the obligation on the taxpayer to report/document & substantiate the Arm’s Length nature of such transaction.

International Transfer Pricing was there world wide in both developed and developing countries. When other developing countries introduced Transfer Pricing, Like Korea in 1998 and China 1999, India introduced International Transfer Pricing in 2001. Now the question arise, Why and What made Transfer Pricing a necessity? More than 100 countries have introduced International as well as Domestic Transfer Pricing Provisions.

So, before we move towards Domestic Transfer Pricing lets Know little bit of International Transfer Pricing.

Page Contents

Illustration of International Transfer Pricing

In the Above Image,

In the Above Image,

There is a USA based car manufacturing company, which has set up six subsidiary companies across the world. Those are as follow:

i. Trading Company inBVI (British Virgin Islands)

ii. A Insurance Company inJersay island.

iii. Company for Holding Brand in Bahams

iv. Manufacturing or Trading for Rubber Tyres inMalaysia.

v. A company inIndia for Automobile Components and Software.

vi. A Car designing company in Japan

Subsidiary companies in Malaysia, India and Japan are set up to provide Raw Materials and Labour for manufacturing the car. This set up is done since in USA Raw material is not easily available and Labour is also expensive. The Trading Company in BVI purchases raw materials and labour from this countries at a reasonable price which is acceptable to all this countries.

In BVI there is low tax or nil tax, the trading company therefore sells this Raw Material or components to USA car manufacturing company at a very high profit margin. The USA company assembles the components to manufacture cars. This cars are sold in US market at a reasonable profit. Since USA company is earning reasonable profit it has to pay tax @ 40%. Now here comes the interesting part. To reduce its tax liability USA company takes loan and insurance from the insurance company set up in Jersey Island. Due to which USA company pays interest and premium to the company in Jersey Island, which is deducted against profit.

The company holding brand or logo in Bahamas has given license to the USA company to use the brand and logo. For the same the USA company pays royalties to the Bahamas Company. Which is also a charge against profit. Ultimately the US company will have NIL Profit or a Loss.

This Money at Bahamas and BVI is routed or flowed to Jersey Island. In all this arrangement the final price of the product is not changed and also shares value is also not changed. Hence, the group pays less amount of tax. Due to which Developed countries like US where car is manufactured and sold and also Developing countries like Malaysia, India and Japan does not get tax dues which it should get. Therefore Transfer Pricing was introduced in the jurisdiction.

Now we come to Domestic Transactions.

Objective of Domestic Transfer Pricing

There are two counts where tax arbitrage happen in India. (objective of domestic transfer pricing)

1. Tax Holidays or Differential Tax

2. Accumulated Losses or loss making concerns

Lets see an example of Differential Tax

In the case Above there is Co. A and Co. B which is in SEZ unit. As we can see Co. A Income is Rs 5000 and Expenses is Rs 4000 whereas in Co. B in SEZ Income is Rs 7000 and Expenses is Rs 3000. And the Related party transactions amount to Rs 500. So Co. A has to pay Tax of Rs 150 and Co B in SEZ has to pay nil tax. But if we see the planned situation the Company needs to only make one change, i.e. increase Related party transactions from Rs 500 to Rs 1500. Due to which The company A as well as B in SEZ does not have to pay tax. Therefore the government has introduce Domestic Transfer Pricing to avoid such kind of Tax Arbitrage.

In the case Above there is Co. A and Co. B which is in SEZ unit. As we can see Co. A Income is Rs 5000 and Expenses is Rs 4000 whereas in Co. B in SEZ Income is Rs 7000 and Expenses is Rs 3000. And the Related party transactions amount to Rs 500. So Co. A has to pay Tax of Rs 150 and Co B in SEZ has to pay nil tax. But if we see the planned situation the Company needs to only make one change, i.e. increase Related party transactions from Rs 500 to Rs 1500. Due to which The company A as well as B in SEZ does not have to pay tax. Therefore the government has introduce Domestic Transfer Pricing to avoid such kind of Tax Arbitrage.

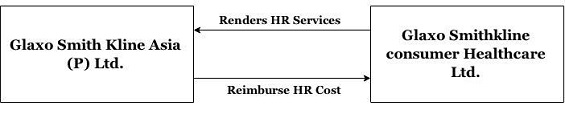

Background

In the case of IT, DELHI Versus GLAXO SMITHKLINE ASIA(P) LTD. The assessee (Glaxo SmithKline Asia) did not have any employee other than a company secretary and all administrative services relating to marketing, finance, HR etc were provided by Glaxo Smith Kline Consumer Healthcare Ltd (“GSKCH”) pursuant to an agreement under which the assessee agreed to reimburse the costs incurred by GSKCH for providing the various services plus 5%. The costs towards services provided to the assessee were allocated on the basis suggested by a firm of CAs.

The AO disallowed a part of the charges reimbursed on the ground that they were excessive and not for business purposes which was upheld by the CIT (A). However, the Tribunal deleted the disallowance on the ground that there was provision to disallow expenditure on the ground that it was excessive or unreasonable unless the case of the assessee fell within the scope of s. 40A (2). It was held that as it was not the case of the Department that s. 40A (2) was attracted, the disallowance could not be made (see 290 ITR 35 (Del) for facts).

The department challenged the deletion. So, SLP (Special Leave Petitions) Dismissed on following grounds, Authorities of the finding that tow companies are not related parties u/s 40A(2). and the entire exercise is revenue neutral (as one is showing it as an expense and another company is showing it as an income). Therefore Hon’ble Supreme Court Suggested Transfer Pricing Provisions should be extended to domestic transactions to “reduce litigation”.

Provision of Section 92BA

As per the section 92BA of the IT Act, “Specified Domestic Transaction” in case of an assessee means any of the following transactions (the aggregate of which exceeds INR 20 crore in previous year and which is not an international transaction), namely:—

- any transaction referred to in section 80A;

- any transfer of goods or services referred to in section 80-IA(8);

- any business transacted between the assessee and other person as referred to in section 80-IA(10);

- any transaction, referred to in any other section under Chapter VI-A or section 10AA, to which section 80-IA(8) or section 80-IA(10) are applicable; or

- any business transacted between the persons referred to in sub-section (6) of section 115BAB (With Effect From 01 April, 2020)

- any other transaction as may be prescribed,

If a transaction is an International Transaction, then the same will not be a Specified Domestic Transaction.

1. Any Transaction Referred To In Section 80A.

Section 80A (6) refers to internal transactions between various units / undertakings of the assessee in respect of goods or services. This clause covers any transactions of goods or services and hence this transaction will be applicable to income as well as expenditure.

2. Transactions of Tax Holiday Undertakings

1. Any transfer of goods or services referred to in section 80-IA(8)

2. Any business transacted between the assessee and other person as referred to in section 80-IA(10)

3. Any transaction, referred to in any other section under Chapter VI-A or section 10AA, to which section 80-IA(8) or section 80-IA(10) are applicable;

It is a common practice among corporates, enjoying tax holiday period, to park excess profits in tax-exempt units / businesses. To curb this loophole, given clauses has inserted in the DTP law. Now TPO (Transfer Pricing Officer) is empowered to make adjustments if it appears that ‘more than ordinary profits’ are earned by tax exempt businesses/units owing to its ‘close connection’ with transacting parties.

Section 80IA (8):

Section 80IA-(8) deals with the internal transactions with more than one undertaking / units of the assessee, out of which one or more undertaking is enjoying the tax holiday. Normally units enjoying tax holiday, charge more than the market value for goods or services used by non-eligible units. Due to this practise, there is no effect on the health of the tax holiday unit as there are no taxes at all and the non-eligible unit gets higher deduction from taxable income. As per Section 80IA-(8), if the internal transfer of goods or services is not at market value, then profits or gains of transacting units shall be computed, as if, transfer, in either case, had been made at market value of such goods or services. Duty is on the taxpayer to prove that the internal transfer is at ALP (Arm’s Length Price)

Section 80IA (10):

As per this clause, when due to close connection between assessee and ‘any other person’ or for any other reason, the eligible business of the assessee produces ‘more than the ordinary profit’, then for the purpose of deduction under this section, profit of the eligible business shall be determined by taking ALP of the transaction. Primary duty is on the taxpayer to prove that the internal transfer is at ALP. However, the department has to prove that the transaction is not at ALP.

Section 10AA:

As per this section, profits of the units located in SEZ, engaged in the manufacturing of any article or thing or providing any services, is exempt subject to conditions.

Non Allocation of Indirect Costs / Services to Tax Holiday Units:

Many a times indirect expenses / head office expenses / administrative expenses have not been charged to the undertaking enjoying tax holiday, due to which more than ordinary profits arises to the tax-holiday undertaking.

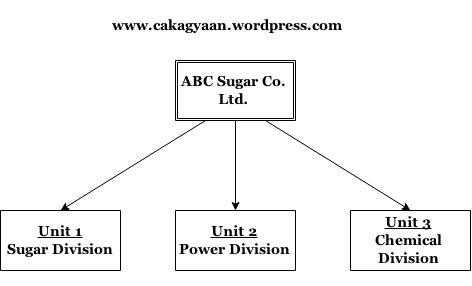

ILLUSTRATION ABC Sugar Co Ltd., engaged the manufacturing of Sugar, is having three divisions- Sugar, Power & Chemical. Power produced by power division is captively consumed in the sugar and chemical division. In case of any shortfall in power generation, the same is purchased from the State Electricity Board (SEB). By-product of the sugar division is used in chemical division for producing ethanol. Profits of the power division are exempt u/s 80-IA.

ABC Sugar Co Ltd., engaged the manufacturing of Sugar, is having three divisions- Sugar, Power & Chemical. Power produced by power division is captively consumed in the sugar and chemical division. In case of any shortfall in power generation, the same is purchased from the State Electricity Board (SEB). By-product of the sugar division is used in chemical division for producing ethanol. Profits of the power division are exempt u/s 80-IA.

INR 5 / unit have been charged by Power Division to sugar & chemical divisions for consumption of electricity. However, SEB rate for industrial undertakings are INR 4/ unit. Due to this pricing, the profit of the power division, which is enjoying a tax holiday, gets inflated by INR 1/ unit. Further, taxable profits of sugar and chemical divisions get reduced due to overcharging by the power division.

There are certain administrative/ indirect expenditure which have been incurred by ABC Sugar Co Ltd. As per prudent accounting norms, entire expenditure should be allocated to the three divisions in a proper ratio. However, ABC Sugar Co Ltd had not allocated the indirect expenditures in the Power division, due to which profits of power division gets inflated and profits of Sugar & chemical division gets reduced. Domestic Transfer Pricing law is introduced to curb similar types of transactions.

3. Any Other Transaction As May Be Prescribed:

Board (CBDT) had been given the power to notify any other transaction, which they feel it necessary, to include in the definition of “Specified Domestic Transaction.”

Arm’s Length Price Methods

As per Section 92C, the Arm’s Length Price in relation to “Specified Domestic Transaction” shall be calculated by the any of the following methods, being the ‘most appropriate method’

| Methods | Comparability |

| Comparable Uncontrolled Price | ‘Price’ of the transaction |

| Resale Price Method | ‘Gross Margin’ of Company reselling the product / services to the unrelated parties |

| Cost Plus Method | ‘Gross Margin’ of company selling manufactured product / services to the unrelated parties |

| Profit Split Method | ‘Splits profits’ between the parties to the transactional based on economic Parameters |

| Transactional Net Margin Method | ‘Net profit margin’ of the tested party |

| Other Method | Prescribed by the board |

As per Rule 10C of the Income Tax Rules, most appropriate method shall be the method which is best suited to the facts and circumstances of each particular transaction and provides the most reasonable measure of the transaction. Following factors should be taken into account while choosing the most appropriate method namely:

I. the nature and class of the international transaction;

II. the class or classes of associated enterprises entering into the transaction and the functions performed by them taking into account assets employed or to be employed and risks assumed by such enterprises;

III. the availability, coverage and reliability of data necessary for application of the method;

IV. the degree of comparability existing between the international transaction and the uncontrolled transaction and between the enterprises entering into such transactions;

V. the extent to which reliable and accurate adjustments can be made to account for differences, if any, between the international transaction and the comparable uncontrolled transaction or between the enterprises entering into such transactions;

VI. the nature, extent and reliability of assumptions required to be made in application of a method.

Documentation Required

As per Section 92D Every person,—

(i) who has entered into an international transaction or specified domestic transaction shall keep and maintain such information and document in respect thereof as may be prescribed;

(ii) being a constituent entity of an international group, shall keep and maintain such information and document in respect of an international group as may be prescribed.

Further, the Assessing Officer or the Commissioner (Appeals) may, in the course of any proceeding under this Act, require any person referred above to furnish any information or document referred therein, within a period of thirty days from the date of receipt of a notice issued in this regard. The Assessing Officer or the Commissioner (Appeals) may, on an application made by such person, extend the period of thirty days by a further period not exceeding thirty days.

As per Section 92E, the assessee has to take an accountant’s report, in Form 3CEB, duly signed and verified as per the provisions of the Act. The Transfer Pricing Audit Report is required to file electronically on or before the due date of filing of Income Tax Return i.e. on or before 30th November of the respective assessment year.

Penalty Provisions

| Default | Nature of penalty |

| · Failure to maintain documents; or

· Failure to report a transaction in the accountant’s report; or · Maintaining or furnishing incorrect information or documents |

2% of the value of transaction |

| failure to furnish master file | Rs 5,00,000 |

| · Failure to furnish documents | 2% of the value of transaction |

| · Failure to furnish Form 3CEB by the due date | Rs 100,000 |

| furnishing incorrect information in reports and certificates | Rs 10,000 for each report |

| · In case of a transfer pricing adjustment, in absence of good faith and due diligence by the taxpayer in applying the provisions and maintaining adequate documentation. | 100%-300% of tax on the adjusted amount |

Click here to Read other Articles of Karan Khatri

(Republished with Amendments by Team Taxguru)

i need to have expert advise on transfer pricing, so if you can provide me contact details of Mr. karan khatri or some like other professional experts

What is the limit (Domestic Transaction) for transfer pricing audit for the AY2020-21

An outstanding one

Dear sir

in my company 18 million INR trnsfered from Hong kong and 19million spend in a year. so can u guide me to calculate the tax

Is the diagram given as example for differential tax correct? The name of company changed interchanged in planned situation rite?

Sir,

Your article was very informative on SDT issue,I have one query if I sell goods to unrelated party and if the unrelated party in return sells the same to my sister concern would it fall under the purview of Specified Domestic Transaction and thereby attracting Transfer Pricing provision??

Thank you

Nice one sir!!! as in your flipkart artciles, your expertise in explaining multi-national corporates comes through! and we are the beneficiaries.. Keep posting

Very effective….worth reading

Dear Sir,

Please Guide in Following case regarding the applicability of Transfer Pricing provisions.

A LTD ———-> DIRECTOR MR.B——> Relative of Mr B ——–> Has Substantial Shareholding in————————> Z Ltd.

Also , will the provisions of DTP be applicable in Both A LTD & Z Ltd or only A LTD.

Nice article, keep writing….