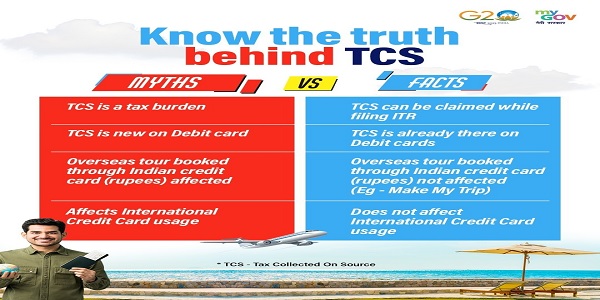

Myth 1: TCS applies to all foreign payments made by Indian companies.

Fact: This is a myth. Tax Collected at Source (TCS) is a provision under the Indian Income Tax Act that requires the collection of tax at the source of specific transactions. However, TCS does not apply to all foreign payments made by Indian companies. It primarily applies to specific transactions such as the sale of goods, certain services, or specified financial transactions as prescribed by the tax authorities.

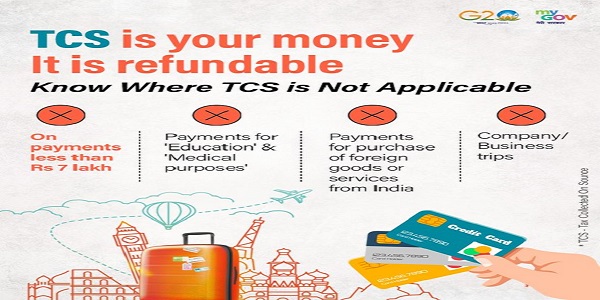

While TCS may apply to certain transactions, here’s a helpful list of payments where it’s not applicable.

Here’s a helpful list of payments where TCS applies. Stay informed!

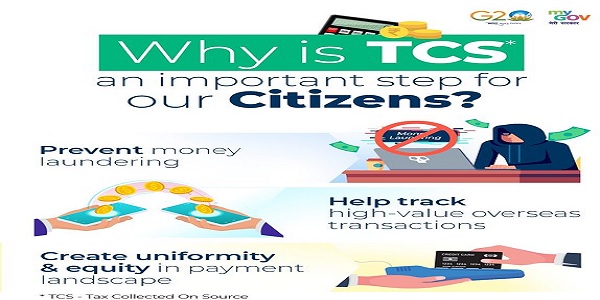

TCS is a vital step towards a transparent and equitable payment landscape. From preventing money laundering to tracking overseas transactions, it paves the way for a stronger economy.

Myth 2: TCS is collected on the total amount of foreign payments.

Fact: This is a myth. TCS is typically collected on a portion of the foreign payment, not on the total amount. The applicable TCS rate and the specific portion of the payment subject to TCS vary depending on the nature of the transaction and the provisions of the Income Tax Act. It is important to consult the relevant tax laws and seek professional advice to determine the specific TCS applicability and rates for a particular transaction.

Myth 3: TCS is not applicable when making foreign payments to non-residents.

Fact: This is a myth. TCS can be applicable on certain foreign payments made to non-residents, subject to the provisions of the Income Tax Act. The applicability of TCS depends on various factors such as the nature of the payment, the residency status of the recipient, and any exemptions or thresholds specified by the tax authorities. It is essential to review the relevant tax provisions and consult with experts to determine the specific applicability of TCS.

Myth 4: TCS is a form of double taxation on foreign payments.

Fact: This is a partial myth. While TCS is a form of upfront tax collection on certain transactions, it does not necessarily mean double taxation. The taxes collected through TCS can be adjusted against the final tax liability of the taxpayer. If the taxpayer is eligible for tax credit or a lower tax rate based on applicable tax treaties or provisions, they can claim a refund or adjust the TCS amount against their final tax liability.

Myth 5: TCS applies uniformly to all foreign payments regardless of the amount.

Fact: This is a myth. TCS provisions may have specific thresholds or exemptions based on the amount of the payment. For instance, there may be certain thresholds below which TCS does not apply or specific exemptions for smaller transactions. The applicability of TCS on foreign payments depends on the specific provisions mentioned in the Income Tax Act and any subsequent notifications or clarifications issued by the tax authorities.

Conclusion: Understanding the provisions of Tax Collected at Source (TCS) under Income Tax on Foreign Payments is crucial to comply with the tax regulations. While TCS is not applicable to all foreign payments made by Indian companies, it can be applicable to specific transactions as specified by the Income Tax Act. It is important to consult the relevant tax laws, seek professional advice, and understand the specific provisions and thresholds to determine the applicability of TCS on foreign payments accurately.